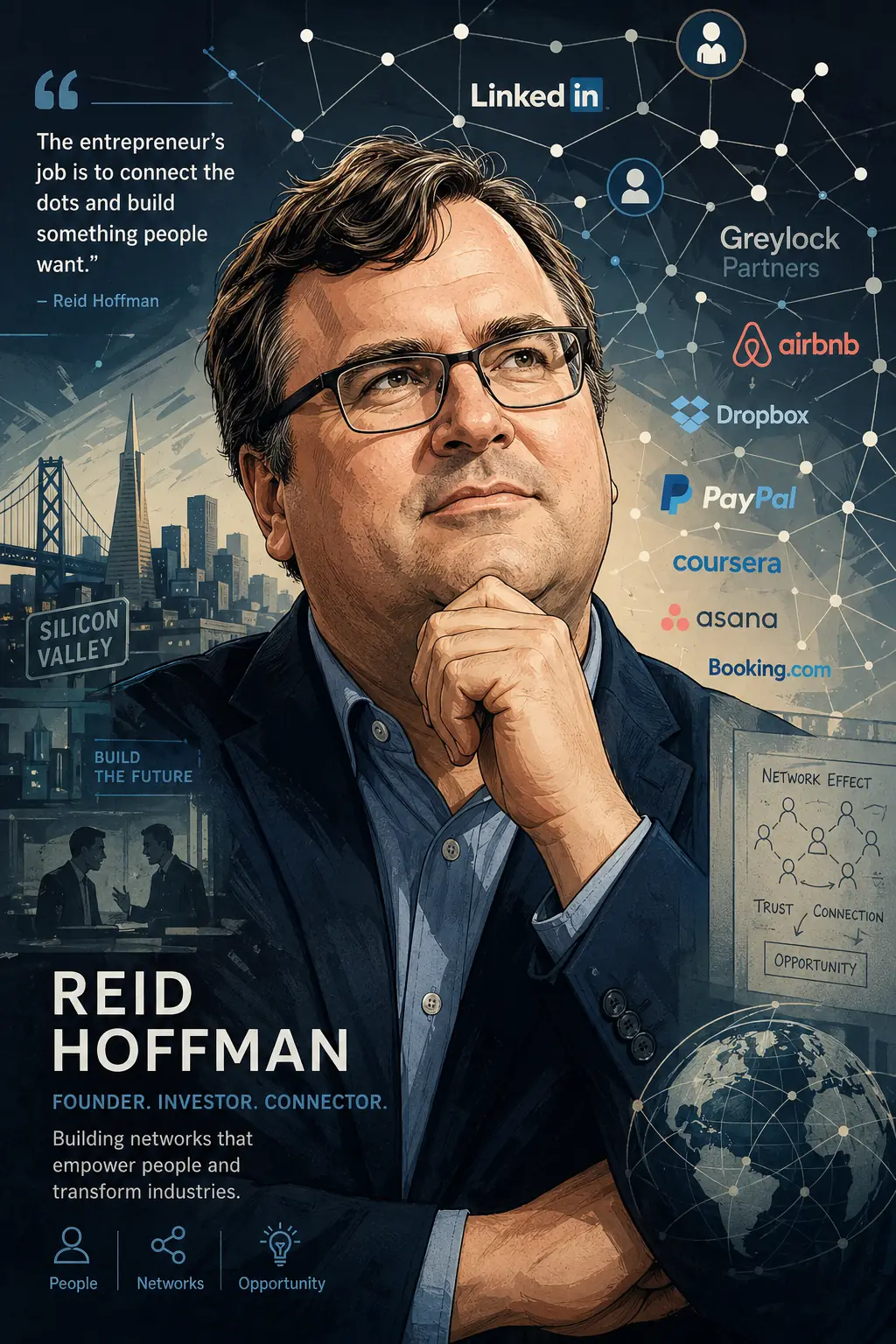

Reid Hoffman: The Oracle of Silicon Valley Who Bet on Networks Before Anyone Else

Before LinkedIn made professional networking a verb, Reid Hoffman was quietly connecting the dots between PayPal, Facebook, and every major startup of a generation.

View all stories about this mogul

Reid Hoffman is the most powerful person in Silicon Valley that most people outside of tech have never heard of. He co-founded LinkedIn, was an early board member of PayPal, was the first outside investor in Facebook, backed Airbnb before it was cool, and became one of the most influential venture capitalists in history — all while maintaining a reputation as genuinely one of the nicest people in an industry not known for niceness. He’s the human embodiment of the network effect he built his fortune on: his value comes not just from what he knows, but from who he connects.

Chapter 1: The Philosopher Who Chose Silicon Valley (1967–1997)

Reid Garrett Hoffman was born on August 5, 1967, in Palo Alto, California — literally in the cradle of Silicon Valley, though the term barely existed yet. His father was a lawyer, his mother a real estate agent. From an early age, Hoffman was the kid who asked questions that made adults uncomfortable. Not troublemaker questions — philosophical ones. Why do people organize themselves the way they do? What makes some groups succeed and others fail? How do ideas spread?

He attended The Putney School in Vermont, a progressive boarding school that emphasized self-directed learning, then went to Stanford University, where he studied symbolic systems — a interdisciplinary program combining philosophy, cognitive science, and computer science. It was the perfect major for someone who wanted to understand how humans think and how machines might think alongside them.

After Stanford, Hoffman did something unexpected for someone in the orbit of Silicon Valley: he went to Oxford University on a Marshall Scholarship to study philosophy. He seriously considered becoming an academic. He wanted to be a public intellectual who shaped how society thought about itself. But he had an epiphany during his time at Oxford: academics write papers that a few hundred people read. Entrepreneurs build products that millions of people use. If you want to change how society works, building things is more effective than theorizing about them.

Chapter 2: The Failures Before the Fortunes (1997–2000)

Hoffman returned to Silicon Valley in 1997 with a philosopher’s mind and an entrepreneur’s ambition. His first venture was SocialNet, a dating and social networking site — years before Friendster, MySpace, or Facebook. The idea was sound: people would create profiles and connect with others based on shared interests, location, and compatibility. The execution was ahead of its time. The internet wasn’t ready. Broadband penetration was low. Digital cameras were rare. Creating a compelling online profile in 1997 was an exercise in frustration.

SocialNet limped along and eventually failed. But Hoffman learned something crucial: the concept of online networking was right. The timing was wrong. And timing, he would later say, is the single most underappreciated factor in startup success. A brilliant idea executed five years too early is indistinguishable from a bad idea. He filed this lesson away.

In 1998, his friend Peter Thiel invited him to join the board of a new company called Confinity, which was building digital payments. Hoffman joined as a board member and then became COO after Confinity merged with Elon Musk’s X.com to form PayPal. At PayPal, Hoffman found himself surrounded by some of the most intense, brilliant, and competitive people in tech — the group that would later be dubbed the “PayPal Mafia.” Thiel, Musk, Max Levchin, David Sacks, Chad Hurley, Steve Chen, Jeremy Stoppelman. The alumni of this one company would go on to found or fund YouTube, Tesla, SpaceX, Yelp, Palantir, LinkedIn, and a dozen other billion-dollar companies.

Chapter 3: LinkedIn — The Network That Changed Work (2002–2004)

Even while working at PayPal, Hoffman was thinking about his next move. The SocialNet failure hadn’t killed his conviction that online networking was transformative — it had refined it. He realized that the highest-value network wasn’t social (that was nice-to-have) but professional (that was need-to-have). People would put real effort into maintaining a professional profile because their careers depended on it.

PayPal went public in February 2002 and was acquired by eBay for $1.5 billion in October of that same year. Hoffman took his payout and immediately started building LinkedIn. The company launched on May 5, 2003, with Hoffman and a small team inviting 350 of their personal contacts. By the end of the first week, they had 4,500 users.

Growth was slow at first — deliberately so. Unlike the social networks that would follow, LinkedIn wasn’t designed for viral, explosive growth. It was designed for steady, professional, high-quality growth. Every connection was supposed to mean something. You didn’t add strangers; you connected with people you actually knew and could vouch for. This made early growth painful but created something that social networks never achieved: trust.

Chapter 4: The Long Game — Building LinkedIn Into a Utility (2004–2008)

While Facebook was capturing headlines with explosive college campus growth and MySpace was dominating pop culture, LinkedIn was doing something less glamorous but arguably more important: becoming essential. Recruiters discovered that LinkedIn was the most efficient way to find candidates. Job seekers discovered it was the most effective way to be found. Salespeople discovered it was the best way to research prospects before meetings.

Hoffman made a critical strategic decision early: LinkedIn would be useful even for people who weren’t actively looking for jobs. By allowing users to build a professional identity, accumulate endorsements, and share industry content, LinkedIn became something people maintained all the time, not just when they were job hunting. This was the difference between a tool you use once and a platform you live on.

Revenue came from three sources: premium subscriptions for job seekers and salespeople, advertising, and talent solutions for recruiters. The talent solutions business was the real money machine. Companies were willing to pay enormous fees for access to LinkedIn’s database of professionals. By 2008, LinkedIn had over 30 million users and was generating significant revenue — all without the drama, controversy, and privacy scandals that plagued its social networking competitors.

Chapter 5: Greylock and the Art of the Angel Investor (2004–2010)

Hoffman didn’t just build LinkedIn. He simultaneously became one of Silicon Valley’s most prolific and successful angel investors. In 2004, a Harvard dropout named Mark Zuckerberg was looking for early funding for a social network called TheFacebook. Peter Thiel wrote the first check — $500,000. But it was Hoffman who helped organize the round, invested his own money, and joined the board of directors.

That single investment would eventually be worth hundreds of millions of dollars. But it wasn’t a one-off. Hoffman invested in Zynga (gaming), Flickr (photos), Digg (news), and dozens of other startups. His investment thesis was deceptively simple: bet on network effects. Any product or platform that becomes more valuable as more people use it has the potential for exponential returns. The math is counterintuitive — a network with 10 users isn’t half as valuable as one with 20 users; it might be ten times less valuable — and most investors didn’t think this way.

In 2009, Hoffman joined Greylock Partners, one of Silicon Valley’s most prestigious venture capital firms. He brought his rolodex, his reputation, and his philosophical approach to investing. At Greylock, he led investments in Airbnb, Dropbox, Coupang, and other companies that would become worth billions. His superpower wasn’t financial modeling or market analysis — it was pattern recognition. He could see the network effects before the network existed.

Chapter 6: The $26.2 Billion Microsoft Deal (2011–2016)

LinkedIn went public in May 2011, and its stock price more than doubled on the first day of trading. It was one of the most successful tech IPOs since Google. But Hoffman knew that LinkedIn faced a strategic challenge: it was dominant in professional networking but vulnerable to disruption from larger platforms. Facebook was encroaching on professional features. Google had launched Google+ with professional networking ambitions. Staying independent meant competing against companies with vastly more resources.

In June 2016, Microsoft CEO Satya Nadella called Hoffman with an offer: Microsoft wanted to acquire LinkedIn for $26.2 billion in cash. It was the largest acquisition in Microsoft’s history and valued LinkedIn at a 50% premium over its stock price. Hoffman, who was chairman of LinkedIn’s board, supported the deal. He saw Microsoft’s enterprise relationships, cloud infrastructure, and global reach as the perfect complement to LinkedIn’s network.

The deal closed in December 2016. Hoffman personally made billions. More importantly, he ensured that LinkedIn’s mission — connecting the world’s professionals — would be backed by one of the world’s most powerful technology companies. Under Microsoft, LinkedIn would grow to over a billion members, becoming the de facto professional identity layer of the internet.

Chapter 7: Masters of Scale — Becoming Silicon Valley’s Philosopher King (2017–2020)

With the Microsoft acquisition complete, Hoffman entered a new phase. He had the money, the network, and the reputation. Now he wanted the influence — not for ego, but because he genuinely believed Silicon Valley needed more thoughtful voices guiding it. He launched “Masters of Scale,” a podcast where he interviewed the world’s most successful entrepreneurs and extracted the principles behind their success.

The podcast was classic Hoffman: intellectual, optimistic, and relentlessly focused on the question of how things scale. Episodes featured Mark Zuckerberg, Eric Schmidt, Sara Blakely, and dozens of others. Hoffman wasn’t just interviewing them — he was synthesizing their experiences into a unified theory of entrepreneurial growth. The podcast became one of the most popular business shows in the world.

He also wrote books — “The Start-up of You,” “The Alliance,” “Blitzscaling” — each one distilling a different aspect of his philosophy. Blitzscaling, co-written with Chris Yeh, argued that in the network age, the optimal strategy is to grow as fast as possible, even at the cost of efficiency, because the first company to achieve network dominance usually wins everything. The book was both a descriptive analysis and a prescriptive playbook, and it influenced an entire generation of founders and investors.

Chapter 8: The AI Bet — From Networks to Intelligence (2020–2023)

Hoffman saw artificial intelligence coming before most of Silicon Valley took it seriously. Through Greylock, he had invested in AI companies for years. But in 2023, he made his most consequential AI move: he co-founded Inflection AI with Mustafa Suleiman, the co-founder of DeepMind. Their goal was to build a personal AI assistant — a conversational AI called Pi that would be empathetic, helpful, and accessible to everyone.

Inflection raised $1.5 billion from Microsoft, Bill Gates, Eric Schmidt, and others. It was one of the largest fundraises in AI history. Hoffman’s pitch was that AI would be the next great network effect: the more people used conversational AI, the better it would get, and the more indispensable it would become. He saw AI not as a replacement for human connection but as an amplifier of it.

But the AI gold rush created uncomfortable questions. Hoffman was simultaneously on the board of Microsoft (LinkedIn’s parent company and OpenAI’s largest investor) and co-founding a company that competed with OpenAI. The conflicts of interest were labyrinthine. In early 2024, Hoffman stepped down from Microsoft’s board, and Inflection AI’s team — including Suleiman — was largely absorbed into Microsoft. The startup had essentially been an expensive acqui-hire.

Chapter 9: Political Ambitions and Controversies (2016–2024)

Hoffman was one of Silicon Valley’s most prominent Democratic donors and political operatives. He poured millions into supporting candidates, funding political organizations, and fighting what he saw as threats to democracy. After the 2016 election, he became especially active, funding organizations that fought misinformation and supported voter registration.

But his political activities also generated controversy. In 2018, it was revealed that a firm Hoffman had funded had conducted a disinformation experiment during the 2017 Alabama Senate special election, creating fake social media accounts to test the impact of political misinformation. Hoffman said he hadn’t known about the specific tactics and apologized, but the episode was deeply embarrassing for someone who had positioned himself as a champion of truth and democratic norms.

His association with Jeffrey Epstein also drew scrutiny. Hoffman had met with Epstein on multiple occasions and had facilitated introductions between Epstein and other tech figures, including Elon Musk. After Epstein’s arrest and death, Hoffman apologized for the association, saying he had been “duped” and that the meetings had been for fundraising purposes. The apology satisfied some observers and enraged others. It was a reminder that even the most networked person in Silicon Valley couldn’t fully control the consequences of his own connections.

Chapter 10: The PayPal Mafia’s Unofficial Don (2002–2025)

If Peter Thiel was the PayPal Mafia’s intellectual godfather, Hoffman was its social infrastructure. He was the one who maintained relationships with everyone, who made introductions, who wrote reference checks, who showed up at dinners. When a PayPal alum started a new company, Hoffman was usually the first call and often the first check.

The numbers are staggering. PayPal alumni went on to create or lead companies worth over a trillion dollars in combined value. YouTube (sold to Google for $1.65 billion), Tesla and SpaceX (combined market cap in the hundreds of billions), Yelp, Palantir, Yammer, Slide — the list goes on. And Reid Hoffman had a hand in almost all of it, either as an investor, an advisor, or simply as the person who made the right introduction at the right time.

This wasn’t accident or luck. Hoffman had a theory about networks that he applied to his own life: the value of a network grows with the square of the number of connections, but only if those connections are activated. A dormant network is worthless. An active network is priceless. Hoffman kept his network perpetually active, and the compound returns were extraordinary.

Chapter 11: The Philosopher Returns — Writing and Thinking at Scale (2023–2025)

In his late fifties, Hoffman increasingly returned to his philosophical roots. He became one of the most thoughtful public voices on the implications of artificial intelligence, arguing that AI would be as transformative as electricity but that its benefits would only materialize if society invested in managing the transition. He worried about job displacement, not because he thought AI would eliminate work, but because the transition period would be brutal for people without the skills or resources to adapt.

He wrote extensively about “superagency” — his term for the amplified ability that AI gives individuals and organizations to accomplish things that were previously impossible. A single person with the right AI tools, he argued, could now accomplish what previously required a team of fifty. This was exciting and terrifying in equal measure.

Hoffman also grappled publicly with Silicon Valley’s political and cultural influence. He acknowledged that the tech industry had accumulated enormous power without the accountability structures that typically accompany power. Governments were too slow and too uninformed to regulate effectively. Companies were too conflicted to self-regulate honestly. The gap, Hoffman argued, needed to be filled by institutions that combined technical expertise with democratic legitimacy.

Chapter 12: Legacy — The Man Who Saw the Network

Reid Hoffman’s legacy is ultimately about one idea: networks matter more than nodes. The individual genius matters less than the connections between people. The single product matters less than the platform that enables millions of products. The lone founder matters less than the ecosystem that supports founders.

He built a $12 billion fortune by applying this principle consistently across every domain — founding LinkedIn, investing in network-effect businesses, maintaining the most valuable personal network in tech, and thinking about how networks scale. His mistakes — the Epstein connection, the Alabama disinformation episode, the tangled AI conflicts of interest — all stemmed from the same impulse: his network was so vast that he couldn’t fully control every node.

Hoffman bet his career on the idea that connecting people creates value. LinkedIn, which started with 350 email invitations, now has over a billion members in 200 countries. It has become the professional infrastructure of the global economy — the place where careers begin, jobs are filled, deals are made, and professional identities are maintained. Reid Hoffman didn’t just build a product. He built the connective tissue of the modern professional world. And in doing so, he proved his own thesis: the network is always more valuable than any individual within it.

💡 Key Insights

- ▸ Hoffman understood that in the network age, the most powerful position isn't being the biggest node — it's being the connector between nodes. LinkedIn's value wasn't any single user; it was the relationships between all of them.

- ▸ The PayPal Mafia's success wasn't luck — it was the deliberate cultivation of a network where former colleagues funded, advised, and championed each other's companies. Hoffman was the unofficial architect of that network.

- ▸ Hoffman's willingness to invest in ideas before they had traction — Facebook, Airbnb, Zynga — came from a philosophical conviction that networks create value in non-linear ways. Most investors model linear growth; Hoffman modeled network effects.