Jeffrey Skilling: The McKinsey Golden Boy Who Turned Enron Into America's Most Spectacular Fraud

He was the smartest guy in every room. He turned a boring gas pipeline company into the 7th-largest corporation in America. Then he walked out the door six months before it collapsed, triggering the largest corporate bankruptcy in U.S. history — and the criminal case that would define a generation of white-collar enforcement.

View all stories about this mogul

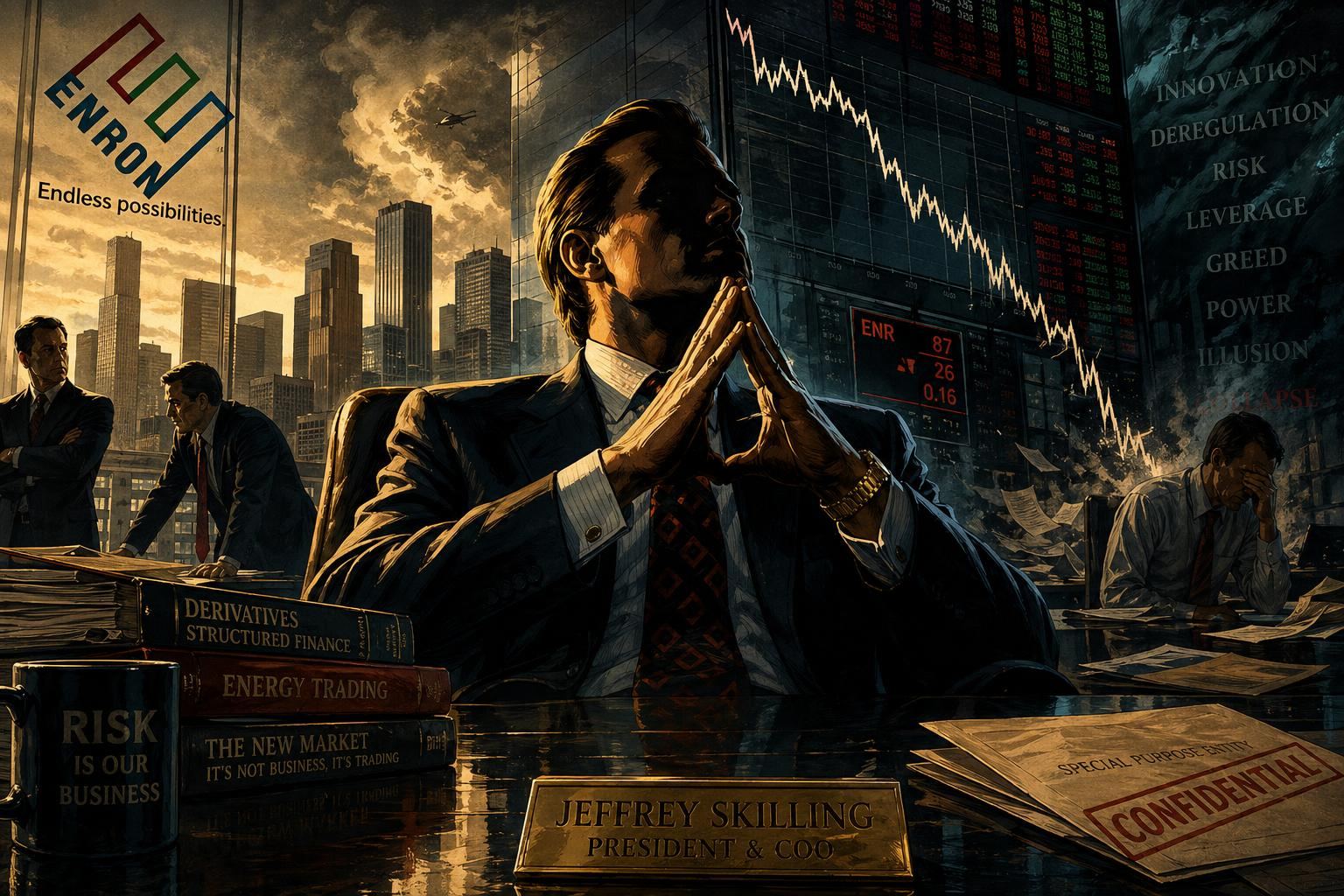

On August 14, 2001, Jeffrey Skilling walked into the offices of Enron chairman Kenneth Lay in Houston and told his boss that he was resigning as CEO. He had been in the job for less than seven months. Enron’s stock price was down roughly 50% from its peak. Internal financial pressures were mounting. Investors were asking uncomfortable questions. The press was circling.

Lay was stunned. He begged Skilling to reconsider. Skilling refused. He cited “personal reasons.” He said he was exhausted. He said he wanted to spend time with his family. Publicly, the resignation announcement would be framed as a voluntary departure by a successful executive seeking better work-life balance.

Privately, Skilling was running for the exit.

Within six weeks, Enron would begin to unravel publicly. Within three months, the company would file for bankruptcy — at the time, the largest corporate bankruptcy in American history. Within a year, Jeffrey Skilling would be under criminal investigation. Within four years, he would be convicted of federal fraud, conspiracy, and insider trading. Within five years, he would be sentenced to 24 years in prison — a sentence later reduced to 14 years on appeal.

The collapse of Enron would become the defining corporate scandal of the early 21st century. It would take down Arthur Andersen, one of the five largest accounting firms in the world. It would wipe out tens of thousands of jobs and billions of dollars in employee retirement savings. It would trigger the Sarbanes-Oxley Act, the most significant corporate governance reform in American history.

And at the center of it all stood Jeffrey Skilling — the McKinsey consultant turned energy trader turned CEO who had built, nurtured, and ultimately destroyed the company that was supposed to be his masterpiece.

📚 Chapter 1: The Boy Who Wanted to Be the Smartest

Jeffrey Keith Skilling was born on November 25, 1953, in Pittsburgh, Pennsylvania, the second of four children. His father was a sales engineer for a valve manufacturer; his mother was a homemaker. The family moved frequently during Jeff’s childhood, eventually settling in a suburb of Aurora, Illinois, outside Chicago.

From an early age, Skilling was obsessed with being the smartest person in the room. His teachers described him as intellectually formidable, endlessly curious, and occasionally arrogant. He was a top student in mathematics and science. He read voraciously. He also had an early entrepreneurial streak: as a teenager, he worked as a production director for a small TV station in Aurora, handling technical operations that most adults in the industry wouldn’t touch.

He enrolled at Southern Methodist University in Dallas, earning a bachelor’s degree in applied science in 1975. He then went to Harvard Business School, graduating in 1979 in the top 5% of his class. His performance at HBS was legendary among his classmates: professors reportedly considered him one of the most intellectually intimidating students they had ever encountered.

After Harvard, Skilling joined McKinsey & Company, the elite management consulting firm. He quickly became one of its rising stars in the energy practice. By the mid-1980s, he was advising the energy giant Enron on strategic issues. That consulting relationship would eventually become the springboard for the rest of his career.

🔥 Chapter 2: The Enron Offer

In 1990, Enron’s CEO Kenneth Lay — a Missouri-born economist who had built the company through a series of mergers into one of the largest natural gas pipeline operators in North America — hired Jeffrey Skilling away from McKinsey and brought him to Houston. Skilling’s task was to transform Enron from a boring utility into a high-growth financial trading company.

Skilling’s pitch to Lay had been audacious. He argued that natural gas, instead of being sold through traditional long-term contracts, should be traded like a commodity on open markets. Enron could create a “gas bank” where producers and buyers met to trade, and Enron would profit from the spread. It was a brilliant insight. Natural gas was, in fact, about to be deregulated, and Enron was perfectly positioned to become the Wall Street of energy.

Skilling built the gas trading business from the ground up. He hired former commodities traders. He built risk management systems. He created financial instruments that could hedge natural gas prices years into the future. By 1996, Enron Gas Services was generating more profit than Enron’s entire pipeline business. Skilling was rewarded with a promotion to president and chief operating officer of Enron Corporation.

The gas trading model worked so well that Skilling began looking for other markets to apply it to. Electricity. Weather derivatives. Bandwidth. Paper. Coal. Water. Any commodity, any market — Skilling believed it could be turned into a financial trading business using Enron’s models and Enron’s capital.

📈 Chapter 3: The Magic of Mark-to-Market

The single most important accounting innovation of Skilling’s career was persuading the Securities and Exchange Commission to let Enron use “mark-to-market” accounting for long-term energy contracts. In traditional accounting, a company recognized revenue as it was earned — over the life of a contract. In mark-to-market accounting, a company could project the total future value of a contract, apply a discount rate, and book the present value as current-year revenue.

For Enron, this was magical. When the company signed a twenty-year contract to sell natural gas, it could book almost all of the expected profits from that contract immediately, rather than over twenty years. Quarterly earnings looked enormous. Growth rates looked spectacular. Wall Street analysts, watching Enron’s reported numbers, assumed the company was executing one of the greatest transformations in corporate history.

The problem, of course, was that mark-to-market accounting only worked if the future assumptions turned out to be correct. If a contract underperformed, Enron would have to take massive write-downs years later. If market prices moved against Enron’s positions, the booked profits would evaporate.

Skilling’s answer was to keep signing new contracts, keep booking new projected profits, and keep the quarterly earnings growing. As long as Enron could keep generating new business, the old contracts wouldn’t matter. It was a treadmill, and the treadmill needed to keep speeding up to stay ahead of the problems it was creating.

💼 Chapter 4: The Culture of Fear

Under Skilling’s leadership, Enron developed a performance review system that became infamous throughout corporate America. It was called the Performance Review Committee — or, more commonly, “rank and yank.” Every six months, every Enron employee was ranked from 1 to 5 based on peer reviews and manager evaluations. Employees ranked 5 were automatically fired. Approximately 15% of the workforce was terminated each year, regardless of absolute performance.

The system was designed to create ruthless competition inside Enron. Skilling believed that elite companies needed to continuously cull their weakest performers in order to maintain a culture of excellence. But in practice, rank and yank created something closer to a culture of fear. Employees hid information from their peers. They sabotaged each other’s projects. They agreed with their managers whether the managers were right or wrong. They refused to raise concerns about questionable practices because anyone who challenged the prevailing narrative risked being ranked a 5 at the next review cycle.

The result was that Enron’s internal warning systems essentially stopped working. Deals that had obvious flaws were approved. Contracts that had unrealistic assumptions were celebrated. Employees who saw problems either stayed silent or quietly left the company. By 2000, Enron was an organization that had lost the ability to tell itself the truth.

This culture would prove fatal when the company needed to confront its own mistakes.

💰 Chapter 5: The Special Purpose Entities

To hide Enron’s growing debts and failing investments, the company’s CFO, Andrew Fastow, developed an elaborate system of “special purpose entities” — off-balance-sheet partnerships with names like LJM, Raptors, Chewco, and JEDI. These entities were legally separate from Enron but were controlled, directly or indirectly, by Enron itself. They allowed Enron to transfer money-losing assets off its balance sheet, book gains on phony transactions, and hide billions of dollars in debt from public investors.

Fastow designed and managed these structures. Skilling, as president and then CEO, approved them. Arthur Andersen, Enron’s auditor, signed off on them. The SEC allowed them. And for years, they worked. Enron’s reported financial performance looked strong even as the underlying business was becoming increasingly fragile.

At the same time, some of these partnerships generated enormous personal profits for Fastow himself — a direct conflict of interest that was disclosed in filings but buried in technical language most investors never read. Fastow would eventually be accused of skimming tens of millions of dollars for his own benefit through these structures.

The arrangements were so complex that even Enron’s own employees struggled to understand them. A 2001 Fortune article by journalist Bethany McLean, titled “Is Enron Overpriced?”, raised public questions about the company’s business model for the first time. It was the beginning of a short but devastating unraveling.

🏆 Chapter 6: America’s Most Innovative Company

At its peak in 2000 and early 2001, Enron was celebrated as one of the most successful and innovative companies in American history. Fortune magazine named Enron “America’s Most Innovative Company” for six consecutive years from 1996 through 2001. Enron’s executives were featured on the covers of business magazines. Its conferences attracted top CEOs, politicians, and academics.

Skilling’s personal compensation reflected the adulation. He earned tens of millions of dollars in annual salary, bonuses, and stock options. He became one of the highest-paid executives in the United States. He was celebrated as the intellectual force behind the company’s transformation, the man who had taught corporate America how to think like Wall Street.

Enron’s stock price reflected the narrative. It climbed from under $20 in 1998 to over $90 by August 2000 — a 4.5x gain in two years. The company’s market capitalization crossed $70 billion. It became the seventh-largest company in the United States by reported revenue.

Skilling was promoted to CEO in February 2001, replacing Kenneth Lay, who stayed on as chairman. It was supposed to be the crowning moment of Skilling’s career. Instead, it was the beginning of the end.

📉 Chapter 7: The Resignation

From the moment Skilling took over as CEO, Enron began to fall apart. The stock price declined from its peak. Several of the company’s non-trading businesses were performing badly. Questions about off-balance-sheet partnerships were beginning to surface. Short sellers were circling. Skilling, who had thrived in the company-building phase, was poorly suited to the crisis-management phase.

On August 14, 2001 — just six months after becoming CEO — Skilling resigned. The public statement emphasized personal reasons. Privately, multiple insiders later said that Skilling had become unable to sleep, unable to function, and desperate to escape before the company’s problems became publicly unmanageable.

Kenneth Lay returned as CEO and attempted to reassure investors that Enron was fundamentally healthy. The reassurances did not work. Over the following weeks, Enron’s auditors began questioning the special purpose entities. Executives began leaving. Whistleblowers, including the now-famous Sherron Watkins, warned Lay that the company’s accounting was unsustainable.

On October 16, 2001, Enron announced a $618 million quarterly loss and a $1.2 billion reduction in shareholder equity tied to its off-balance-sheet arrangements. The SEC launched a formal investigation. The credit rating agencies began downgrading Enron’s debt. Customers began refusing to enter into new contracts. The trading business — the heart of Enron’s revenue — seized up.

💀 Chapter 8: The Bankruptcy

On December 2, 2001, Enron filed for Chapter 11 bankruptcy protection. It was, at the time, the largest corporate bankruptcy in American history. The company’s stock — which had traded above $90 in August 2000 — was now trading for pennies. Twenty thousand Enron employees lost their jobs. Many of them also lost their retirement savings, which had been invested heavily in Enron stock as part of the company’s 401(k) plan.

Arthur Andersen, Enron’s auditor, was dragged down with the company. In June 2002, Andersen was convicted of obstruction of justice for shredding Enron-related documents. Although the Supreme Court later overturned the conviction, the damage was irreversible. Andersen — one of the “Big Five” accounting firms — ceased to exist. Tens of thousands of Andersen employees around the world lost their jobs as a result of Enron’s collapse.

The political and regulatory response was swift. Congress held hearings. Investors filed class-action lawsuits. In July 2002, President George W. Bush signed the Sarbanes-Oxley Act, which imposed strict new requirements on public company accounting, internal controls, and executive certification of financial statements. It was, at the time, the most significant corporate governance reform in American history.

⚖️ Chapter 9: The Trial

The federal government’s criminal investigation into Enron was massive. A dedicated Enron Task Force was established by the U.S. Department of Justice, drawing prosecutors from multiple U.S. Attorney’s offices. Over the next several years, dozens of Enron executives were indicted, and most agreed to cooperate with prosecutors in exchange for reduced sentences.

Andrew Fastow pleaded guilty in January 2004 and agreed to testify against his former bosses in exchange for a ten-year sentence. His testimony became the backbone of the case against Skilling and Lay. He described, in detail, how the special purpose entities had been used to hide Enron’s financial problems, and how Skilling had approved and directed the arrangements.

Jeffrey Skilling and Kenneth Lay were indicted in February 2004. Their trial began in January 2006 in Houston. It lasted four months. More than 50 witnesses testified. Prosecutors presented thousands of pages of documents. The defense argued that Skilling had been unaware of the fraudulent details and had relied in good faith on Enron’s accountants and lawyers.

The jury didn’t buy it. On May 25, 2006, Skilling was found guilty of 19 counts of fraud, conspiracy, insider trading, and making false statements. Lay was also found guilty — but he died of a heart attack in July 2006, before sentencing, and his convictions were later vacated on the legal principle that defendants cannot be convicted after death.

On October 23, 2006, Jeffrey Skilling was sentenced to 24 years and 4 months in federal prison, along with $45 million in restitution.

🔒 Chapter 10: Thirteen Years in Federal Prison

Skilling reported to a federal prison in Waseca, Minnesota, in December 2006. He was 53 years old. He would spend the next twelve years behind bars.

The sentence was later reduced on appeal. In 2013, after years of legal battles, Skilling reached an agreement with federal prosecutors that cut his sentence to 14 years in exchange for dropping his remaining appeals. The deal also required him to pay $42 million to the victims of the Enron fraud.

Prison life was, by all accounts, a shock to Skilling. He had gone from being one of the highest-paid and most celebrated executives in America to being inmate 29296-179, working menial jobs and eating cafeteria food. He taught GED classes to other inmates. He read widely. He kept in touch with his family. According to fellow inmates who later spoke to journalists, he was quiet, disciplined, and largely unrepentant about Enron’s collapse itself — though he acknowledged that individual accounting decisions had been flawed.

He was released from federal custody in February 2019, having served over twelve years in total.

💼 Chapter 11: The Attempted Comeback

Upon his release, Skilling surprised the business world by attempting to return to the energy industry. In 2020, he began exploring new ventures related to blockchain technology, energy trading, and data analytics. Reports surfaced that he was pitching potential partners on a new trading platform concept. The idea of Jeffrey Skilling — convicted felon, architect of the largest corporate collapse of his generation — returning to the energy industry provoked a mixture of outrage, disbelief, and morbid fascination.

His attempted comeback struggled. Most established financial institutions refused to work with him. Regulators watched his activities closely. Potential investors were understandably hesitant. Skilling had been one of the most publicly disgraced executives in American history, and his brand damage was extreme.

But Skilling, characteristically, did not give up. He continued to network, pitch, and rebuild. Whether he ultimately succeeds in a meaningful new business remains uncertain. What is remarkable is that he tried at all — that after twelve years in prison and the destruction of tens of thousands of people’s retirement savings, he still believed he had something to contribute.

🌅 Chapter 12: The Ledger

Enron’s collapse wiped out approximately $74 billion in shareholder value. It cost roughly 20,000 Enron employees their jobs and, in many cases, their life savings. It destroyed Arthur Andersen and ended the careers of tens of thousands of accountants, auditors, and consultants who had nothing to do with Enron’s fraud. It triggered the Sarbanes-Oxley Act, which reshaped corporate governance for every public company in the United States. It made “Enron” a verb — as in, “I was Enron’d by my employer’s retirement plan.”

Jeffrey Skilling, personally, lost essentially everything. He lost his fortune. He lost his public reputation. He lost his freedom for more than a decade. His wife Sue died of cancer in 2016 while he was still incarcerated. His son, John Taylor “J.T.” Skilling, died of an apparent drug overdose in 2011. His daughter, Kristin, wrote publicly about the years of grief and shame the family had endured as a result of her father’s prosecution.

Skilling himself is now in his early 70s. He has served his sentence. He has paid his restitution. He has, by the legal measure, fulfilled his punishment. He lives in Houston. He remains one of the most studied case subjects in business school curricula — a figure whose name is still invoked whenever a public company’s accounting practices look suspicious.

The lesson of Skilling’s career is not that he was uniquely evil or stupid. The lesson is that he was extraordinarily capable — intellectually brilliant, deeply ambitious, relentlessly confident — and that his capabilities were directed toward a system of accounting tricks and cultural brutality that eventually outran its own ability to hide from reality. He was not an idiot. He was a genius who convinced himself that the rules did not apply to him.

Every generation of business executives produces its own version of Jeffrey Skilling. Enron’s collapse is a reminder of what happens when that type of executive is given the keys to a multi-billion-dollar corporation and told that their performance will be judged quarterly. The numbers will always look good — until they don’t. And when they don’t, the damage will be measured in jobs lost, savings destroyed, and generations of trust in American capitalism eroded.

That is the ledger Jeffrey Skilling left behind. It is still being paid.

💡 Key Insights

- ▸ Skilling's greatest innovation — 'mark-to-market accounting' for long-term energy contracts — allowed Enron to book decades of projected future profits as current earnings. It was technically legal, wildly aggressive, and inevitably fatal. The lesson: creative accounting that depends on future assumptions being correct will eventually punish someone who can't wait for the future.

- ▸ Enron's stack-ranking system — in which 15% of employees were fired every year regardless of absolute performance — created a culture of ruthless internal competition that punished anyone who raised concerns. Cultures of fear cannot self-correct, even when the company is sailing toward a cliff.

- ▸ Skilling's abrupt resignation in August 2001, six months before Enron collapsed, was later cited by prosecutors as evidence he knew the company was doomed. The jury agreed. Founders and CEOs who leave suddenly during good times are almost always leaving for a reason.

- ▸ The 2002 Sarbanes-Oxley Act — passed in direct response to Enron and WorldCom — reshaped corporate governance in America for a generation. Skilling's fraud did not just destroy Enron; it permanently changed how every public company in the United States is audited and governed.

- ▸ Skilling served 12 years in federal prison and was released in 2019. His ongoing attempts to rebuild a business career in the energy sector — despite being one of the most publicly disgraced executives in American history — are a reminder that ambition is not easily extinguished, even by conviction and imprisonment.