Mark Zuckerberg: From Harvard Dropout to the Architect of the AI Age

He wired a billion humans together, survived a crisis that could have destroyed any CEO, then bet his entire empire on two futures at once — and one of them is actually working.

View all stories about this mogul

In January 2004, a nineteen-year-old sophomore at Harvard sat in his Kirkland House dorm room and wrote a few thousand lines of PHP code. Twenty-two years later, the thing he built connects 3.2 billion people daily, generates over $130 billion in annual revenue, and is now racing to define how humanity interacts with artificial intelligence. The sophomore is worth roughly $200 billion. He still wears the same gray t-shirt.

Mark Zuckerberg is the youngest self-made billionaire in history, the most sued man in Silicon Valley (and that’s saying something), the CEO who sat stone-faced through two congressional hearings while senators asked him how Facebook makes money, and — increasingly — the guy who might have just made the smartest strategic play in the entire AI race by giving his best technology away for free.

This is the story of how a socially awkward programmer from Westchester County built the most powerful communication network in human history, nearly lost it to a privacy scandal that made “delete Facebook” a global movement, bet $46 billion on virtual reality, and then pivoted into AI with a strategy so counterintuitive that his competitors are still trying to figure out whether it’s genius or insanity.

🏫 Chapter 1: The Wiring of Mark Zuckerberg (1984–2003)

Mark Elliot Zuckerberg was born on May 14, 1984, in White Plains, New York. His father, Edward, was a dentist. His mother, Karen, was a psychiatrist. Upper-middle-class, suburban, stable. No trauma narrative here. No rags-to-riches origin story. Just a kid with a dentist dad who happened to be freakishly good with computers.

How freakishly good? At age 12, he built a messaging program called “ZuckNet” that connected the computers in their home to the ones in his father’s dental office. His dad used it as an intercom system. Most twelve-year-olds in 1996 were playing Doom. Zuckerberg was building intranet communications software for a dental practice.

His parents hired a private tutor — David Newman, a software developer — who came to the house once a week. Newman would later tell reporters that the kid was a “prodigy” and that keeping ahead of him was a genuine challenge. Zuckerberg transferred to Phillips Exeter Academy, one of the most elite prep schools in the country, where he excelled in classics and computer science.

The Synapse Moment

Before Facebook, before Harvard, Zuckerberg built something that proved he understood human behavior at a software level. During his senior year at Exeter, he and a friend created Synapse — a music player that used machine learning (in 2002!) to learn your listening habits and build playlists automatically. Essentially, it was Spotify’s recommendation engine a decade before Spotify existed.

Both Microsoft and AOL reportedly tried to acquire Synapse and hire the teenager who built it. Zuckerberg turned them both down. He was going to Harvard.

Think about that for a second. An eighteen-year-old turns down job offers from two of the biggest tech companies on the planet. Not because he had a better offer. Because he wanted to go to college. This is not a kid who lacked confidence.

💻 Chapter 2: The Facebook — From Dorm Room to Domination (2004–2012)

The founding story has been told so many times — in books, in a $225 million Aaron Sorkin film, in a thousand magazine profiles — that mythology has almost replaced reality. So let’s stick to what actually happened.

In January 2004, Zuckerberg registered thefacebook.com. On February 4, he launched it from his dorm room. The site was restricted to Harvard students. Within 24 hours, between 1,200 and 1,500 students had signed up. Within a month, more than half the undergraduate population was on it.

The key insight — the one that separated thefacebook from Friendster, MySpace, and every other social network that existed — was real identity. You signed up with your real name. You connected with people you actually knew. You used your real Harvard email to verify. In a world of anonymous screen names and fake profiles, Zuckerberg bet on authenticity. It was a simple idea. It was also a billion-dollar idea.

Eduardo, Sean, and the Money

Zuckerberg’s co-founder and initial CFO was Eduardo Saverin, who put up $15,000 in seed money. Their partnership would disintegrate in one of Silicon Valley’s ugliest co-founder disputes, settled for an estimated $65 million and an undisclosed number of shares.

But the person who truly changed Facebook’s trajectory was Sean Parker — the Napster co-founder who convinced Zuckerberg to move to Palo Alto, drop the “the,” and think about the company in terms of billions, not millions.

“Drop the ‘the.’ Just Facebook. It’s cleaner.” — Sean Parker, as dramatized in The Social Network (but reportedly close to what actually happened)

Parker introduced Zuckerberg to Peter Thiel, who wrote the first outside check: $500,000 for a 10.2% stake in June 2004. That stake would eventually be worth billions. Not a bad return for a lunch meeting.

The Growth Machine

What happened between 2004 and 2012 was less a startup story and more a phenomenon. Facebook expanded from Harvard to the Ivy League, then to all colleges, then to high schools, then to everyone with an email address. The growth was not organic in the warm, fuzzy sense. It was engineered. Zuckerberg and his team were obsessively, almost pathologically focused on growth metrics.

The numbers tell the story:

- 1 million users by December 2004

- 5.5 million by December 2005

- 12 million by December 2006

- 100 million by August 2008

- 500 million by July 2010

- 1 billion monthly active users by October 2012

Each milestone was a moat. Every person who joined made the platform more valuable for everyone already on it — the classic network effect, executed at a speed and scale never seen before.

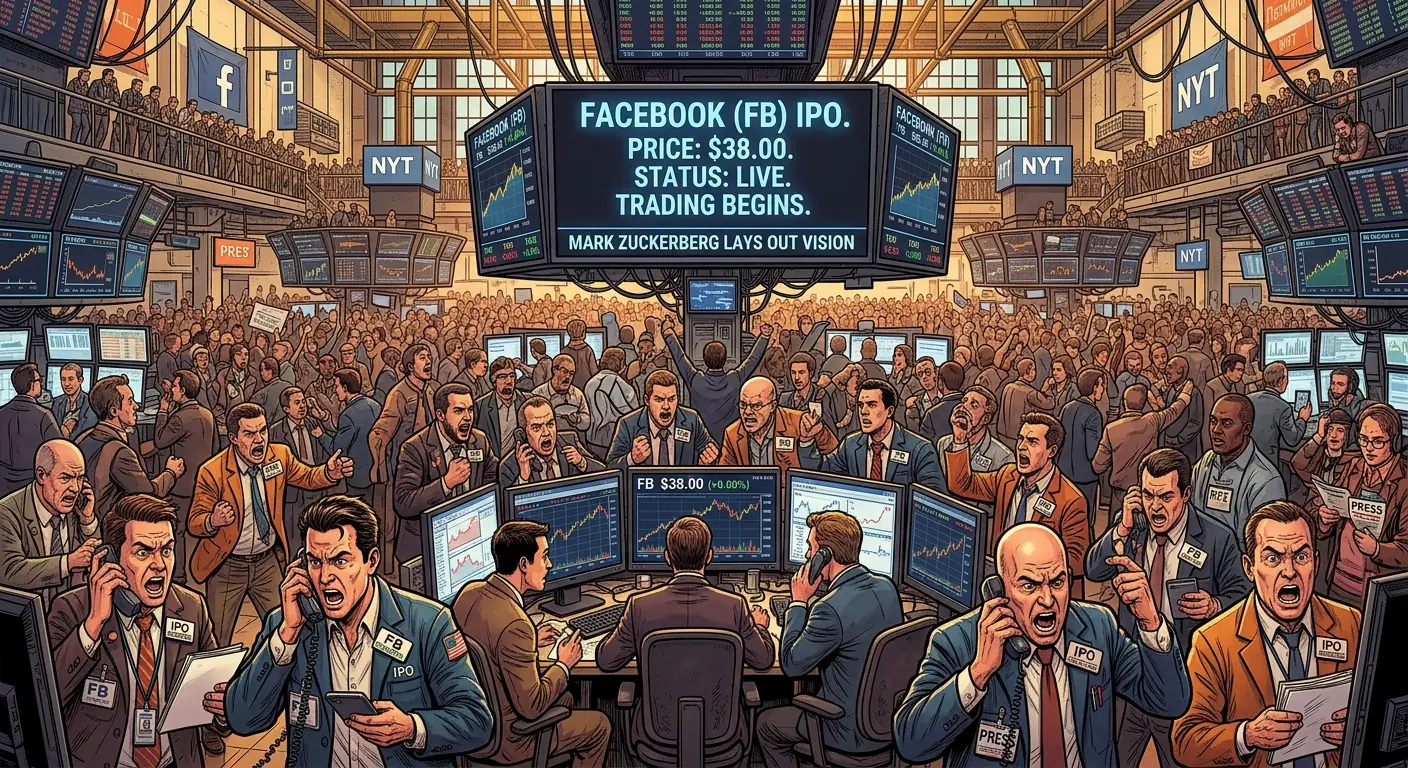

The IPO That Stumbled

On May 18, 2012, Facebook went public on the NASDAQ at $38 per share, valuing the company at approximately $104 billion — the largest technology IPO in history at the time. Zuckerberg rang the opening bell from Facebook’s Menlo Park headquarters wearing his signature hoodie, a detail that delighted the press and quietly horrified Wall Street traditionalists.

Then the stock cratered.

Within three months, Facebook shares had fallen to $17.55 — a 54% decline from the IPO price. Analysts hammered the company’s mobile strategy (or lack thereof). At the time, Facebook generated virtually zero revenue from mobile, even though the majority of its users were already accessing the platform on phones. The narrative flipped overnight: Zuckerberg went from boy genius to the guy who might have just presided over the most overhyped IPO in tech history.

“There’s no guarantee that Facebook is going to be able to make money on mobile.” — Analyst note, summer 2012

What happened next is, in retrospect, one of the most decisive pivots in corporate history.

📱 Chapter 3: The Mobile Pivot and the Acquisition Spree (2012–2017)

Zuckerberg did something that very few CEOs at the helm of a $100 billion company can bring themselves to do: he admitted he was wrong. Not in a vague, PR-managed way. He told his entire company that Facebook was a mobile-first company now — and if you were working on desktop features, you needed to stop and start thinking about phones.

He mandated that every employee use Facebook on their phone as their primary way of accessing the product. He personally reviewed mobile designs. He rejected features that didn’t work elegantly on a 4-inch screen. It was a top-down, CEO-driven transformation of a company with thousands of employees, and it happened in months, not years.

By 2013, mobile ad revenue had gone from essentially zero to 41% of total advertising revenue. By 2014, it was 69%. By 2016, it was over 84%. The stock, which had been left for dead at $17, climbed past the IPO price, then kept going. And going.

The Billion-Dollar Shopping Spree

Between 2012 and 2014, Zuckerberg made three acquisitions that reshaped the entire technology landscape:

Instagram — $1 billion (April 2012). At the time, Instagram had 30 million users, 13 employees, and zero revenue. The price tag was considered absurd. A billion dollars for a photo-sharing app? Bloomberg later estimated Instagram’s standalone value at over $100 billion by 2018. It was arguably the greatest acquisition in tech history.

WhatsApp — $19 billion (February 2014). The largest acquisition of a venture-backed company ever. WhatsApp had 450 million users and was growing at a million new users per day. Zuckerberg flew to the home of co-founder Jan Koum and pitched the deal personally. The strategic logic was simple: WhatsApp dominated messaging in markets where Facebook Messenger didn’t. Buying it meant owning global messaging. Period.

Oculus VR — $2 billion (March 2014). This one raised the most eyebrows. A virtual reality headset company? Most people thought it was an expensive toy. Zuckerberg saw it as the future of computing. He was early — arguably too early — but the purchase would eventually become the foundation of the entire Meta pivot.

“One day, we believe this kind of immersive, augmented reality will become a part of daily life for billions of people.” — Mark Zuckerberg, announcing the Oculus acquisition, March 2014

🔥 Chapter 4: The Reckoning — Cambridge Analytica and the Crisis Years (2016–2019)

If the first decade of Facebook’s story was a rocket ship, the second half of the 2010s was a controlled demolition of the company’s public image.

It started with the 2016 U.S. presidential election. Russian operatives used Facebook to run a disinformation campaign reaching an estimated 126 million Americans. Facebook was slow to acknowledge the problem and appeared more concerned about PR than impact on democratic institutions.

Then came Cambridge Analytica. In March 2018, The New York Times and The Guardian reported that Cambridge Analytica had harvested personal data from up to 87 million Facebook users without consent, using it to build psychographic profiles for political advertising through a personality quiz app that exploited Facebook’s own platform policies.

The fallout was immediate and severe. The hashtag #DeleteFacebook trended globally. Facebook’s stock dropped $119 billion in a single day on July 26, 2018 — the largest single-day loss in stock market history at that time. Zuckerberg was called to testify before both the Senate Judiciary Committee and the Senate Commerce Committee on April 10, 2018, and the House Energy and Commerce Committee the following day.

The hearings became iconic television. Zuckerberg wore a suit instead of his gray t-shirt and answered questions from senators who clearly did not understand how the internet worked.

“Senator, we run ads.” — Mark Zuckerberg, responding to Senator Orrin Hatch’s question about how Facebook makes money while remaining free to users, April 10, 2018

He survived. The stock recovered. But something had fundamentally changed. The era of Silicon Valley being treated as the good guys was over, and Facebook was the primary reason.

The FTC hit Facebook with a $5 billion fine in July 2019 — the largest penalty ever imposed on a company for violating consumers’ privacy. Five billion dollars. And Zuckerberg shrugged it off. Facebook’s annual revenue that year was $70.7 billion. The fine was less than a month’s earnings. The market literally cheered the settlement — the stock went up on the news because investors had feared something worse.

This crystallized what makes Zuckerberg different: he doesn’t crumble under public pressure, doesn’t resign, doesn’t even particularly seem to care about being liked. He just keeps building.

🌐 Chapter 5: The Meta Gamble (2021–2023)

On October 28, 2021, Mark Zuckerberg did something no one expected: he renamed his company. Facebook, Inc. became Meta Platforms, Inc. The ticker symbol changed from FB to META. The stated reason? The company’s future was the “metaverse” — a persistent, shared virtual world where people would work, socialize, and live through VR and AR headsets.

The rebrand was audacious, divisive, and partly motivated by the fact that the name “Facebook” had become toxic. Whistleblower Frances Haugen had leaked thousands of internal documents to The Wall Street Journal, revealing that Facebook knew Instagram was harmful to teenagers’ mental health and chose profits over safety. Changing the name didn’t make the problems go away — but it signaled that Zuckerberg was betting his legacy on something entirely new.

The Cost of Vision

The metaverse bet was not cheap. Meta’s Reality Labs division — responsible for VR headsets, AR glasses, and metaverse development — reported staggering losses:

- 2020: $6.6 billion loss

- 2021: $10.2 billion loss

- 2022: $13.7 billion loss

- 2023: $16.1 billion loss

That’s over $46 billion burned on a bet that, by 2023, had produced a VR platform called Horizon Worlds that was widely mocked for looking worse than a 2006 Wii game.

Wall Street revolted. Meta’s stock crashed from a peak of $384 in September 2021 to a low of $88 in November 2022 — a 77% decline that wiped more than $700 billion in market capitalization. Zuckerberg’s personal net worth dropped by over $100 billion. He went from the third-richest person on Earth to barely cracking the top twenty.

Activist investors called for his head. Analysts demanded he cut costs and abandon the metaverse. The media declared him finished.

“Mark is in the penalty box.” — Brad Gerstner, Altimeter Capital, in his open letter to Meta’s board, October 2022

But here’s the thing about Mark Zuckerberg that people keep forgetting: he owns roughly 13% of Meta’s total shares, but controls approximately 61% of the voting power through a dual-class share structure. Class B shares carry 10 votes per share. The board can advise him. Analysts can yell at him. Investors can sell their stock. Nobody can fire him.

He’s not a hired CEO. He’s a founder-king with a constitutional monarchy. And in 2023, the king decided to listen — but on his own terms.

✂️ Chapter 6: The Year of Efficiency (2023)

On March 14, 2023, Zuckerberg published a letter to employees titled “Update on Meta’s Year of Efficiency.” The language was unusually blunt for a CEO known for corporate-speak:

“I think we should prepare ourselves for the possibility that this new economic reality will continue for many years. Higher interest rates lead to the economy running leaner… I think we should operate leaner and more efficiently.” — Mark Zuckerberg, March 2023

The numbers were brutal. Meta cut approximately 21,000 jobs across two rounds of layoffs — about 25% of the workforce. Entire projects were shut down. Middle management layers were eliminated. Zuckerberg explicitly said he wanted to flatten the organization and reduce “managers managing managers.”

The results were extraordinary, at least by Wall Street’s metrics:

- Revenue (2023): $134.9 billion (up 16% year-over-year)

- Net income (2023): $39.1 billion (up 69% year-over-year)

- Operating margin: improved from 20% in 2022 to 29% in 2023

The stock responded accordingly. From its November 2022 low of $88, Meta shares climbed to over $390 by the end of 2023 — a roughly 340% gain in thirteen months. It was one of the most dramatic turnarounds in public market history.

But the Year of Efficiency wasn’t just about cost cuts. Something else was happening inside Meta. Something that would define the next chapter of Zuckerberg’s story.

🤖 Chapter 7: The AI Pivot — Llama and the Open Source Gambit (2023–Present)

While the world was focused on Meta’s layoffs and metaverse losses, Zuckerberg was quietly assembling one of the largest AI research operations on the planet. Meta’s FAIR (Fundamental AI Research) lab, founded in 2013 under the leadership of Yann LeCun, had been publishing groundbreaking papers for years. But in 2023, Zuckerberg shifted the entire company’s center of gravity toward AI — and did it with a strategy that nobody in the industry expected.

He gave it away.

The Llama Strategy

In February 2023, Meta released LLaMA (Large Language Model Meta AI) — a family of large language models ranging from 7 billion to 65 billion parameters. The initial release was restricted to researchers, but within a week, the model weights leaked online and became freely available.

Rather than fighting the leak, Zuckerberg leaned into it. In July 2023, Meta released Llama 2 as fully open-source, available for commercial use. In April 2024, Llama 3 followed with models up to 70 billion parameters. By early 2025, Llama 4 arrived with benchmarks competitive against the best closed-source models from OpenAI, Google, and Anthropic.

This was not generosity. It was a strategic masterstroke.

“I think that open source AI is going to be the best path for us and for the developer community. When you have an open ecosystem, it tends to develop and improve faster.” — Mark Zuckerberg, interview with The Verge, July 2023

Here’s the logic, stripped down: OpenAI charges for GPT access. Google charges for Gemini. Anthropic charges for Claude. They all need those revenues to fund their massive compute costs. Meta doesn’t need to charge for its AI models because Meta doesn’t make money from AI models. Meta makes money from advertising. It makes $130+ billion a year from ads.

By open-sourcing Llama, Zuckerberg accomplished several things simultaneously:

- Commoditized the competition’s core product. If a powerful AI model is free, it’s harder for OpenAI and Google to charge premium prices.

- Built an ecosystem. Thousands of developers building on Llama means thousands of developers invested in Meta’s AI stack.

- Attracted talent. AI researchers want to publish papers and share their work. Meta’s open approach is a powerful recruiting tool in a market where top AI researchers can name their price.

- Improved the product for free. Open-source communities find bugs, optimize performance, and build applications that Meta can learn from.

The Infrastructure Bet

Zuckerberg didn’t just release models. He committed to building the compute infrastructure to train them. In January 2024, he announced that Meta would build a massive AI infrastructure, targeting 350,000 NVIDIA H100 GPUs by end of year — an investment worth tens of billions of dollars.

In 2024, Meta’s capital expenditure guidance was $35–40 billion, primarily for AI infrastructure. For 2025, Zuckerberg signaled capex of $60–65 billion — numbers that dwarfed every competitor except Google and Microsoft.

This is the Zuckerberg pattern in its purest form: identify the next platform shift, commit resources at a scale that borders on reckless, endure the criticism, and bet that being early and aggressive will matter more than being cautious and right.

AI Across Meta’s Products

The AI pivot wasn’t just about Llama. Zuckerberg integrated AI across every Meta product:

- Meta AI — a chatbot assistant rolled out across WhatsApp, Instagram, Messenger, and Facebook, reaching hundreds of millions of users by mid-2024.

- AI-powered advertising — Meta’s Advantage+ ad system uses AI to automate campaign creation, targeting, and optimization. Advertisers reported significant improvements in return on ad spend.

- AI-generated content tools — image generation, text generation, and creative tools built directly into Instagram and Facebook.

- AI for recommendation algorithms — the core feed algorithms across all Meta platforms were rebuilt using advanced AI models, increasing engagement and time spent.

By late 2024, Zuckerberg was claiming that Meta AI was “on track to be the most-used AI assistant in the world” — a claim that, given Meta’s 3.2+ billion daily active users across its family of apps, was not implausible.

🧬 Chapter 8: The Man Behind the Machine (What Most People Get Wrong)

The public perception of Mark Zuckerberg is, to put it mildly, unflattering. The Jesse Eisenberg portrayal in The Social Network cemented an image of a cold, socially inept backstabber. The congressional hearings reinforced the robotic-CEO narrative. The memes are relentless.

But here’s what the caricature misses: Zuckerberg is one of the most adaptive business strategists alive. Consider the pivots:

- 2012: Pivoted from desktop to mobile. Facebook was left for dead. Stock recovered and soared.

- 2014: Acquired Instagram and WhatsApp when both seemed overpriced. Both became pillars of a trillion-dollar empire.

- 2021: Pivoted to the metaverse. Stock cratered. Still ongoing, but Ray-Ban Meta smart glasses have shown genuine consumer traction.

- 2023: Pivoted to AI while simultaneously executing a brutal cost restructuring. Stock tripled.

That’s four major strategic shifts in twelve years, any one of which could have destroyed the company if executed poorly. He executed all four. The only comparable track record is Satya Nadella’s transformation of Microsoft — but Nadella inherited a company in decline. Zuckerberg built his from a dorm room.

By the Numbers (as of early 2026)

- Meta market cap: ~$1.8 trillion

- Daily active users (family of apps): 3.3+ billion

- Annual revenue (2025): ~$165 billion

- Employees: ~67,000

- Zuckerberg’s net worth: ~$200 billion

- Age: 41

By any financial measure, he is one of the most successful entrepreneurs in human history. Whether his iron-grip control has always been exercised wisely is a separate — and much more contested — question.

🔑 Key Insights

1. Ruthless prioritization beats everything. Zuckerberg has killed his own strategies repeatedly — desktop for mobile, mobile-first for metaverse, then a hard correction back to efficiency and AI. Most CEOs can’t even make one painful pivot. He makes them serially, and he doesn’t flinch.

2. Open source can be a weapon, not just a gift. The Llama strategy is a case study in using openness as competitive strategy. By making the AI model layer free, Meta commoditizes its competitors’ revenue streams while protecting its own advertising moat. It’s the most sophisticated competitive move in the current AI race.

3. Scale is its own kind of armor. Facebook survived Cambridge Analytica, congressional hearings, a $5 billion FTC fine, and the #DeleteFacebook movement. The product barely lost users. When your platform has 2+ billion daily users, you are infrastructure. You can survive reputational damage that would kill any smaller company.

4. Founder control is a double-edged sword — but it enables long-term bets. The dual-class share structure that lets Zuckerberg control Meta’s direction despite owning only ~13% of shares is either brilliant governance or a structural flaw. It let him survive the metaverse losses that would have gotten any hired CEO fired. Whether that patience pays off depends on the next five years.

5. The best time to restructure is when your back is against the wall. The Year of Efficiency wasn’t planned during good times. It was forced by a stock collapse, investor revolt, and competitive pressure. But Zuckerberg executed it with a discipline that surprised everyone — and it unlocked the most profitable era in Meta’s history.

Mark Zuckerberg is 41 years old. He has been CEO of the same company for 22 years. He has survived lawsuits, congressional investigations, a privacy crisis that sparked a global backlash, a $700 billion stock crash, and an endless stream of memes questioning whether he’s actually human. Through all of it, he has never lost control of the company he built in a dorm room.

The question is whether his current bet on AI — backed by tens of billions in infrastructure and an open-source strategy that breaks every rule in Silicon Valley — will cement Meta’s dominance for the next decade, or whether he’s the last founder standing in a game about to be won by someone else entirely.

Either way, nobody’s counting him out. They tried that in 2012, 2018, and 2022. It didn’t work any of those times.

💸 Chapter 9: The IPO and the Billionaire Backlash (2012–2014)

So, Facebook had crushed the mobile pivot, bought Instagram for a cool $1 billion (a figure that now seems like petty cash), and was growing like kudzu across the globe. What’s next for a company that seems to have conquered the internet? You go public, obviously. And when Facebook went public on May 18, 2012, it wasn’t just an IPO; it was the IPO. The largest technology IPO in history at the time, valuing the company at a mind-boggling $104 billion. Zuckerberg, still only 28 years old, rang the Nasdaq bell from Menlo Park, surrounded by his team, looking about as comfortable as a penguin in a tuxedo (which is to say, not very).

The hype was galactic. Everyone wanted a piece of the Facebook pie. Brokerages struggled to handle the sheer volume of orders, and the stock opened at $42.05 per share, up from its initial offering price of $38. But then… well, then the party abruptly ended. The stock price immediately started to slide, closing barely above its IPO price on day one, and then tanking in the subsequent days and weeks. By September 2012, it had plummeted to around $17.55 per share, wiping out billions in shareholder value. Ouch. The press, which had been fawning just weeks earlier, turned into a pack of wolves, questioning everything from Facebook’s mobile advertising strategy (or perceived lack thereof) to the entire valuation. It was a brutal initiation into the public markets.

The Post-IPO Hangover

The immediate aftermath of the IPO was a chaotic scramble. Analysts, investors, and the media all pointed fingers. Was the valuation too high? Were the underwriters too greedy? Was Facebook’s mobile advertising strategy truly as weak as it seemed? Zuckerberg and his team were suddenly under a microscope, not just from users, but from Wall Street, which demands predictable growth and, you know, profits. This was a stark contrast to the “move fast and break things” ethos of a private startup. Now, every broken thing had a dollar sign attached to it.

Zuckerberg, ever the pragmatist, doubled down. He famously shifted the company’s focus to “mobile first, then everything else.” Internal teams were restructured, and engineering resources poured into optimizing the mobile experience and, crucially, mobile advertising. This period, though financially painful, forged a new discipline within the company. It forced them to confront their weaknesses head-on and laid the groundwork for the incredible mobile advertising machine Facebook would become. It taught them a hard lesson: even if you’re the king of social media, the market doesn’t care about your past triumphs; it cares about your future earnings.

The Billionaire Next Door (and his critics)

With the IPO, Zuckerberg officially became one of the wealthiest people on the planet. His net worth, which fluctuated wildly with the stock, was estimated at over $19 billion at the time of the IPO. Suddenly, the guy in the gray t-shirt was a symbol of immense, almost incomprehensible, wealth. This, naturally, attracted a new level of public scrutiny. No longer just a nerdy Harvard dropout, he was now the face of a corporate behemoth that touched billions of lives.

His notoriously private personal life became fair game, albeit one he fought hard to protect. Critics highlighted the perceived disconnect between his casual demeanor and the immense power he wield wielded. The media loved to juxtapose his modest hoodies with his billions, often with a hint of suspicion. Was he just a kid who got lucky, or a calculating genius? The answer, as always, was probably a bit of both. This era marked the beginning of public fascination and often, exasperation, with the man behind the world’s largest social network. It was the moment Zuckerberg transitioned from a tech innovator to a global figure whose every move, and every dollar, was dissected.

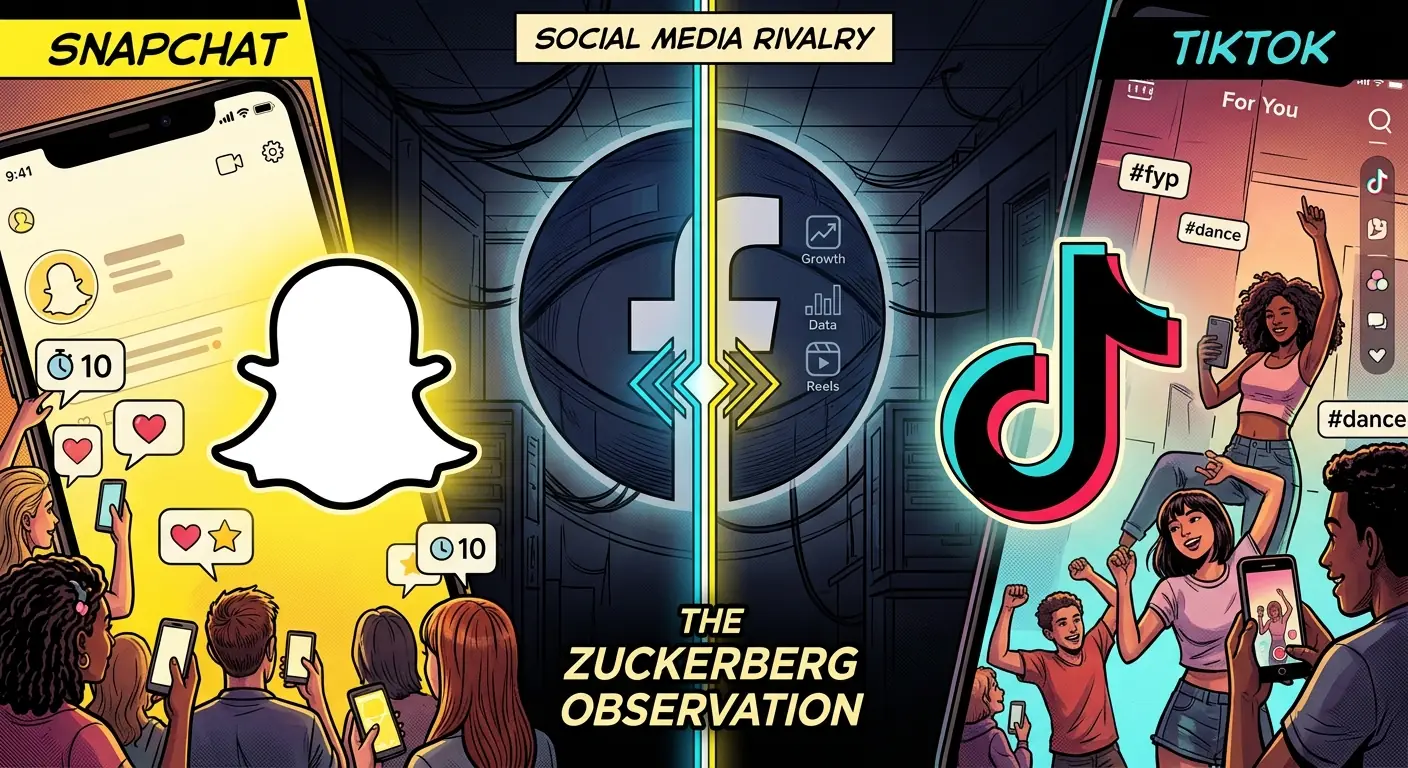

👻 Chapter 10: The Social Wars — Snapchat, TikTok, and the Copycat Kingdom (2013–2020)

Remember the good old days when Facebook was just competing with MySpace for who had the most sparkly profile backgrounds? Ah, simpler times. By the mid-2010s, Facebook wasn’t just the dominant social network; it was a digital empire. But empires always face challengers, especially from plucky upstarts with new ideas and younger demographics. Two of the biggest threats weren’t trying to be Facebook; they were trying to be different from Facebook: Snapchat and, later, TikTok. And Zuckerberg, ever the strategist, had a simple, effective, and often ruthless playbook for dealing with them: acquire, or if that fails, replicate.

The Ghost in the Machine

Enter Snapchat in 2011, with its disappearing messages and ephemeral “Stories.” It was everything Facebook wasn’t: spontaneous, raw, and seemingly free from the permanence that made Facebook feel, well, a bit like your digital yearbook. Young people loved it. Zuckerberg, recognizing a potent threat (and perhaps a brilliant idea), tried to buy Snapchat not once, but twice. First in 2013 for $3 billion, and again in 2016 for a reported $30 billion. Both times, Snapchat CEO Evan Spiegel famously said “no thanks.”

Zuckerberg’s response? “Fine, we’ll just build it ourselves.” In August 2016, Instagram, which Facebook owned, launched “Instagram Stories.” It was an almost carbon copy of Snapchat Stories, right down to the filters and swipe-up gestures. The tech world gasped. Spiegel himself commented, rather pointedly:

“At the end of the day, just because someone else has adopted a format, it doesn’t mean that we’re going to stop innovating.”

But innovate as Snapchat might, Instagram Stories quickly eclipsed it in user numbers. By June 2018, Instagram Stories had 400 million daily active users, dwarfing Snapchat’s 191 million. It was a masterclass in competitive cloning, a move that cemented Facebook’s reputation as a company that would not hesitate to absorb or imitate any perceived threat.

The Rise of Short-Form

Just as the dust settled on the Snapchat wars, a new challenger emerged from the East: TikTok. Launched internationally in 2017, this short-form video app, owned by Chinese company ByteDance, rapidly captured the attention of Gen Z with its addictive algorithmic feed and easy-to-use video creation tools. It was fun, creative, and dangerously engaging. Facebook, of course, took notice.

Initially, Facebook’s response was Lasso, a standalone TikTok clone launched in 2018. It flopped. Hard. Clearly, a different approach was needed. So, in August 2020, Facebook launched “Reels” directly within Instagram, once again leveraging its massive user base to integrate a competitor’s core feature. Reels was Facebook’s full-throated answer to TikTok, complete with an algorithmic feed and a push for creators. The strategy was clear: if they can’t acquire you, and a standalone clone fails, integrate your features into their existing, dominant platforms. It’s a strategy that has kept Facebook (now Meta) at the top, but also continually raises questions about anti-competitive practices and innovation.

The Acquisition That Got Away (or didn’t)

This era truly defined Facebook’s approach to competition: a willingness to spend astronomical sums for promising startups (Instagram, WhatsApp) or, failing that, to ruthlessly replicate their most successful features. This “copycat kingdom” strategy, while incredibly effective for Facebook’s bottom line, ignited fierce debates about antitrust and fair competition. Critics argued that Facebook stifled innovation by either buying out potential rivals or simply crushing them with its scale. Regulators started to pay closer attention, questioning whether a single company should have so much power to dictate the terms of the social media landscape. For Zuckerberg, it was about survival and dominance; for many others, it was about maintaining a healthy, competitive market.

🛑 Chapter 11: The Empire’s Ethical Quandaries (2017–2022)

If the Cambridge Analytica scandal (covered in Chapter 4) was a Category 5 hurricane for Facebook, then the years that followed were an endless, torrential downpour of ethical quandaries. It wasn’t just about data privacy anymore; it was about content moderation, misinformation, foreign interference, mental health, and the very fabric of democracy. Facebook, by virtue of its sheer scale, became a reluctant (or perhaps, a willfully blind) battleground for the world’s nastiest problems, and Mark Zuckerberg found himself constantly in the crosshairs.

The Content Conundrum

Post-2016, the world woke up to the dark underbelly of viral content. Facebook was implicated in everything from enabling the spread of misinformation during the 2016 and 2020 US elections to facilitating hate speech that fueled genocide in Myanmar. In 2018, a UN report concluded that Facebook played a “determining role” in inciting violence against the Rohingya Muslim minority in Myanmar. The company’s content moderation efforts, often outsourced to low-paid workers in developing countries, were deemed woefully inadequate, slow, and culturally insensitive.

The problem was immense: how do you moderate billions of posts in hundreds of languages, distinguishing between satire, legitimate news, and dangerous propaganda, all in real-time? Facebook poured billions into AI and human moderators, but the scale of the challenge often seemed insurmountable. Zuckerberg, in congressional hearings, often reiterated the company’s commitment to safety, but the public perception was that Facebook was always a step behind, reacting to crises rather than preventing them. It was a whack-a-mole game where the moles were constantly evolving and multiplying.

The Echo Chamber Effect

Beyond outright hate speech, critics increasingly pointed to Facebook’s core algorithmic design as a culprit for societal polarization and mental health issues. The algorithms, optimized for engagement, often prioritized sensational, emotionally charged content, inadvertently creating “echo chambers” where users were primarily exposed to views reinforcing their existing beliefs. This, some argued, contributed to political extremism and a decline in civil discourse.

Then came the bombshell internal documents. In 2021, former Facebook product manager Frances Haugen blew the whistle, leaking thousands of internal company documents to the Wall Street Journal and various regulatory bodies. These “Facebook Files” revealed that the company was well aware of the negative impacts of its platforms. Perhaps most damning were the findings that Instagram was detrimental to the mental health of teenage girls, with internal researchers noting:

“We make body image issues worse for one in three teen girls.”

The company’s own research showed that despite these findings, they often failed to act decisively to mitigate the harm, prioritizing growth and engagement. This revelation ignited a fresh wave of public outrage and calls for stricter regulation, painting a picture of a company that put profits before people.

The Whistleblower’s Cry

Frances Haugen’s testimony before Congress was a pivotal moment. She directly accused Facebook of prioritizing “astronomical profits over people.” Her revelations fueled bipartisan calls for greater transparency and accountability from tech giants. Zuckerberg, in response, dismissed many of the claims as a “false narrative” and defended the company’s investments in safety. He argued that the complex issues of social media couldn’t be solved by simply blaming one company.

However, the damage was done. The era between 2017 and 2022 saw Facebook’s reputation plummet, becoming a symbol for many of the ills of modern technology. From privacy breaches to political manipulation and mental health crises, the company became a lightning rod for criticism. It forced Zuckerberg to confront not just business challenges, but profound ethical and societal responsibilities, fundamentally changing the public’s perception of him and the empire he built. The “move fast and break things” mantra had finally collided with the harsh reality that some things, once broken, are incredibly difficult to fix.

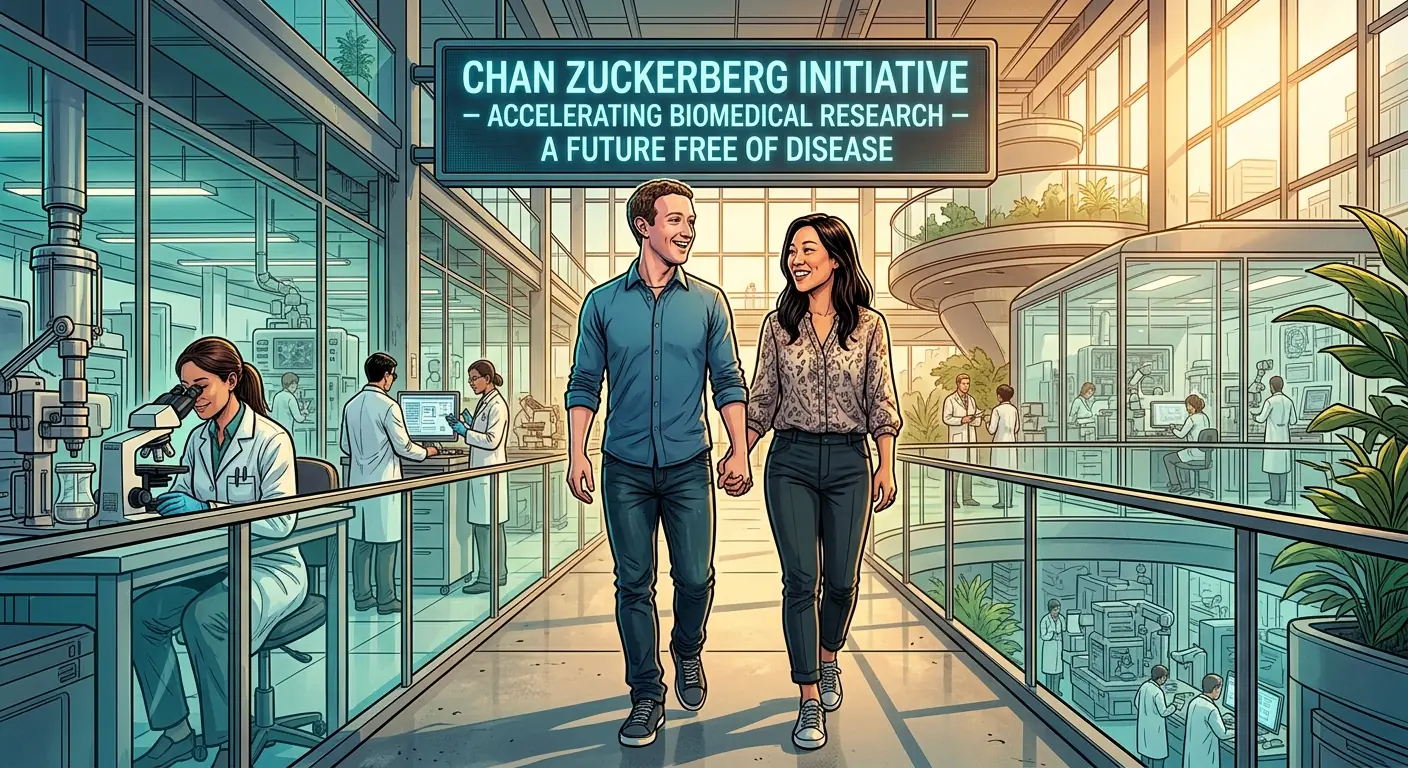

💖 Chapter 12: A Philanthropic Vision and the Long Game (2015–Present)

While the public was busy dissecting Facebook’s ethical dilemmas and Mark Zuckerberg’s stoic demeanor, another, perhaps less-understood, aspect of his life was quietly taking shape: his philanthropic endeavors and the blossoming of his personal life. Far from the image of the detached tech CEO, Zuckerberg, alongside his wife, Priscilla Chan, began to articulate a long-term vision for societal impact that went far beyond likes and shares.

The Pledge and the Purpose

In December 2015, shortly after the birth of their first daughter, Maxima, Mark and Priscilla announced the formation of the Chan Zuckerberg Initiative (CZI). But this wasn’t just another charitable foundation. In an open letter to their daughter, they pledged to give away 99% of their Facebook shares (then valued at about $45 billion) to advance human potential and promote equality. This wasn’t a one-time donation; it was a commitment to transfer the vast majority of their wealth over their lifetimes.

CZI was structured as a Limited Liability Company (LLC) rather than a traditional non-profit, a controversial but strategic choice that allowed it to invest in for-profit companies, participate in political lobbying, and generally operate with more agility than a traditional foundation. Their focus areas were ambitious: advancing science, curing disease, improving education, and promoting justice and opportunity. They weren’t just writing checks; they were building teams of scientists, engineers, and educators, aiming to tackle some of the world’s toughest problems with the same long-term, iterative approach Facebook used for its products. Think less “band-aid solutions” and more “rewriting the human genome.” For example, CZI’s Biohub aims to cure, prevent, or manage all diseases by the end of the century. That’s a pretty big swing.

Family Life and Public Scrutiny

Amidst the relentless public scrutiny of his company, Zuckerberg’s personal life evolved significantly. He married Priscilla Chan in May 2012 (the day after Facebook’s IPO, no less — talk about a whirlwind weekend!). They went on to have three daughters: Maxima (“Max”) in 2015, August in 2017, and Aurelia in 2023. These milestones often offered rare glimpses into a more human side of Zuckerberg, shared via (where else?) Facebook and Instagram posts, often accompanied by heartfelt reflections from Priscilla.

These personal moments, however, were still processed through the lens of public expectation and criticism. While many praised their philanthropic commitment, others questioned the CZI’s LLC structure, or debated whether Zuckerberg’s immense wealth and influence, even when directed towards good, concentrated too much power in too few hands. Balancing the demands of running a multi-billion-dollar corporation with the responsibilities of fatherhood and large-scale philanthropy is a unique tightrope walk, and Zuckerberg has largely chosen to keep his private life fiercely guarded, offering only curated glimpses.

The Future Beyond the Feed

What does CZI reveal about Zuckerberg’s long game? It suggests a belief that technology, data, and scientific rigor can be applied to solve humanity’s grand challenges, not just connect people. It’s a testament to his characteristic optimism about progress, even when his company faces existential threats. While Meta (Facebook’s parent company) is chasing the metaverse and AI, CZI is investing in brain imaging, single-cell biology, and personalized learning.

This duality—the pragmatic, hard-nosed CEO of Meta and the ambitious, scientific philanthropist—is key to understanding the full scope of Mark Zuckerberg. He’s not just building platforms; he’s investing in the fundamental tools and knowledge that he believes will shape the future of human existence. Whether it’s through a VR headset or a breakthrough in gene therapy, Zuckerberg seems committed to leaving an indelible mark on the world, for better or worse. It’s a vision that extends far beyond the daily scroll, touching upon the very essence of what it means to be human in the 21st century.

💡 Key Insights

- ▸ Zuckerberg's greatest skill isn't coding — it's ruthless prioritization. He killed Facebook's desktop-first strategy to go mobile, killed mobile-first to chase the metaverse, then pivoted again to AI. Most CEOs can't even make one painful pivot. He's made three.

- ▸ The open-source Llama strategy isn't charity — it's a calculated move to commoditize the AI layer that competitors charge for, while Meta monetizes AI through its unmatched advertising data. Giving away the model makes the ecosystem dependent on Meta's infrastructure.

- ▸ Zuckerberg survived the Cambridge Analytica crisis not by being likable, but by being irreplaceable. Facebook had 2.2 billion users. Senators could grill him on live TV, but they couldn't uninstall the app from a billion phones. Scale is its own kind of armor.

- ▸ The metaverse bet cost Meta over $46 billion in Reality Labs losses from 2020–2024. Most boards would have fired the CEO. Zuckerberg's dual-class share structure meant he couldn't be fired. Founder control is either visionary governance or a governance failure — depending entirely on whether the founder is right.

- ▸ Meta's 'Year of Efficiency' in 2023 — cutting 21,000 jobs and slashing costs — proved that Zuckerberg could operate as a disciplined capital allocator, not just a growth-obsessed founder. The stock tripled. Wall Street doesn't reward vision. It rewards margins.

Sources

- David Kirkpatrick — The Facebook Effect: The Inside Story of the Company That Is Connecting the World ↗

- Steven Levy — Facebook: The Inside Story (2020) ↗

- Meta Platforms Investor Relations — SEC Filings & Earnings Reports ↗

- U.S. Senate Committee on the Judiciary — Zuckerberg Testimony, April 10, 2018 ↗

- Meta AI Blog — Llama Model Releases ↗

- SEC Filing — Meta Platforms 2023 10-K Annual Report ↗

- Bloomberg — Meta's Market Cap and Financial Coverage ↗