Carlos Slim: How a Lebanese Immigrant's Son Cornered Mexico's Phone Lines and Became the World's Richest Man

He bought Mexico's state telephone monopoly for pennies on the dollar during a privatization fire sale. Then he turned it into a fortune that briefly surpassed Bill Gates and Warren Buffett combined.

View all stories about this mogul

On March 10, 2010, Forbes magazine published its annual billionaires list. For the first time in the magazine’s history, the world’s richest person was not American. He wasn’t European. He wasn’t a tech founder, an oil baron, or a financial wizard from Wall Street. He was Carlos Slim Helú, a 70-year-old telecommunications magnate from Mexico City, with a net worth of $53.5 billion — surpassing Bill Gates by $6.5 billion. A man most Americans had never heard of was now, by the cold mathematics of net worth, the most financially successful human being on the planet.

The story of how he got there is a masterclass in a type of wealth-building that Silicon Valley doesn’t like to talk about: not innovation, not disruption, not “changing the world.” Just buying the right assets, at the right price, at the right moment — and holding them while everyone else panics.

🌱 Chapter 1: The Merchant’s Son

Carlos Slim Helú was born on January 28, 1940, in Mexico City. His parents were Maronite Christians who had emigrated from Lebanon. His father, Julián Slim Haddad, arrived in Mexico in 1902 at the age of 14, fleeing conscription in the Ottoman Empire. He opened a dry goods store called La Estrella de Oriente — The Star of the Orient — and through relentless work and shrewd real estate purchases during the Mexican Revolution, built a modest fortune.

Julián kept meticulous financial ledgers and taught his six children to do the same. By the time Carlos was 11 years old, he was maintaining a personal balance sheet, tracking his income (mostly allowance and small jobs) against his expenses. By 12, he had bought his first shares in a Mexican bank. By 15, he was analyzing stock fundamentals.

This wasn’t the childhood of a future tech visionary. This was the childhood of a future value investor — someone trained from the cradle to think in terms of assets, cash flows, and the gap between market price and intrinsic value.

Slim studied civil engineering at the National Autonomous University of Mexico (UNAM), graduating in 1961. He also taught algebra and linear programming at the university while simultaneously running his first investment operations. The engineering background gave him a structural mind: he thought about businesses the way an engineer thinks about load-bearing walls. What’s essential? What can be removed? What’s the failure point?

🏗️ Chapter 2: The Crisis Investor

Mexico’s economy in the 1970s and 1980s was a rollercoaster of oil-fueled booms and debt-driven busts. In 1982, the country defaulted on its international debt, triggering a crisis that wiped out billions in asset values. The peso collapsed. Capital fled. Real estate prices cratered. The stock market fell by over 70%.

Carlos Slim went shopping.

While most Mexican businessmen were liquidating their holdings and moving money to American banks, Slim was buying everything he could get his hands on. He acquired stakes in mining companies, retailers, tobacco firms, and construction companies — all at fire-sale prices. His logic was pure Graham-and-Dodd value investing: when everyone is selling in panic, the assets don’t disappear. The factories are still there. The customers are still there. The panic creates a gap between price and value, and that gap is where fortunes are made.

By 1985, Slim’s holding company, Grupo Carso (a portmanteau of Carlos and Soumaya, his wife’s name), controlled a diverse portfolio of Mexican industrial companies. He was already one of the richest men in Mexico. But he was about to become something much bigger.

📞 Chapter 3: The Deal of the Century

In 1990, Mexican President Carlos Salinas de Gortari announced the privatization of Telmex — Teléfonos de México, the state-owned telephone monopoly. The government was selling its controlling stake in the company that operated every landline in a country of 85 million people.

The privatization was structured as a public auction. Multiple bidders competed. Slim’s consortium — which included France Télécom and Southwestern Bell — won with a bid of approximately $1.76 billion for a 20.4% stake that came with operational control.

The price was a fraction of what Telmex was worth. The company had enormous embedded value: an installed base of millions of phone lines, a nationwide fiber-optic backbone, and — critically — the regulatory framework of a near-monopoly. Under the privatization terms, Telmex was granted a six-year period of exclusivity before competitors could enter the long-distance market. During that window, Slim had Mexico’s telecommunications infrastructure essentially to himself.

He moved fast. He invested heavily in modernizing the network — digitizing switching equipment, expanding coverage into rural areas, and dramatically reducing the time it took to install a new phone line (from months to days). Service improved. Revenue surged. And because Slim controlled the only game in town, profit margins were astronomical.

By 1994, Telmex was generating enough cash to fund Slim’s next move: the mobile revolution.

📱 Chapter 4: The Latin American Mobile Empire

In the mid-1990s, mobile phones were still a luxury product in most of Latin America. Slim saw what was coming. He founded América Móvil in 2000, spinning it off from Telmex as a dedicated wireless company. Then he began a continent-wide land grab.

Over the next decade, América Móvil acquired wireless operators in Brazil, Colombia, Ecuador, Argentina, Chile, Peru, Paraguay, Uruguay, Guatemala, El Salvador, Honduras, Nicaragua, and the Dominican Republic. The strategy was simple: buy the mobile license, build the network, sign up customers, and dominate before competitors could scale.

The prepaid model was key. In Latin America, where millions of people had no bank account or credit history, traditional postpaid phone contracts were impractical. Slim embraced prepaid — letting customers buy credit in small increments at corner stores. This made mobile phones accessible to hundreds of millions of people who had never been telecom customers before.

By 2010, América Móvil had over 230 million subscribers across the Americas. It was the largest telecommunications company in the Western Hemisphere outside the United States. In many countries, its market share exceeded 70%. Slim had done in wireless what he’d done in wireline: built a dominant position so large that competitors struggled to make a dent.

The financial results were extraordinary. América Móvil generated tens of billions in revenue annually. Slim’s net worth, driven overwhelmingly by his stakes in Telmex and América Móvil, soared past $50 billion. In 2010, he overtook Bill Gates to become the world’s richest person, a title he held for four consecutive years.

⚖️ Chapter 5: The Monopoly Problem

Slim’s dominance came with a political cost. By the 2010s, his telecommunications monopoly had become one of the most contentious political issues in Mexico.

Critics — including the OECD, which published a 2012 report estimating that Slim’s telecom monopoly cost the Mexican economy $129 billion over a decade through inflated prices — argued that Slim’s fortune was built not on entrepreneurial genius but on regulatory capture. He had bought a state monopoly, used exclusive licensing periods to entrench his position, and then leveraged his political relationships to delay meaningful competition for years.

In 2013, Mexican President Enrique Peña Nieto signed a sweeping telecommunications reform package designed to break Slim’s grip. The reforms created a new regulatory body with real enforcement power, established rules for network sharing, and classified Telmex and América Móvil as “dominant players” — a designation that subjected them to stricter regulation and forced them to offer wholesale access to competitors.

Slim’s response was characteristically pragmatic. He didn’t fight the reforms publicly. He complied with the new regulations, adjusted his pricing, and accepted the reduction in market share. His net worth dipped — from a peak of roughly $80 billion to about $50 billion — but he remained the richest man in Latin America by a wide margin.

The telecom reform debate exposed the fundamental tension at the heart of Slim’s empire: was he a visionary who modernized Mexico’s telecommunications infrastructure and connected hundreds of millions of Latin Americans to the mobile revolution? Or was he a monopolist who exploited a sweetheart privatization deal and overcharged consumers for two decades?

The honest answer is probably both.

📰 Chapter 6: The New York Times Lifeline

In January 2009, with the global financial crisis hammering newspaper advertising revenue, Carlos Slim lent The New York Times Company $250 million in exchange for 14% interest-rate notes and warrants that could be converted into a roughly 17% equity stake.

The Times was in genuine financial distress. Print advertising was collapsing. The company’s stock had fallen from $45 in 2004 to under $4. There were real questions about whether the paper of record would survive.

Slim’s loan was a lifeline. The terms were expensive — 14% interest was loan-shark territory — but Slim was one of the few people on Earth with both the cash and the willingness to bet on a distressed media asset. He later converted his warrants into stock and gradually increased his stake.

By 2015, Slim was the single largest shareholder of The New York Times Company, with a stake worth approximately $250 million. By 2026, following the Times’s remarkable digital transformation under CEO Meredith Kopit Levien — which pushed the company past 10 million digital subscribers — Slim’s investment was worth well over $1 billion.

It was vintage Slim: buy an iconic, high-quality asset when it’s on its knees, provide liquidity when everyone else is running for the exits, and wait. The same playbook he’d used in the 1982 Mexican debt crisis. The same playbook he’d used with Telmex. The same playbook, over and over, for five decades.

👨👩👦 Chapter 7: The Family Machine

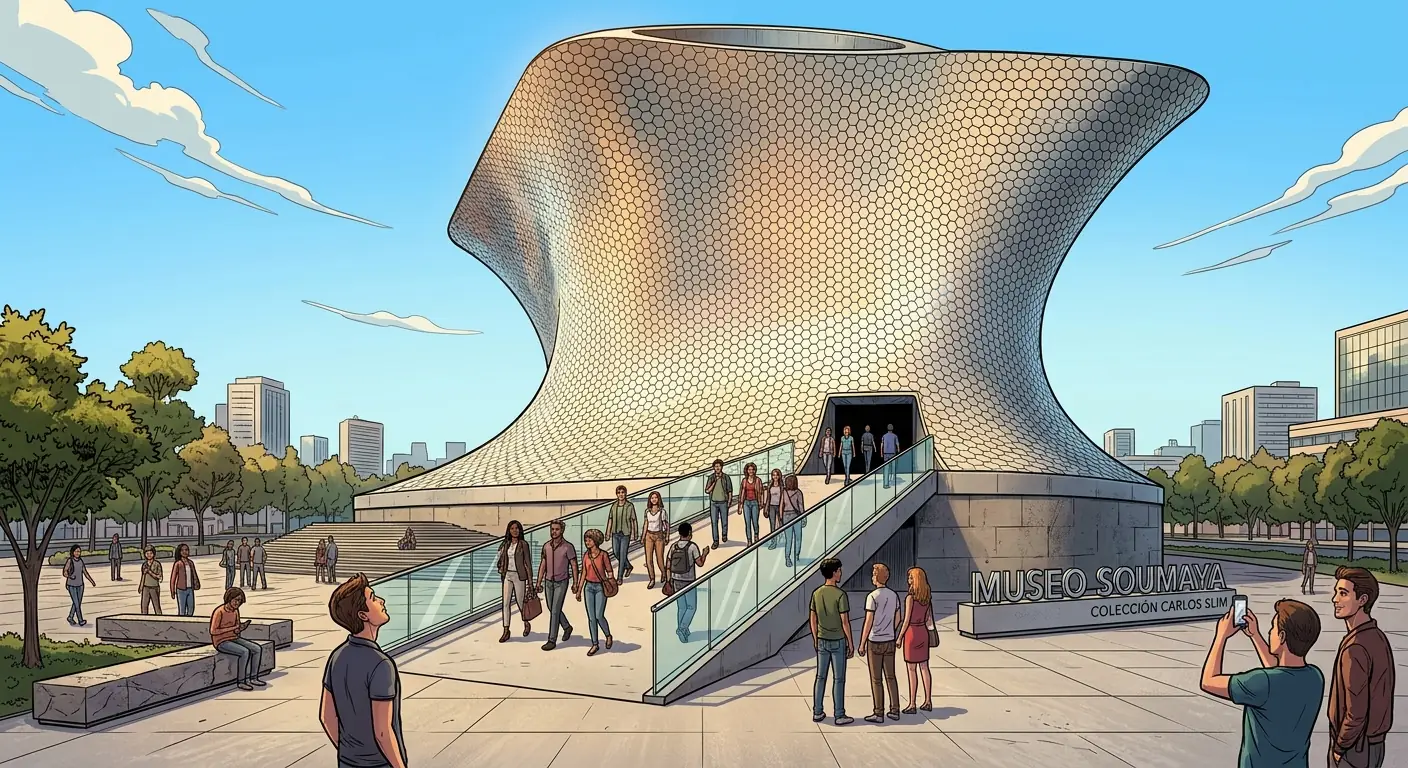

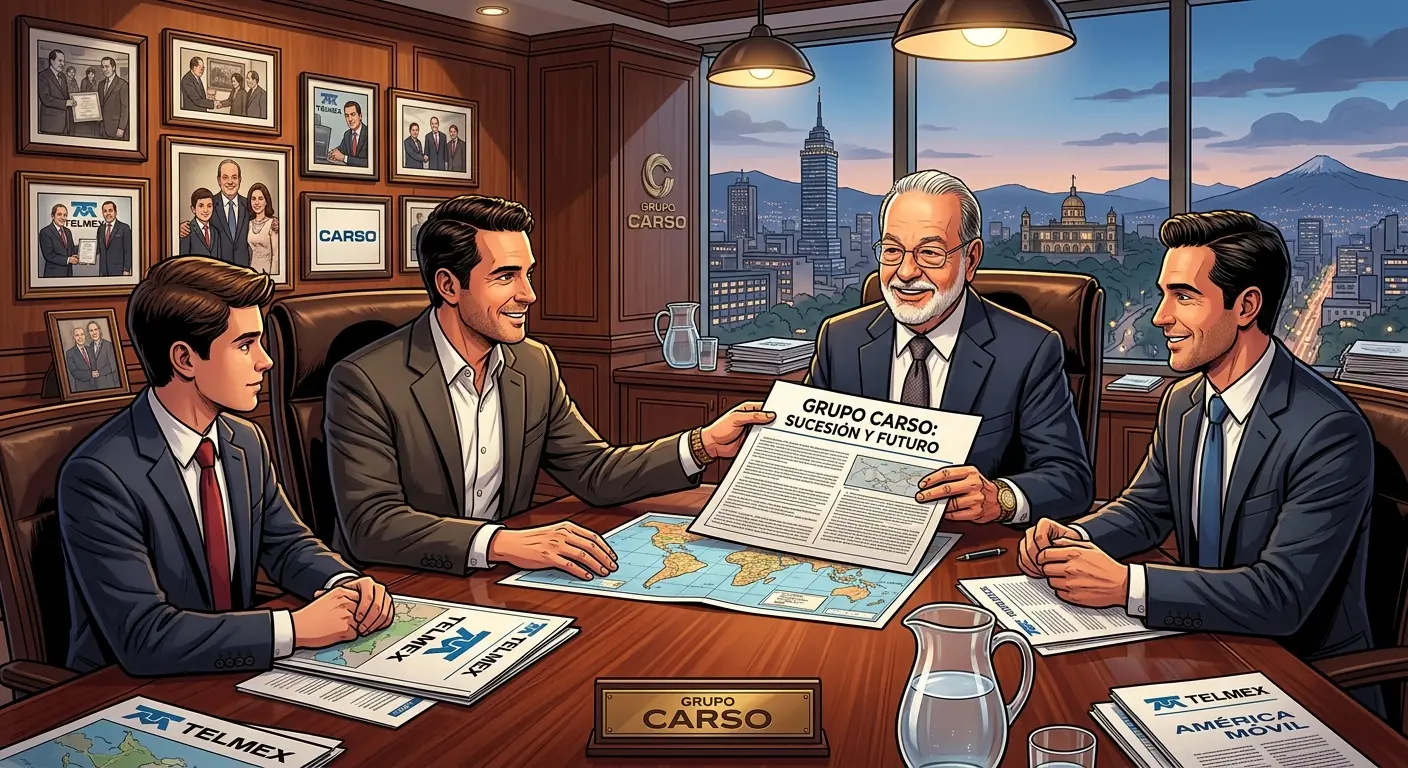

Unlike many billionaire dynasties that fracture across generations, the Slim family has operated with unusual cohesion. Carlos Slim has six children — three sons and three daughters — from his marriage to Soumaya Domit, who died of kidney disease in 1999. Her death devastated Slim, who named his flagship museum, the Museo Soumaya in Mexico City, in her honor. The museum, designed by architect Fernando Romero (who is married to Slim’s daughter Soumaya Jr.), houses over 66,000 works of art and is free to the public.

The three sons — Carlos Slim Domit, Marco Antonio Slim Domit, and Patrick Slim Domit — each run different segments of the family empire. Carlos Jr. chairs Telmex and América Móvil. Marco Antonio oversees Grupo Financiero Inbursa, the family’s banking and insurance arm. Patrick manages the family’s stakes in real estate and infrastructure.

The division is deliberate. By giving each son a distinct domain, Slim avoided the succession bloodbaths that have consumed other family empires. There is no single “heir” to compete for. Each brother runs his territory, and the family operates as a coordinated conglomerate rather than a zero-sum hierarchy.

Slim’s total family fortune, including assets held by his children, was estimated at approximately $100 billion in 2026. The Slims are, collectively, the wealthiest family in Latin America and one of the wealthiest in the world.

🏛️ Chapter 8: The Ledger

Carlos Slim’s personal net worth in early 2026 stands at approximately $82 billion, making him the 13th richest person in the world. He is 86 years old. He still goes to the office. He still reviews balance sheets. He still takes meetings.

His empire spans telecommunications, banking, insurance, construction, retail, mining, media, real estate, and energy. Grupo Carso’s companies account for roughly 40% of the listings on Mexico’s stock exchange. It is estimated that Slim’s businesses generate revenue equivalent to approximately 6% of Mexico’s GDP.

The debate over Slim’s legacy will never be settled cleanly. He modernized Mexico’s telecommunications infrastructure. He connected hundreds of millions of people across Latin America to mobile phones. He saved The New York Times. He built one of the world’s great museums and opened it to the public for free.

He also built his fortune on a privatization deal that many economists consider one of the most lopsided transactions in modern economic history. He charged some of the highest telecommunications rates in the OECD for years while operating in a country where tens of millions lived in poverty. His monopoly power was so extensive that the Mexican government had to pass sweeping reforms just to introduce basic competition.

Slim once said, in a rare interview: “When you live for others’ opinions, you are dead. I don’t want to live thinking about how I’ll be remembered.” It’s a convenient philosophy for a man whose legacy resists easy categorization.

What cannot be denied is the scale of what he built. A Lebanese immigrant arrived in Mexico in 1902 with nothing. His son, born 38 years later, became the richest person on the planet. In one generation, the Slim family went from a dry goods store in Mexico City to a fortune larger than the annual economic output of most nations.

That is an extraordinary story. Whether it’s an inspiring one depends entirely on what you think about the system that made it possible.

🧘 Chapter 9: The Man Behind the Money: Habits & Heart (1960s-Present)

So, we’ve talked about the deals, the acquisitions, the sheer, audacious scale of Carlos Slim’s empire. But who is the guy behind the spreadsheets and the unprecedented wealth? Is he a flashy billionaire with private jets and yachts the size of small countries? Nope. Not even close. If you’ve pictured a Mexican Gatsby, you’ve got it all wrong. Carlos Slim is, by all accounts, startlingly un-billionaire-like in his personal habits. This is a man who reportedly still lives in the same modest house he’s owned for decades, drives himself around Mexico City, and wears off-the-rack suits. His idea of a good time often involves a quiet dinner with family, a good cigar, and maybe a book. He’s reportedly never owned a computer, preferring to delegate digital tasks, and uses old-school notebooks for his meticulous planning. Talk about a man who marches to the beat of his own slightly analog drum.

The Frugal Mogul

His frugality isn’t just a quirky personal trait; it’s a core tenet of his business philosophy. It’s not about deprivation, but about efficiency and value. Why buy a new car when the old one still runs perfectly? Why waste money on lavish corporate headquarters when a functional office will do? This mindset permeated his companies. While other executives might have indulged in corporate perks, Slim insisted on lean operations, minimal debt, and a relentless focus on profitability. This was particularly crucial during Mexico’s economic downturns, allowing his companies to weather storms that sank more extravagant competitors. It’s the ultimate “waste not, want not” approach, scaled up to billions. He’s famously quoted as saying,

“I don’t believe in consumption. I believe in investment.” And he certainly put his money where his mouth is, or rather, kept it in his pocket (or invested it) instead of splurging. This isn’t just about saving a few pesos; it’s a deep-seated philosophical stance that helped build and protect his fortune.

A Love Story and a Legacy

Behind every great man, or so the saying goes, is a great woman. For Carlos Slim, that was Soumaya Domit Gemayel, his wife and the namesake of Grupo Carso. They married in 1966 and had six children together. Soumaya wasn’t just a spouse; she was a significant influence, particularly on his cultural and philanthropic endeavors. She was a passionate art collector and a driving force behind the creation of the Museo Soumaya, a stunning architectural marvel in Mexico City that houses Slim’s vast art collection, including works by Rodin and Da Vinci. Her battle with kidney disease, which she ultimately succumbed to in 1999 at the age of 50, was a profoundly impactful period for Slim. He established the Carlos Slim Health Institute, focusing on research, training, and health solutions, particularly for underserved populations. Her memory and her love for art and culture continue to shape a significant part of his public legacy, proving that even the most calculating of businessmen can be deeply moved by personal loss and love. It’s a reminder that even the world’s richest man is, at his core, a person with a personal history and motivations beyond just the bottom line.

🛒 Chapter 10: Beyond Telecom: The Retail & Infrastructure Juggernaut (1980s-Present)

While Telmex and America Movil are the colossal pillars of Carlos Slim’s empire, it would be a mistake to think he’s a one-trick pony. Far from it. His diversified portfolio, often acquired during economic downturns, includes some of Mexico’s most recognizable brands and essential infrastructure. We’re talking retail, construction, real estate, and even financial services. It’s like he looked at the entire Mexican economy and said, “Yeah, I’ll take a piece of that… and that… and especially that.” This strategy, born from his early days of crisis investing, created a sprawling conglomerate that touches nearly every aspect of Mexican life, often in ways consumers don’t even realize.

From Coffee Shops to Construction Sites

Take Sanborns, for instance. It’s not just a department store; it’s an institution in Mexico, famous for its blue-tiled “Casa de los Azulejos” restaurant in Mexico City. Slim acquired a majority stake in Sanborns in 1985, during one of Mexico’s economic crises, adding it to his Grupo Carso portfolio. He also scooped up Sears Roebuck de México in 1997, keeping the brand alive and thriving in Mexico long after its American parent company began its slow, painful decline. His approach wasn’t just to buy and hold; it was to revitalize. He streamlined operations, invested in modernizing stores, and applied the same disciplined financial management to these retail chains that he did to his telecom ventures. The result? These businesses, which many had written off, became consistent cash cows, providing a stable, diversified income stream that insulated his empire from the volatility of any single sector. It’s a classic move: buy undervalued assets, apply smart management, and watch them flourish.

Building Blocks of an Empire

But Slim’s reach extends far beyond retail therapy and coffee breaks. His construction and real estate holdings are massive. Grupo Carso Infraestructura y Construcción (CICSA) is one of Mexico’s largest construction firms, involved in everything from oil platforms to highways, tunnels, and water treatment plants. During the 1980s and 90s, when Mexico was undergoing significant infrastructure development, Slim was there, ready to build. This was a direct legacy of his civil engineering background. He understood the nuts and bolts of large-scale projects and saw the long-term value in essential infrastructure. This wasn’t just about making a quick buck; it was about laying the physical foundation for Mexico’s economic growth, and, conveniently, ensuring his companies were integral to that growth. He also holds significant real estate interests, owning vast tracts of land and commercial properties across Mexico. It’s a strategy that ensures his companies aren’t just selling services but are literally building the world around their customers, creating a symbiotic relationship where his businesses benefit from and contribute to the country’s development. It’s a masterclass in vertical and horizontal integration, making him not just a telecom titan but a true industrialist in the mold of the 20th century’s great tycoons.

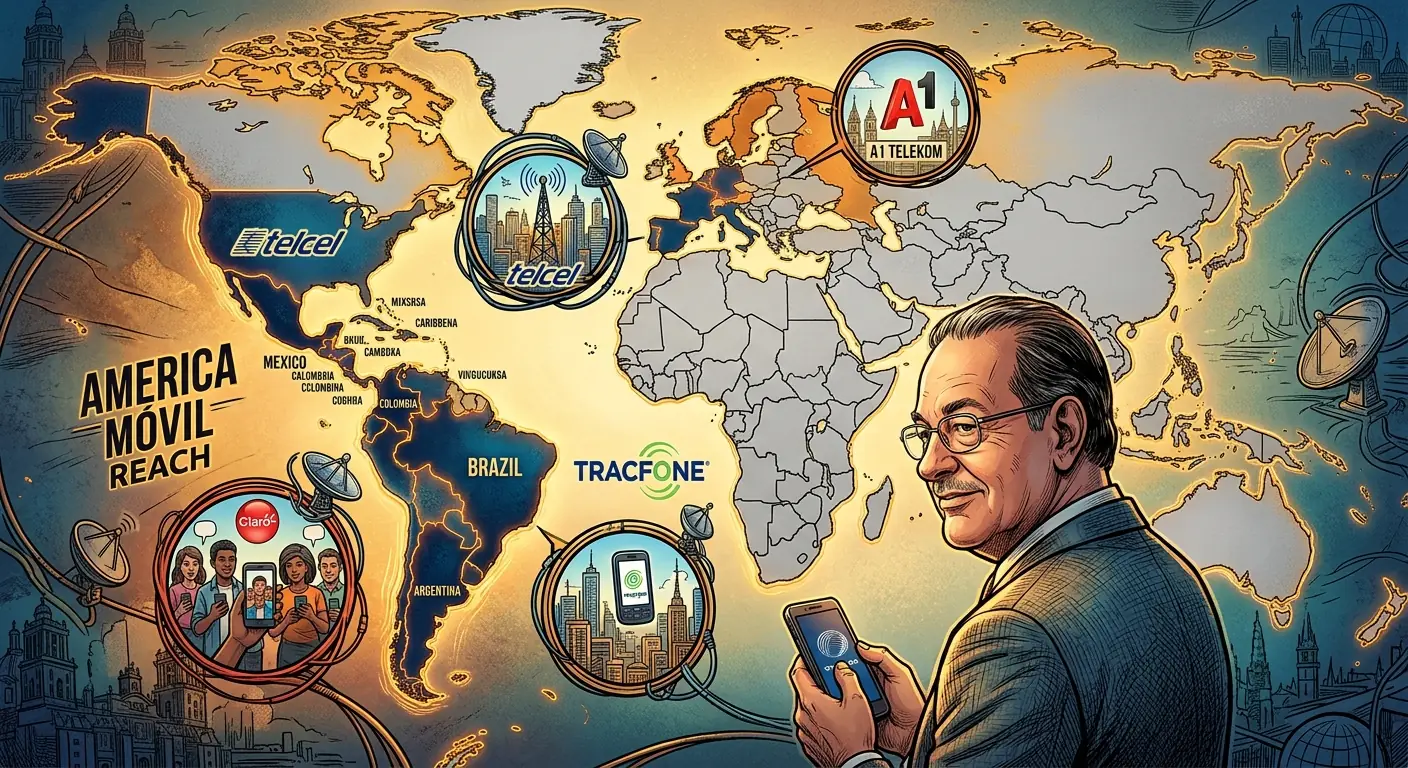

🌍 Chapter 11: The Global Telecom Wars and American Expansion (2000s-Present)

After conquering Mexico and much of Latin America with America Movil, Carlos Slim wasn’t content to rest on his laurels. His ambition, it turned out, was global. The early 2000s saw a mad dash by telecom giants to expand internationally, and Slim, ever the shrewd opportunist, was ready to play. While many saw borders, he saw untapped markets and potential synergies. This wasn’t just about adding more subscribers; it was about building a continental, then intercontinental, network that could compete with the world’s biggest players, bringing him into direct conflict with established giants like AT&T, Vodafone, and Telefonica. The game was on, and Slim was bringing his signature aggressive, value-focused play to the global stage.

Crossing Borders: TracFone and Europe

One of America Movil’s most significant international forays was into the United States with TracFone Wireless. Launched in 1996 (though significant growth came in the 2000s), TracFone targeted the prepaid mobile market, particularly among low-income customers and immigrants. It was a brilliant move, leveraging America Movil’s expertise in catering to a similar demographic in Latin America. By offering affordable, no-contract plans, TracFone grew to become the largest prepaid mobile provider in the US, a market segment largely overlooked by major carriers focusing on postpaid contracts. By 2014, TracFone had over 25 million subscribers in the US, making America Movil a silent but powerful player in the fiercely competitive American market. But Slim’s ambitions didn’t stop at the US border. He made significant moves into Europe, often through strategic investments rather than outright acquisitions. In 2012, America Movil became the largest shareholder in Dutch telecom company KPN, eventually owning around 21%. He also took a substantial stake in Austrian operator Telekom Austria. These moves were less about direct control and more about gaining influence, diversifying his portfolio, and potentially creating a larger, interconnected network. It was a sophisticated game of chess, positioning his empire in key global markets, even if he wasn’t always the sole monarch.

The Clash of Titans: Regulatory Headaches Abroad

Naturally, such aggressive global expansion didn’t go unnoticed, nor was it without its challenges. Slim’s reputation as a dominant force preceded him, and regulators in Europe and the US were often wary of his moves, fearing the kind of market concentration he’d achieved in Mexico. His bid to take full control of KPN, for example, faced significant political resistance in the Netherlands, ultimately forcing him to back down. This was a stark contrast to his relatively smoother sailing in less regulated Latin American markets. His global expansion also brought him into direct, often brutal, competition with the world’s established telecom heavyweights. Telefonica, Vodafone, and AT&T saw America Movil as a formidable, often relentless, rival. These weren’t just business battles; they were often regulatory skirmishes, lobbying wars, and pricing showdowns across multiple continents. Slim learned that while his proven strategy of low-cost operations and aggressive market capture worked, the political and regulatory landscapes varied wildly. It was a continuous dance between ambition and pragmatism, proving that even for the world’s richest man, global dominance is never a straightforward path.

🖼️ Chapter 12: Philanthropy and the Cultural Touch (2000s-Present)

For a man often criticized for his monopolistic tendencies and relentless pursuit of profit, Carlos Slim has also made an undeniable mark in the world of philanthropy and culture. It’s a fascinating duality: the shrewd capitalist who built an empire, and the benefactor who opened a world-class art museum and poured billions into health and education initiatives. Is it enlightened self-interest? A genuine desire to give back? Or perhaps a bit of both, with a generous dash of legacy-building thrown in? Whatever the motivation, the scale of his philanthropic endeavors is as impressive as his business acumen, often focusing on areas that reflect his personal interests and the needs of his home country.

The Soumaya Museum: A Gift to Mexico

Perhaps the most visible symbol of Slim’s cultural philanthropy is the Museo Soumaya in Mexico City. Named in honor of his late wife, Soumaya Domit Gemayel, the museum is an architectural marvel designed by his son-in-law, Fernando Romero. Opened in 2011, this shimmering, asymmetrical structure is home to Slim’s vast personal art collection, which reportedly numbers over 66,000 pieces. And here’s the kicker: admission is absolutely free. This isn’t just a vanity project; it’s a genuine gift to the people of Mexico, providing access to a collection that includes pre-Hispanic Mesoamerican pieces, 19th- and 20th-century Mexican art, and an astonishing array of European masters, notably the largest private collection of Auguste Rodin sculptures outside of France. He famously said,

“We want to promote art from Mexico and the world, for all publics.” The museum stands as a testament to his wife’s passion and his own belief in the power of art to enrich lives, making culture accessible to millions who might not otherwise experience it. It’s a grand gesture that profoundly impacts Mexico City’s cultural landscape.

Billions for Betterment: Health, Education, and Digital Inclusion

Beyond the art world, Carlos Slim’s philanthropic efforts are channeled primarily through the Carlos Slim Foundation. Established in 1986, though significantly expanded in the 2000s, the Foundation is one of the largest private philanthropic organizations in Latin America. Its focus areas are broad but strategic: health, education, employment, justice, culture, human development, and environmental protection. In 2010, he pledged $6.5 billion to various initiatives, a staggering sum that underscored his commitment. One key area is health, particularly in Latin America, focusing on preventable diseases, maternal health, and combating chronic illnesses. The Foundation has invested heavily in digital health solutions and training programs for health professionals. In education, it has launched initiatives like “Capacítate para el Empleo” (Train for Employment), an online platform offering free vocational training courses, aiming to bridge the skills gap and boost employment opportunities for millions. They’ve also been instrumental in promoting digital literacy and access to technology, recognizing that connectivity, an industry he dominates, is also a crucial tool for social progress. While critics might argue that his philanthropy is a way to soften his monopolistic image or secure tax benefits (and hey, who doesn’t like a good tax break?), the sheer scale and impact of the Carlos Slim Foundation’s work are undeniable, addressing critical social needs with significant, measurable results.

🕰️ Chapter 13: The Enduring Legacy and Future of an Empire (2020s-Present)

Carlos Slim Helú, now in his early 80s, remains a towering figure in global business. His net worth, while fluctuating with market conditions, consistently places him among the wealthiest people on Earth. But what does the future hold for the man who once topped the Forbes list, and more importantly, for the vast empire he meticulously built? The questions of legacy, succession, and the evolving challenges of a new economic landscape are now front and center. It’s a testament to his foresight that these transitions are already well underway, designed to ensure that Grupo Carso and America Movil continue to thrive long after their founder steps back completely.

The Succession Plan: A Family Affair

Unlike some tycoons who cling to power until their last breath, Slim has been orchestrating a gradual, deliberate succession for years. His three sons – Carlos Slim Domit, Marco Antonio Slim Domit, and Patrick Slim Domit – have been deeply involved in running the various arms of the empire for decades. Carlos Jr. is the chairman of the board of America Movil and Grupo Carso. Marco Antonio heads Grupo Financiero Inbursa, the family’s financial services arm. Patrick oversees the retail and industrial divisions. His sons-in-law also hold key positions. This isn’t a sudden handover; it’s a meticulously planned transition, mirroring the family-centric approach he learned from his own father. The control is distributed, but the strategic direction remains cohesive, guided by the principles Slim himself instilled: long-term vision, disciplined investment, and a keen eye for value. It’s less about a single successor and more about a collective leadership, ensuring continuity and shared responsibility. This approach minimizes the risk of a power vacuum or a chaotic breakup of the empire, a common pitfall for many family-run businesses of this scale.

Enduring Impact and Lingering Criticisms

Carlos Slim’s legacy is, without doubt, complex and multifaceted. He transformed Mexico’s telecommunications landscape, bringing phones and internet to millions, fostering economic growth, and building a global powerhouse. His business philosophy — buying low, holding long, and focusing on operational efficiency — is a case study in value investing. He’s proven that wealth can be built not just through innovation but through shrewd, almost brutally effective, capital allocation. Yet, criticisms persist. His monopolies have often been accused of stifling competition, leading to higher prices for consumers in Mexico, a charge he has consistently downplayed. Regulatory bodies have chipped away at his dominance, forcing America Movil to divest assets and open its networks. These battles continue to shape the industry in Mexico. However, his philanthropic efforts, especially the free Museo Soumaya and the wide-reaching Carlos Slim Foundation, offer a counter-narrative, painting him as a benefactor who genuinely cares about his country’s social and cultural development. His impact on Mexico is profound, extending from the phone in your pocket to the art on display and the infrastructure beneath your feet. He is a testament to the power of a single individual’s vision, tenacity, and, yes, colossal capital, to reshape an entire nation and leave an indelible mark on the global economic stage. The lessons from Carlos Slim’s journey are many, but perhaps the most enduring is that true wealth isn’t just amassed; it’s meticulously built, defended, and ultimately, whether through business or philanthropy, imprinted on the world.

💡 Key Insights

- ▸ Slim's fortune was built not on innovation but on timing and structure. He bought Telmex during Mexico's 1990 privatization wave for $1.76 billion — roughly 20 cents on the dollar of its true value — and was given regulatory terms that effectively guaranteed a monopoly for years. The lesson: the biggest fortunes are often made not by creating markets but by acquiring them at the moment of maximum dislocation.

- ▸ Slim modeled his investment philosophy on Warren Buffett's: buy quality assets when they're distressed, hold them forever, and let compounding do the work. But where Buffett operated in transparent U.S. markets with strong regulators, Slim operated in Latin America, where relationships with governments determined access to deals. Same philosophy, vastly different playing field.

- ▸ When Slim became the world's richest man in 2010, surpassing Bill Gates, it triggered a national debate in Mexico about inequality. A country where 40% of the population lived in poverty had produced the planet's wealthiest individual. Slim's response — investing in infrastructure and education — was generous but didn't address the structural critique: his fortune existed partly because of the regulatory moat that kept competitors out.

- ▸ Slim's $250 million investment in The New York Times in 2015 — made when the paper was struggling financially — demonstrated his understanding of undervalued assets. By 2026, that investment had returned over $1 billion. The pattern is always the same: find a premium asset in temporary distress, provide liquidity when no one else will, and wait.

- ▸ At 86, Slim's empire is managed by his three sons — Carlos Jr., Marco Antonio, and Patrick — who run different parts of the family's business conglomerate. Unlike many dynastic successions, the Slim family has maintained cohesion by giving each heir a distinct domain rather than forcing them to compete for a single throne.