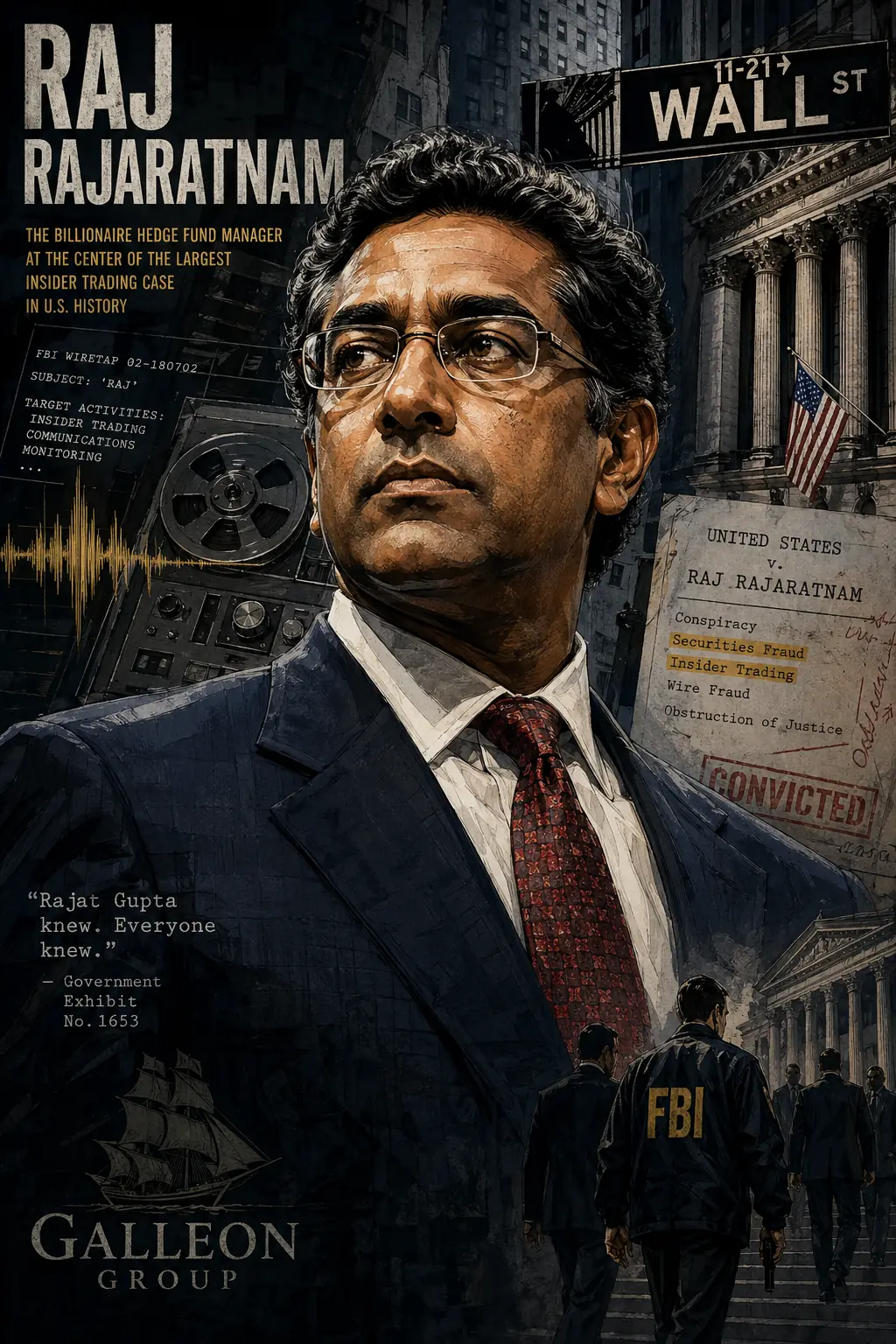

Raj Rajaratnam: The Hedge Fund King Who Built Wall Street's Biggest Insider Trading Ring

He ran Galleon Group, a $7 billion hedge fund, and had the best information on Wall Street. The problem was that the information was stolen — and the FBI was listening to every phone call.

View all stories about this mogul

Raj Rajaratnam had the best information on Wall Street. His hedge fund, Galleon Group, consistently outperformed the market. His stock picks were uncanny. His timing was perfect. He always seemed to know what was going to happen before it happened. That’s because he did — he was getting tips from corporate insiders, board members, and consultants who fed him confidential information about mergers, earnings, and strategic decisions before they were made public. It was the largest insider trading ring ever prosecuted, spanning dozens of companies and hundreds of millions in illegal profits. And the FBI caught it all on tape.

Chapter 1: The Tamil Tiger’s Son (1957–1983)

Rajaratnam Rajaratnam was born on June 15, 1957, in Colombo, Sri Lanka (then Ceylon), to a Tamil family. His father was a successful businessman who ran a Singer sewing machine distributorship. The family was wealthy by Sri Lankan standards — upper-middle class, educated, connected. But Sri Lanka in the 1970s was increasingly unstable, with ethnic tensions between the Sinhalese majority and Tamil minority escalating toward civil war.

Rajaratnam left Sri Lanka as a teenager to attend school in England, then came to the United States, enrolling at the University of Sussex before transferring to the Wharton School of Business at the University of Pennsylvania — one of the most prestigious business schools in the world. At Wharton, he earned his MBA and developed the skills and connections that would define his career.

He was smart, ambitious, and intensely competitive. Fellow students described someone who was always working the angles — not dishonest, exactly, but always looking for an edge. He understood instinctively that in finance, information is the most valuable commodity. The person with the best information wins. This insight would make him a billionaire and then send him to prison.

Chapter 2: Needham and the Education of a Trader (1983–1997)

After Wharton, Rajaratnam joined Needham & Company, a small investment bank that focused on technology companies. It was the perfect training ground. Needham was plugged into Silicon Valley and the emerging tech industry, giving Rajaratnam access to executives, engineers, and entrepreneurs who were building the companies that would dominate the next two decades.

At Needham, Rajaratnam developed his signature approach: build deep relationships with company insiders, gather as much information as possible, and trade on superior knowledge. Within the bounds of the law, this is called fundamental research. Analysts meet with management, tour factories, talk to customers, and synthesize information into investment theses. The line between aggressive research and insider trading is clear in theory and blurry in practice.

Rajaratnam rose to become head of Needham’s technology research group and then its president. He was making millions and building a reputation as one of the most connected technology investors on Wall Street. But Needham was small, and Rajaratnam wanted his own fund. In 1997, he left to found Galleon Group.

Chapter 3: Galleon Group — The $7 Billion Powerhouse (1997–2005)

Galleon Group launched with $250 million and grew rapidly. Rajaratnam’s track record was exceptional — annual returns that consistently beat the market. The fund attracted institutional investors, pension funds, and wealthy individuals. By the mid-2000s, Galleon managed approximately $7 billion, making it one of the largest hedge funds in the world.

Rajaratnam’s investment style was aggressive and technology-focused. He made large, concentrated bets on tech companies, often timing his trades around earnings announcements, mergers, and other corporate events with remarkable precision. His analysts were some of the best-paid on Wall Street, and the firm had a culture of relentless information gathering.

The results attracted attention — and not just from investors. Rajaratnam’s uncanny ability to trade ahead of major announcements caught the eye of the SEC, which began informal inquiries into Galleon’s trading patterns as early as 2005. The agency noticed that Galleon frequently accumulated large positions in companies just days before merger announcements or positive earnings surprises. The pattern was too consistent to be luck.

Chapter 4: The Network of Insiders (2003–2009)

What made Rajaratnam’s scheme different from garden-variety insider trading was its scale and sophistication. He didn’t have one source — he had a network. At its height, the insider trading ring included corporate executives, board members, consultants at McKinsey & Company, and employees at technology companies including Intel, IBM, Google, and Goldman Sachs.

The most prominent insider was Rajat Gupta, the former managing director of McKinsey & Company and a member of Goldman Sachs’ board of directors. Gupta allegedly tipped Rajaratnam about Goldman’s earnings and about Warren Buffett’s $5 billion investment in Goldman during the 2008 financial crisis — information that allowed Rajaratnam to make millions in trades before the news became public.

Other insiders included Anil Kumar, a McKinsey director who was paid $1.75 million for tips about McKinsey clients; Danielle Chiesi, a portfolio manager at another hedge fund who traded information with Rajaratnam; and various corporate employees who provided earnings data, merger details, and strategic plans. The network was held together by personal relationships, ethnic and professional ties, and cash payments.

Chapter 5: The FBI Listens In (2008)

The investigation’s breakthrough came when the FBI obtained authorization to wiretap Rajaratnam’s phone — the first time wiretaps had been used in a securities fraud investigation. Traditional white-collar cases relied on document evidence — emails, trading records, financial statements. Wiretaps brought a new dimension: investigators could hear the crimes being committed in real time.

The recordings were devastating. On one call, Rajat Gupta phoned Rajaratnam immediately after leaving a Goldman Sachs board meeting where Warren Buffett’s $5 billion investment had been discussed. Rajaratnam placed trades within minutes. On another call, an Intel insider provided quarterly earnings data before the public announcement. On dozens of calls, Rajaratnam and his sources discussed confidential corporate information with the casualness of people discussing sports scores.

The wiretaps also revealed the culture of Galleon Group. Rajaratnam spoke about his sources with a mixture of pride and entitlement. He didn’t seem to consider what he was doing to be wrong — it was just how the game was played. Everyone on Wall Street had sources. Everyone gathered information. He was just better at it. This attitude — common among the financial elite — would prove catastrophic when the recordings were played for a jury.

Chapter 6: The Takedown — October 16, 2009

At 5:30 AM on October 16, 2009, FBI agents arrived at Rajaratnam’s apartment at the Sutton Place complex in Manhattan. He answered the door in his pajamas. They read him his rights and took him into custody. Simultaneously, agents arrested five other individuals connected to the insider trading ring across New York City.

The arrests were coordinated for maximum impact. Preet Bharara, the US Attorney for the Southern District of New York, held a press conference announcing the charges and describing the case as “the largest hedge fund insider trading case in history.” The message to Wall Street was unmistakable: the era of lax enforcement was over.

Rajaratnam was charged with fourteen counts of conspiracy and securities fraud. He was released on $100 million bail — one of the largest bail amounts in US history. The case immediately became the most talked-about story on Wall Street, with implications that extended far beyond one hedge fund. If Rajaratnam’s network included McKinsey consultants and Goldman Sachs board members, how deep did insider trading really go?

Chapter 7: The Trial — Wiretaps in the Courtroom (2011)

Rajaratnam’s trial began in March 2011 and lasted seven weeks. The prosecution’s strategy was simple: play the tapes. Assistant US Attorney Reed Brodsky and his team played dozens of wiretap recordings for the jury, each one documenting Rajaratnam receiving confidential information and acting on it.

The defense, led by prominent attorney John Dowd, argued that Rajaratnam was a brilliant analyst who traded on legitimate research — “mosaic theory,” the legal practice of combining multiple pieces of public information to reach investment conclusions. The phone calls, Dowd argued, were taken out of context and didn’t prove that the information exchanged was material or nonpublic.

The jury wasn’t persuaded. On May 11, 2011, after twelve days of deliberation, Rajaratnam was found guilty on all fourteen counts. It was the most significant insider trading conviction in decades and validated the government’s aggressive use of wiretap technology in white-collar cases. Rajaratnam showed no visible emotion as the verdict was read.

Chapter 8: The Sentence — Eleven Years (2011)

On October 13, 2011, Judge Richard Holwell sentenced Rajaratnam to eleven years in federal prison — the longest sentence ever imposed for insider trading. The judge cited the “breadth of his illegal activity” and the “corruption of these financial markets” as justifications for the severe sentence. Rajaratnam was also ordered to pay $10 million in criminal fines and $53.8 million in forfeiture.

The SEC separately filed civil charges, resulting in a $92.8 million penalty — the largest ever in an SEC insider trading case. Combined with the criminal forfeiture, Rajaratnam was required to pay nearly $150 million. His personal fortune, estimated at over $1.5 billion at its peak, was severely diminished.

Rajaratnam’s attorneys argued for leniency, citing his charitable work and the fact that no victim was identifiable in the traditional sense — insider trading doesn’t steal from a specific person but rather from the integrity of the market. The judge rejected this argument, noting that the damage to market confidence was itself a form of harm that affected millions of investors who relied on the fairness of the system.

Chapter 9: The Domino Effect — Rajat Gupta and Others (2011–2014)

Rajaratnam’s conviction triggered a cascade of related prosecutions. The most prominent was Rajat Gupta, the former McKinsey managing director who had been one of the most respected business leaders in the world. Gupta was convicted in June 2012 on three counts of securities fraud and one count of conspiracy. He was sentenced to two years in prison.

Gupta’s fall was particularly dramatic. He had been the head of one of the world’s most prestigious consulting firms, served on the boards of Goldman Sachs and Procter & Gamble, and was deeply involved in philanthropy. His conviction destroyed his reputation and raised profound questions about why a man who already had wealth and status would risk everything for relatively modest financial gains. Gupta maintained that he never received any financial benefit from his tips to Rajaratnam — a claim prosecutors disputed.

In total, the Galleon investigation resulted in over 80 arrests and more than 70 convictions. The scope was unprecedented. Traders, analysts, corporate executives, lawyers, and consultants were all caught in the net. The investigation revealed that insider trading was not a rare aberration but a systemic practice that had infiltrated the highest levels of corporate America and Wall Street.

Chapter 10: Prison and Health (2012–2023)

Rajaratnam reported to the Federal Medical Center at Devens, Massachusetts, in December 2012. He was fifty-five years old and in poor health — he had been diagnosed with diabetes and kidney problems that required regular dialysis. His attorneys had argued that prison would be dangerous for someone in his condition, but the judge ruled that the Bureau of Prisons could provide adequate medical care.

Life in federal prison was a dramatic change for a man who had lived in a $10 million Manhattan apartment, traveled by private jet, and managed billions of dollars. Reports described Rajaratnam as a quiet, cooperative inmate who kept largely to himself. His health continued to deteriorate, requiring a kidney transplant that was performed at an outside medical facility.

Rajaratnam was released from prison in 2023 after serving approximately eleven years. He emerged into a financial world that had been fundamentally changed by his case. Compliance departments at major financial institutions had been expanded dramatically. Communication surveillance was standard practice at hedge funds and banks. The legal and cultural boundaries around information gathering had been redrawn. Whether these changes had actually reduced insider trading or simply driven it further underground was debatable.

Chapter 11: The Systemic Question — How Deep Does It Go?

The Rajaratnam case forced Wall Street and the broader financial industry to confront an uncomfortable question: is insider trading a rare crime committed by a few bad actors, or is it a systemic feature of how financial markets actually work?

The evidence suggested the latter. Rajaratnam’s network included people at every level of the financial ecosystem — company boards, management consultancies, hedge funds, investment banks. The information flowed through personal relationships, professional networks, and cultural communities. It was not a conspiracy orchestrated by a criminal mastermind but a diffuse network of mutual back-scratching that had evolved organically over decades.

Academic research supports this view. Studies of trading patterns around corporate announcements consistently find abnormal activity — volume spikes, unusual options trading, price movements — in the days before major announcements, suggesting that material nonpublic information is being traded on far more frequently than enforcement actions would suggest. Rajaratnam wasn’t an anomaly. He was just the one who got caught.

Chapter 12: Legacy — The Man Who Proved Wall Street’s Dirty Secret

Raj Rajaratnam’s legacy is defined by what his prosecution revealed about the financial system. The case demonstrated that the line between legal information gathering and insider trading is crossed routinely by sophisticated market participants. It proved that wiretap technology could be effectively deployed against white-collar criminals. And it resulted in the longest prison sentence ever imposed for insider trading.

But the deepest legacy is the question it left unanswered: did anything actually change? Galleon Group was shut down. Dozens of traders and executives went to prison. Compliance costs across the financial industry increased by billions. But human nature — the desire for an edge, the willingness to rationalize unethical behavior, the tribal loyalty that makes people share secrets with their networks — hasn’t changed.

Rajaratnam’s personal fortune, once estimated at over $1.5 billion, was largely consumed by legal fees, fines, and forfeiture. He spent over a decade in prison and emerged with a destroyed reputation and diminished health. The price was high. Whether the deterrent effect justified the cost — whether the next Raj Rajaratnam looks at that outcome and decides the edge isn’t worth the risk — is the question that will determine whether the Galleon case was a turning point or just an expensive cautionary tale that the next generation of ambitious traders will ignore.

💡 Key Insights

- ▸ The Rajaratnam case was the first to use wiretaps in a white-collar securities fraud investigation, fundamentally changing how Wall Street crimes are prosecuted. The recordings made the case unwinnable for the defense.

- ▸ Rajaratnam's network extended into the highest levels of corporate America — board members, executives, consultants. The case revealed that insider trading wasn't a fringe activity but a systemic practice among sophisticated investors.

- ▸ The eleven-year sentence sent a message that insider trading would be punished like violent crime. Whether it actually deterred the practice or just made practitioners more careful is an open question.