Bill Hwang: The Church-Going Trader Who Vaporized $36 Billion

He was a devout Christian who tithed millions. He was also a Wall Street gambler who placed the most reckless bets in financial history. When Bill Hwang's family office imploded in March 2021, it triggered the largest margin call ever, destroyed two banks, and left the world asking: how did nobody see this coming?

View all stories about this mogul

🙏 Chapter 1: The Believer

Sung Kook “Bill” Hwang was a man of contradictions so extreme they almost felt performative.

On Sunday mornings, he attended Grace and Mercy Church in Manhattan — a small Korean Christian congregation where he sang hymns, prayed fervently, and donated millions. He funded Christian media ventures. He supported missionaries. He named his investment firm “Archegos” — Greek for “leader” or “author,” a term used in the New Testament to describe Jesus.

On Monday mornings, he made leveraged bets of such staggering recklessness that they would have made a Las Vegas pit boss nervous.

Born in South Korea in 1964, Hwang emigrated to the United States as a teenager. His father was a pastor — a detail that adds either poignancy or irony to the story, depending on your perspective. Hwang attended UCLA and then Carnegie Mellon University for business school.

After Carnegie Mellon, he joined Hyundai Securities and then moved to Peregrine Financial Group before landing at Tiger Management — Julian Robertson’s legendary hedge fund, one of the most respected investment firms of the 1990s.

“At Tiger, Hwang learned two things: how to analyze stocks with extraordinary depth, and how to bet with extraordinary conviction. The first skill made him brilliant. The second skill made him dangerous.”

Robertson’s Tiger Management was famous for its “Tiger Cubs” — junior portfolio managers who were trained in Robertson’s concentrated, high-conviction investment style and then spun out to launch their own funds. Hwang was one of the most successful cubs.

In 2001, Hwang launched Tiger Asia Management, a hedge fund focused on Asian equities. The fund was successful — at its peak, it managed approximately $8 billion. Hwang was respected in the industry as a skilled stock picker with deep knowledge of Asian markets.

Then, in 2012, it all went sideways.

🚨 Chapter 2: The First Fall

In December 2012, Tiger Asia Management pleaded guilty to insider trading charges related to Chinese bank stocks. The SEC alleged that Hwang had traded on material, non-public information obtained from private placement offerings.

The penalty was $44 million — a substantial fine, but not a career-ender. However, as part of the settlement, Hwang agreed to convert Tiger Asia from a hedge fund to a family office. This meant he would no longer manage outside investors’ money. He would only manage his own.

This distinction — hedge fund versus family office — would prove to be the most consequential regulatory detail in modern financial history.

Hedge funds are subject to extensive regulation. They must register with the SEC. They must disclose their holdings. They must report to investors. They face leverage limits and compliance requirements.

Family offices are exempt from virtually all of this. Because they manage only the family’s own money, regulators largely leave them alone. No disclosure requirements. No registration. No leverage limits. No oversight.

Bill Hwang had just been given the keys to the most unregulated vehicle in the financial system.

“When Hwang converted from a hedge fund to a family office, regulators thought they were punishing him. They were actually liberating him. He could now trade with no disclosure, no oversight, and no limits. It was like grounding a teenager and then handing them the keys to a Ferrari.”

Hwang renamed his family office Archegos Capital Management. He started with approximately $200 million of his own money. Over the next nine years, he would turn that $200 million into $36 billion.

And then he would lose it all in two days.

📈 Chapter 3: The Leverage Machine

Archegos’ strategy was simple in concept and terrifying in execution: take concentrated positions in a small number of stocks, lever them up as much as possible, and ride the momentum.

But Hwang didn’t buy stocks directly. He used a financial instrument called a “total return swap” — a derivative contract where a bank agrees to pay Hwang the return on a stock (including price appreciation and dividends) in exchange for a fee. The bank buys the actual stock to hedge its exposure.

The beauty of the total return swap, from Hwang’s perspective, was anonymity. When you buy stock directly, you must file public disclosures once you own more than 5% of a company. When you hold the same economic exposure through a swap, you don’t have to disclose anything. The bank owns the stock on paper. Hwang’s name never appears.

This allowed Hwang to quietly amass enormous positions without anyone — regulators, other investors, or the companies themselves — knowing.

How enormous? By March 2021, Archegos held leveraged positions worth approximately $160 billion. On a capital base of roughly $36 billion. That’s 4-5x leverage on the entire portfolio.

The positions were concentrated in a handful of stocks: ViacomCBS, Discovery, Baidu, Tencent Music, GSX Techedu, and a few others. In some cases, Hwang effectively controlled 50% or more of a company’s freely traded shares — a position so large that unwinding it would be virtually impossible without crashing the stock price.

“Imagine owning half the float of a stock through hidden derivatives, leveraged 5 to 1. If the stock goes up 10%, you make 50% on your capital. If the stock goes down 10%, you lose 50% of your capital. And if the stock goes down 20%, you’re wiped out. That was Archegos’ position. In multiple stocks. Simultaneously.”

The banks that provided these swaps — Goldman Sachs, Morgan Stanley, Credit Suisse, Nomura, Deutsche Bank, UBS, and others — each knew about their own exposure to Hwang. But none of them knew the total picture. Each bank thought it was managing a reasonable risk. The aggregate risk was catastrophic.

💣 Chapter 4: The Margin Call

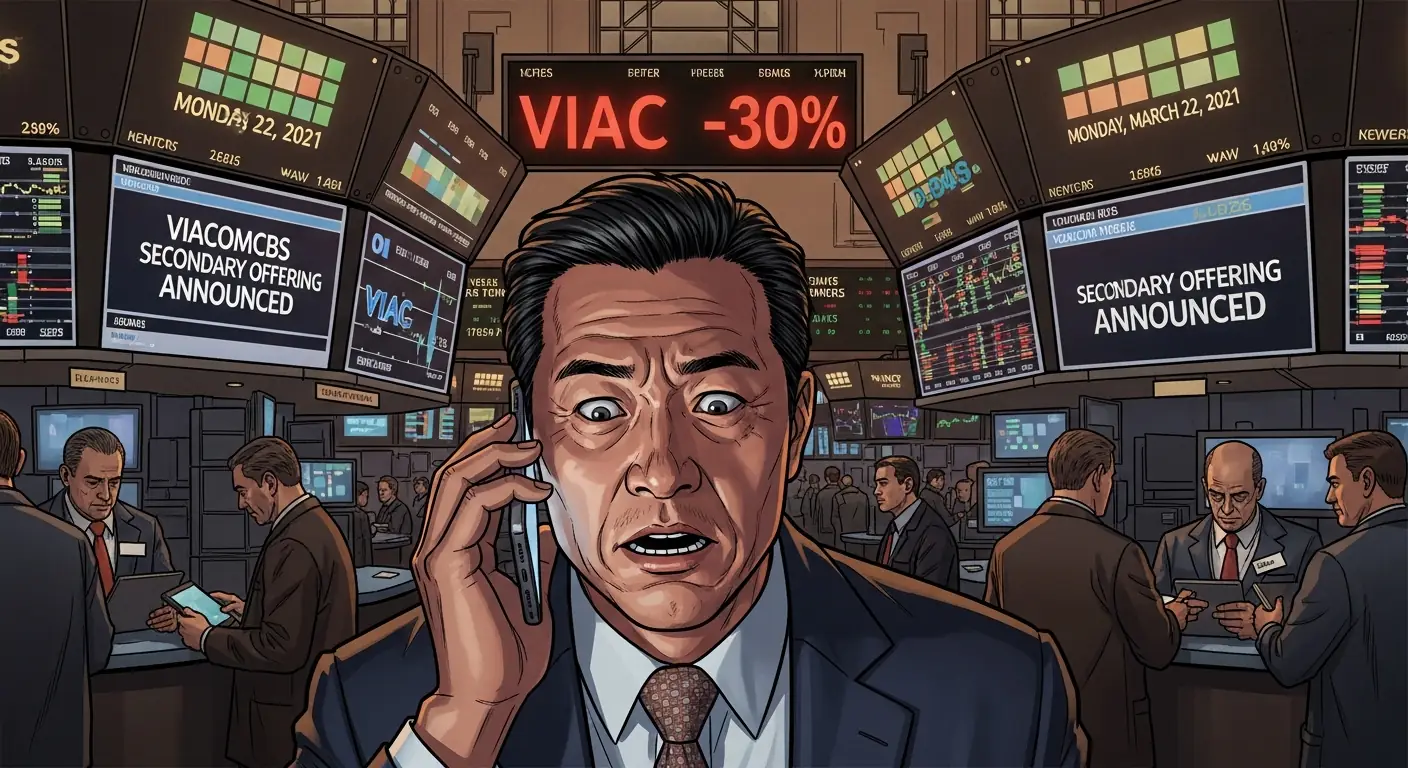

On Monday, March 22, 2021, ViacomCBS announced a secondary stock offering — issuing new shares to raise capital. The announcement diluted existing shareholders and put downward pressure on the stock price.

ViacomCBS dropped 9% on the announcement. For most investors, a 9% decline is annoying but manageable. For Archegos, which held a leveraged position equivalent to billions of dollars of ViacomCBS stock, it was the beginning of the end.

The decline triggered margin calls from Archegos’ prime brokers. Banks demanded that Hwang post additional collateral to cover the losses on his positions. Hwang couldn’t post enough collateral. The losses were too large and the positions were too concentrated.

On Thursday, March 25, Goldman Sachs and Morgan Stanley began liquidating Archegos’ positions. They did so aggressively — dumping billions of dollars of stock onto the market in massive block trades. They moved first because they understood what was about to happen: a death spiral.

“Goldman and Morgan Stanley were the smart ones. They liquidated fast and took relatively small losses. Credit Suisse and Nomura hesitated — and that hesitation cost them everything.”

Credit Suisse and Nomura did not act as quickly. They tried to negotiate with Hwang. They tried to manage the unwind gradually. While they delayed, the stocks kept falling, the losses kept mounting, and the hole kept getting deeper.

On Friday, March 26, the stocks in Archegos’ portfolio collapsed. ViacomCBS fell 27%. Discovery fell 27%. Baidu fell 9%. Tencent Music fell 18%. Billions of dollars in market value evaporated in a single day.

When the dust settled, Archegos’ $36 billion in capital was gone. Completely. Every dollar.

🏦 Chapter 5: The Banking Carnage

The damage extended far beyond Archegos.

Credit Suisse lost approximately $5.5 billion from its Archegos exposure. The loss — which came on top of the bank’s earlier losses from the Greensill Capital collapse — devastated Credit Suisse’s investment bank. Several senior executives were fired. The bank’s stock price cratered. The Archegos disaster was a primary factor in Credit Suisse’s eventual acquisition by UBS in 2023 — effectively the death of a 167-year-old institution.

Nomura lost approximately $3 billion. The Japanese bank’s prime brokerage business was permanently scarred.

Morgan Stanley lost approximately $911 million — a significant but manageable sum, thanks to its early liquidation.

Goldman Sachs lost approximately $10 million — a testament to the speed and ruthlessness of its risk management.

UBS and Deutsche Bank reported smaller losses.

Total banking losses from the Archegos collapse: approximately $10 billion.

“Archegos didn’t just blow up a family office. It blew up a bank. Credit Suisse — one of the oldest and most prestigious banks in the world — was fatally wounded by its relationship with a single client. One client. $5.5 billion in losses. That’s not a risk management failure. That’s an institutional suicide.”

The disparity in losses between the banks revealed a stark truth about risk management on Wall Street: the banks that moved first suffered least. Goldman and Morgan Stanley, both of which had strong risk management cultures, recognized the danger early and acted decisively. Credit Suisse and Nomura, which had weaker risk cultures and were more dependent on Archegos’ lucrative trading fees, hesitated — and paid catastrophically.

⚖️ Chapter 6: The Trial

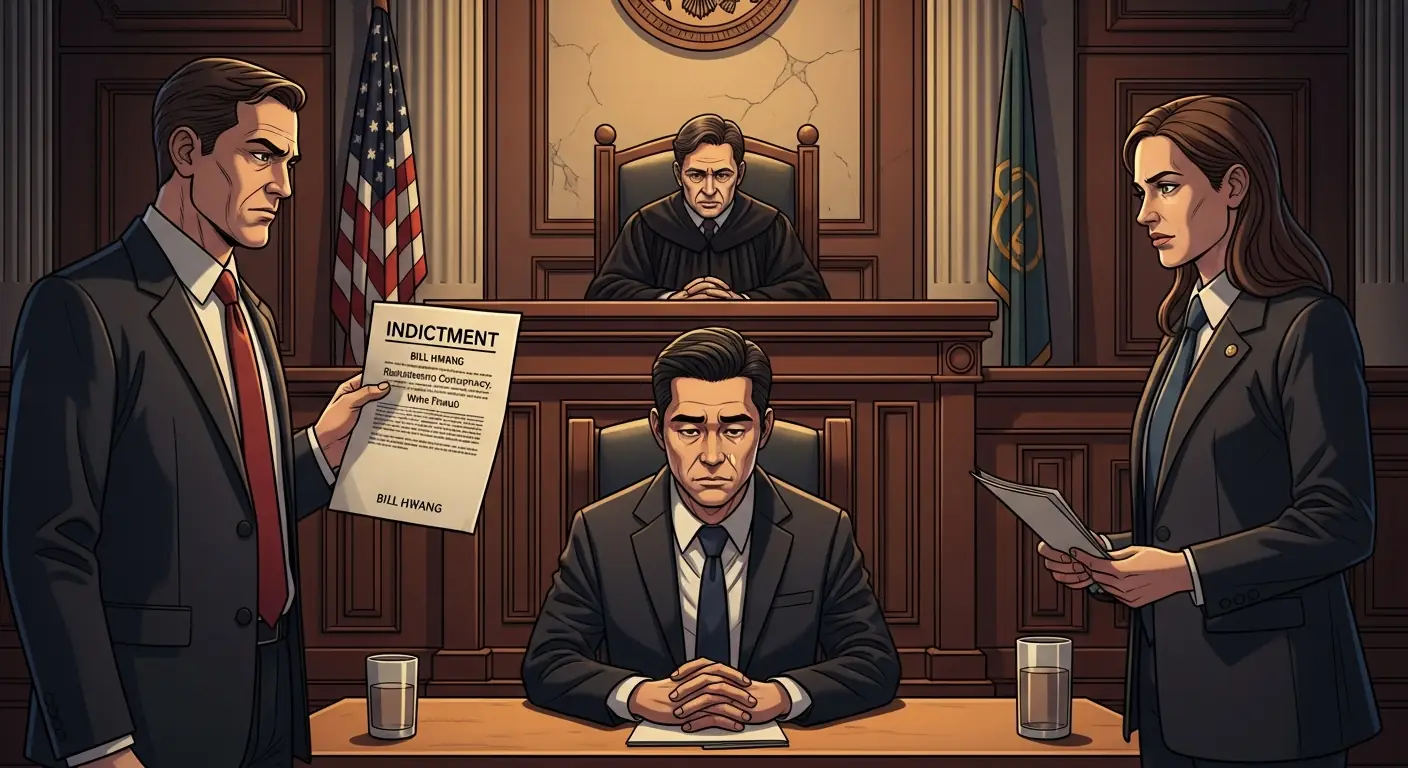

On April 27, 2022, federal prosecutors indicted Bill Hwang on charges of racketeering conspiracy, securities fraud, and wire fraud. The indictment alleged that Hwang had manipulated stock prices through his concentrated positions and lied to his banks about the extent of his trading.

Hwang pleaded not guilty. His defense argued that he was a legitimate investor who had made concentrated bets — as many successful investors do — and that the banks knew exactly what they were doing when they extended him credit.

The trial, held in federal court in Manhattan in 2024, was one of the most closely watched financial cases in years. It pitted prosecutors — who portrayed Hwang as a market manipulator who deceived his banks and distorted stock prices — against defense attorneys who argued that Hwang’s trades were legal, that the banks were willing participants, and that the losses were the result of a market downturn rather than fraud.

In July 2025, Bill Hwang was found guilty on all counts — 10 counts of securities fraud and one count of racketeering conspiracy. He faced decades in prison.

“The Hwang verdict sent a clear message: using derivatives to build hidden positions that manipulate stock prices is fraud, regardless of how sophisticated the instruments or how willing the counterparties. But the message came after $10 billion in losses and the destruction of a major bank. Justice arrived, but not before the damage was done.”

Patrick Halligan, Archegos’ chief financial officer, was also convicted.

The trial revealed in painful detail how Hwang had operated: building massive positions through swaps at multiple banks, each of which was unaware of his total exposure. He held regular “risk meetings” with bank representatives where, prosecutors alleged, he systematically understated his positions and overstated his diversification.

🕳️ Chapter 7: The Systemic Blind Spot

The Archegos collapse raised questions that regulators are still grappling with years later.

How could one family office accumulate $160 billion in leveraged positions without anyone noticing?

The answer is the regulatory framework itself. Family offices are exempt from SEC registration and disclosure requirements. Banks are not required to share information about their clients’ positions with each other or with regulators. The derivatives Hwang used — total return swaps — were not subject to the same disclosure rules as direct stock ownership.

The system was designed to be blind.

How could banks extend so much credit to a single client?

Greed. Archegos was incredibly profitable for its prime brokers. The fees, commissions, and financing charges that Hwang paid generated tens of millions of dollars per year for each bank. Relationship managers who brought in Hwang’s business were heroes within their firms. Risk managers who raised concerns were overruled.

“The banks weren’t victims. They were accomplices. They knew Hwang was running concentrated, leveraged positions. They knew he had a prior conviction for insider trading. They knew the risks. They extended credit anyway because the fees were too good to pass up.”

Has anything changed?

Some things. The SEC proposed new rules requiring family offices and hedge funds to report their swap positions, closing the disclosure gap that Hwang exploited. Banks tightened their prime brokerage risk management (at least temporarily). Credit Suisse no longer exists as an independent entity.

But the fundamental incentive structure — where banks earn fees by extending leverage and relationship managers are rewarded for growing client balances — remains largely intact. The next Bill Hwang may already be building positions that no one can see.

🙏 Chapter 8: God, Money, and Contradiction

The religious dimension of Bill Hwang’s story resists easy interpretation.

Hwang was, by all accounts, genuinely devout. He donated millions to Christian causes. He funded the Fuller Theological Seminary. He supported Christian media ventures, including a Christian broadcasting company in Korea. He spoke publicly about his faith and the role of God in his investment decisions.

He named his firm Archegos — a New Testament term for Jesus.

And then he used that firm to build hidden positions of such reckless size that their collapse destroyed a 167-year-old bank and vaporized tens of billions of dollars in wealth.

“The contradiction between Hwang’s professed faith and his financial conduct is not as simple as hypocrisy. Many devout people compartmentalize their lives — adhering to strict moral codes in some domains while operating by entirely different rules in others. Hwang may have genuinely believed that his trading was legitimate while simultaneously engaging in practices that a jury would later call fraud.”

Or perhaps it was simpler than that. Perhaps Hwang believed that God was on his side. That his extraordinary run of profits — turning $200 million into $36 billion in less than a decade — was evidence of divine favor. That the markets were his ministry and his returns were his testimony.

This kind of prosperity theology — the belief that financial success is a sign of God’s blessing — is common in certain Christian circles, particularly in Korean-American evangelical communities. If you believe God wants you to be rich, then every profitable trade confirms your faith and every risk is sanctified by divine will.

It’s a dangerous theology for a trader with access to unlimited leverage.

🏆 Chapter 9: Lessons from the Abyss

The Archegos story is, at its core, a story about leverage, concentration, and the failure of systems designed to prevent exactly this kind of disaster.

Lesson 1: Leverage kills.

A $200 million portfolio with no leverage is a rich person’s account. A $200 million portfolio leveraged to $160 billion is a weapon of mass financial destruction. The difference between the two is the margin call. Leverage amplifies gains until the moment it amplifies losses, and that moment always comes.

Lesson 2: Concentration is not conviction — it’s recklessness.

Hwang’s positions were so concentrated that he effectively controlled the markets for several stocks. This made his gains enormous on the way up and his losses catastrophic on the way down. True conviction means having a well-researched thesis. Concentration at Archegos’ level means having a death wish.

Lesson 3: Opacity is risk.

The total return swap structure that allowed Hwang to hide his positions wasn’t just a legal loophole — it was a systemic risk multiplier. When no one can see the total picture, no one can assess the total risk. Transparency isn’t just about regulation — it’s about survival.

Lesson 4: Banks follow fees, not risk.

Every bank that extended credit to Archegos knew about Hwang’s insider trading conviction. They extended credit anyway because the fees were lucrative. Risk management is only as strong as the willingness of senior executives to forgo revenue.

Lesson 5: The biggest risks are the ones you can’t see.

The financial system’s near-miss with Archegos happened not because people took visible risks but because massive risks were invisible. The swaps were hidden. The leverage was hidden. The concentration was hidden. The next crisis will probably also come from something no one can see.

“Bill Hwang turned $200 million into $36 billion and then back to zero. The round trip took about nine years. Somewhere in that story is everything you need to know about Wall Street: the brilliance, the greed, the blindness, and the inevitability of the crash.”

Bill Hwang, the church-going trader from South Korea, is currently awaiting sentencing. He faces decades in prison. His fortune is gone. His firm is dissolved. Credit Suisse is gone. And the regulatory gaps he exploited remain only partially closed.

It’s a parable. Whether it’s about faith, greed, regulation, or human nature depends on which part of the story you read most carefully.

The answer, of course, is all of the above.

Bill Hwang was convicted on all counts in July 2025 and awaits sentencing. Archegos Capital Management was dissolved. Credit Suisse was acquired by UBS in June 2023 for approximately $3.2 billion. Total banking losses from the Archegos collapse exceeded $10 billion.

🤫 Chapter 10: The Quiet Empire Builder (2013-2020)

After the 2012 insider trading scandal and the forced conversion of Tiger Asia into Archegos Capital Management, Bill Hwang wasn’t exactly banished to a financial Siberia. No, he was given the keys to a private island, metaphorically speaking. With a starting capital of roughly $200 million of his own money, Hwang embarked on a journey that would see that sum balloon into an estimated $36 billion in just under a decade. How did he do it? It wasn’t through sheer luck, folks. It was a methodical, almost stealthy accumulation of power, built on deep market insight, relentless leverage, and a rather peculiar form of financial sorcery known as total return swaps.

From Exile to Enigma

Hwang, a seasoned “Tiger Cub” from Julian Robertson’s legendary Tiger Management, hadn’t lost his fundamental analytical chops. He still possessed an uncanny ability to spot undervalued companies, particularly in the burgeoning Asian tech and media sectors. While many in the institutional world might have viewed him with suspicion after his SEC settlement, Hwang was busy proving that past indiscretions don’t necessarily preclude future astronomical returns – at least, not for himself. He focused on a concentrated portfolio of high-growth stocks, making massive bets on companies like Tencent Music Entertainment, Baidu, ViacomCBS, Discovery, and Farfetch. These weren’t penny stocks; these were major players, and Hwang was building positions so large they would have made institutional investors blush. His strategy was simple: find companies he believed in, and then bet the farm, the barn, and a few neighboring farms too.

The Swap Secret

The real secret sauce, the clandestine ingredient that allowed Hwang to become a titan without anyone truly noticing, was the total return swap (TRS). Imagine you want to own a huge chunk of a company’s stock, but you don’t want anyone to know you own it, and you also don’t want to tie up all your cash. Enter the TRS. Instead of buying the shares directly, Hwang would enter into agreements with investment banks (his “prime brokers”). The banks would buy the shares, and Hwang would pay them a fee plus any interest, while receiving the returns (or losses) on the underlying stock. Crucially, the shares remained on the banks’ balance sheets, not Archegos’. This meant Hwang avoided triggering disclosure rules that require investors to publicly reveal stakes exceeding 5% in a company. He could amass positions that were, in some cases, over 20% of a company’s outstanding shares without a peep. It was financial invisibility, and it was glorious… until it wasn’t.

The Banks’ Blind Trust (or Greed)

How did a man with a track record of insider trading convince the world’s most sophisticated financial institutions to essentially bankroll his ghost empire? Simple: money talks, and Hwang was generating a lot of it for his prime brokers in the form of fees and interest payments. Banks like Goldman Sachs, Morgan Stanley, Credit Suisse, Nomura, and UBS were locked in a fierce competition for Archegos’ lucrative business. Each bank, blinded by the promise of hefty commissions and perhaps a bit of hubris, was happy to extend credit and facilitate Hwang’s TRS positions. None of them had a complete picture of his overall leverage across all his brokers. They only saw their piece of the pie, assuming their individual exposure was manageable. It was a classic case of collective shortsightedness, where the allure of a whale client overshadowed basic risk management, creating a ticking time bomb built by many hands.

🤝 Chapter 11: The Enabler Network (2015-2021)

While Bill Hwang was busy conjuring billions out of thin air with his total return swaps, he wasn’t doing it alone. He had a willing network of enablers: the world’s most prestigious (and, as it turned out, sometimes remarkably naive) investment banks. This wasn’t a conspiracy in the traditional sense, but rather a perfect storm of intense competition, opaque financial instruments, and a collective failure of risk management that allowed Archegos to become a systemic threat. It was like a high-stakes poker game where every player thought they were the only one at the table, unaware that the pot was already far too big for anyone to cover.

The Golden Ticket Client

For any prime brokerage division at a major investment bank, a client like Archegos was a “whale.” Hwang’s active trading, his huge positions, and his seemingly consistent (for a time) returns generated significant revenue. We’re talking millions upon millions in fees, often dwarfing what smaller, less active clients would bring in. Goldman Sachs, Morgan Stanley, Credit Suisse, Nomura, UBS, Deutsche Bank, Wells Fargo – they all wanted a piece of that action. The internal pressure to land and retain such a lucrative client was immense. “Yes, he had that insider trading thing,” a sales executive might have mumbled, “but look at the volume! Look at the fees!” This short-term focus on revenue often eclipsed the long-term view of risk. Hwang, a master of cultivating these relationships, knew exactly how to play the banks against each other, dangling the promise of more business to whichever firm offered the most favorable terms and the least intrusive questions.

A House of Cards, Many Hands Building

The true genius (or madness, depending on your perspective) of Archegos’ strategy was that Hwang didn’t just use one bank for his swaps. He used many. Each bank effectively held a synthetic position for Archegos, believing they had a manageable, diversified slice of his portfolio. What they didn’t know was that their competitors were holding equally massive, and often identical, slices. It was like a dozen chefs all baking the same giant cake, each thinking they were only responsible for a single serving, unaware that the whole thing was collapsing under its own weight. This complete lack of transparency across prime brokers was the critical flaw. There was no central clearinghouse for these over-the-counter (OTC) derivatives, and no mechanism for banks to share client exposure data. So, when Archegos had, say, $10 billion in ViacomCBS exposure, each bank might have thought they had only $1 billion, utterly oblivious that nine other banks were holding another $9 billion.

Trust, But Verify? Nah.

The banks’ risk management systems, designed to prevent single-client overexposure, utterly failed here. They relied on their own individual data points, operating in silos. The competitive drive meant they were hesitant to ask Hwang about his other brokers, fearing he might take his business elsewhere. And Hwang, under no legal obligation to disclose his overall leverage, certainly wasn’t volunteering the information. This combination of intense competition, the opaque nature of total return swaps, and a fundamental breakdown in cross-firm information sharing created a scenario where billions of dollars in highly concentrated, highly leveraged positions could accumulate unnoticed. It wasn’t just a failure of Bill Hwang; it was a spectacular, multi-billion-dollar failure of the entire prime brokerage ecosystem to “trust, but verify.” Or, more accurately, to “trust, and then just hope for the best.”

💥 Chapter 12: The Fallout Beyond the Banks (2021-Present)

While the headlines screamed about the multi-billion dollar losses at Credit Suisse, Nomura, and Morgan Stanley, the Archegos implosion wasn’t just a banking problem. Oh no, friends. When a fund the size of Archegos, with positions often representing 10% to 20% of a company’s shares, gets margin called, the fallout ripples far beyond the prime brokers. It sent shockwaves through specific sectors of the stock market, caught other unsuspecting investors in the crossfire, and left a trail of questions about market stability and regulatory oversight that continue to linger. It was a financial earthquake, and while the banks felt the initial tremors most acutely, the aftershocks hit everyone connected to Hwang’s chosen stocks.

Collateral Damage: The Stock Market

The last week of March 2021 was a bloodbath for a specific basket of stocks that Archegos held. As the prime brokers scrambled to liquidate Hwang’s positions to cover their margin calls, they dumped massive blocks of shares onto the market. We’re talking unprecedented volumes. ViacomCBS (VIAC), which had been trading around $90 a share, plummeted by over 50% in a single week. Discovery (DISCA) suffered a similar fate, seeing its stock price halve. Chinese tech giants like Baidu (BIDU) and Tencent Music Entertainment (TME) also saw dramatic, sudden drops. This wasn’t just a bad day; it was a systemic shock for these companies, erasing billions in market capitalization in a flash. Other investors—pension funds, mutual funds, retail traders—who held these “Bill Hwang stocks” were caught entirely off guard, watching their portfolios evaporate through no fault of their own. It was a stark reminder that even seemingly stable, large-cap stocks can be victims of extreme, hidden leverage.

The Ghost of Archegos: Empty Offices and Scrutiny

What happened to the actual Archegos Capital Management? Poof. Gone. The offices were emptied, the website taken down, and the roughly 50 employees were left scrambling, many likely unaware of the full extent of the financial brinkmanship they were part of until it was too late. But the immediate collapse of the firm was just the beginning. The Archegos debacle instantly ignited a fierce debate about the opaque world of family offices. Regulators had intentionally exempted family offices from the stringent reporting requirements imposed on hedge funds, believing they posed no systemic risk since they managed only private wealth. Archegos proved that belief catastrophically wrong. Suddenly, family offices—which manage trillions of dollars globally—were under an intense, albeit often fleeting, spotlight. Were they the next unregulated shadow banking system? The question hung heavy in the air, creating unease among the wealthy elite who enjoyed these very same exemptions.

A Call for Transparency (Mostly Unanswered)

In the immediate aftermath, there were loud calls for greater transparency in the over-the-counter derivatives market, particularly for instruments like total return swaps. Regulators, including the SEC, vowed to investigate and implement reforms. The idea was to prevent another Archegos by ensuring that prime brokers had a clearer picture of a client’s overall exposure. However, enacting significant regulatory change is a notoriously slow and complex process, often bogged down by lobbying efforts and the sheer global nature of financial markets. While some proposals have been floated, such as requiring large security-based swap positions to be publicly reported, the speed and comprehensiveness of these reforms remain debated. The Archegos saga highlighted how easily innovation (or, perhaps, regulatory arbitrage) can outpace oversight, leaving the financial system vulnerable to the next clever, and catastrophic, leverage machine.

🔮 Chapter 13: The Lingering Shadow & His Future (2021-Present)

The dust has largely settled on the immediate financial carnage of the Archegos meltdown, but the story of Bill Hwang is far from over. His personal future, the broader implications for financial regulation, and the enduring lessons of unchecked ambition continue to cast a long shadow over Wall Street. From a church pew to a courtroom, Hwang’s journey embodies a profound contradiction that challenges our understanding of faith, risk, and responsibility in the high-stakes world of finance. The question isn’t just “how did it happen?” but “what have we truly learned, and could it happen again?” (Spoiler alert: probably).

Bill Hwang Today: Awaiting Judgment, Not Redemption

In April 2022, Bill Hwang was arrested and charged with racketeering conspiracy, securities fraud, and wire fraud. He pleaded not guilty to all charges, maintaining his innocence and arguing that his actions were not illegal, but rather standard (if aggressive) market practices. His legal battle has been a protracted affair, with his defense arguing that the “swaps” weren’t “securities” in the traditional sense, and therefore, he couldn’t have committed securities fraud by manipulating their prices. As of late 2023, the trial is ongoing, with his fate hanging in the balance. Should he be convicted, Hwang could face decades in prison. Despite the catastrophic losses, Hwang reportedly still retains a substantial personal fortune, though nowhere near his peak of $36 billion. He continues to attend his Grace and Mercy Church, a silent testament to a faith that, for many, remains irreconcilable with the financial devastation he wrought.

The Archegos Effect: A Regulatory Reckoning (or Lack Thereof)

The Archegos collapse was a potent, multi-billion-dollar alarm bell that exposed a critical blind spot in financial regulation: the family office loophole. In response, the U.S. Securities and Exchange Commission (SEC) in late 2022 proposed new rules that would require large security-based swap positions to be reported publicly. This “sunlight” rule aims to prevent another Archegos by making it impossible for an entity to build massive, hidden leverage across multiple banks. However, implementing these rules is a complex dance, often slowed by industry lobbying and the sheer difficulty of coordinating global financial oversight. While the Archegos incident certainly fueled discussions about bringing family offices under greater scrutiny, the political will to fully close the exemption remains elusive. The reality is that many powerful, wealthy families benefit from this very same lack of oversight, making comprehensive reform a challenging uphill battle.

A Billion-Dollar Fable for the Modern Age

The legacy of Bill Hwang and Archegos is a multi-layered cautionary tale. It’s a story of how an individual’s unchecked ambition, coupled with sophisticated but opaque financial instruments, can exploit regulatory gaps to create systemic risk. It’s also a story about the perpetual tension between innovation and oversight, and the timeless lure of easy money for institutions that should know better. The Archegos meltdown serves as a stark reminder that even in an era of advanced risk management and sophisticated algorithms, human greed and collective blind spots can still bring down giants. The enduring question is not if another Archegos will emerge, but when, and in what guise. Because as history repeatedly shows, in the high-stakes world of finance, the lessons from the abyss are often forgotten until the next time we’re staring into it.

💡 Key Insights

- ▸ The Archegos collapse exposed a massive blind spot in financial regulation: family offices. Because Hwang was trading through a family office rather than a hedge fund, he was exempt from most disclosure requirements. Banks had no obligation — and no mechanism — to share information about his positions with each other. Each bank saw only its own exposure, not the terrifying totality. The lesson: regulatory gaps don't just create risk for the rule-breakers — they create systemic risk for everyone.

- ▸ Hwang's strategy of using total return swaps to build enormous positions without disclosure was not illegal at the time — it was a perfectly legal exploitation of a regulatory loophole. The banks that enabled these trades were not victims — they were willing participants who earned enormous fees from Hwang's business. The Archegos story is ultimately about the collective failure of an industry that prioritized short-term revenue over long-term risk management.