From MIT to Inmate: How Sam Bankman-Fried Built a $32 Billion Empire on Stolen Money

He was crypto's golden boy — a messy-haired MIT grad who convinced the world he'd fix finance. Then $8 billion in customer funds vanished, and the empire collapsed in six days.

View all stories about this mogul

He shuffled into billion-dollar meetings wearing cargo shorts and a wrinkled T-shirt. He slept on a beanbag in the office. He played League of Legends during investor calls. He told Congress he wanted more regulation. He pledged to give away virtually every dollar he ever made. And behind that carefully crafted image of the nerdy altruist who just happened to be worth $26 billion, prosecutors would later allege, he was running one of the largest financial frauds in American history — siphoning at least $8 billion in customer deposits to prop up a failing trading firm, buy luxury real estate in the Bahamas, and make political donations that would make a lobbying firm blush. On March 28, 2024, a federal judge sentenced Samuel Bankman-Fried to 25 years in prison. He was 32 years old.

This is the story of how a math prodigy from Stanford academics built an empire on the premise that he was smarter than everyone else, and what happened when the world found out he wasn’t.

🎓 Chapter 1: The Prodigy — MIT, Utilitarianism, and the Birth of a True Believer (1992–2017)

Samuel Bankman-Fried was born on March 6, 1992, in Stanford, California — and if you wanted to design a human being in a lab to become a Silicon Valley poster child, you’d basically get his upbringing. Both parents were professors at Stanford Law School. His mother, Barbara Fried, was a prominent legal scholar who co-founded a political fundraising organization called Mind the Gap. His father, Joseph Bankman, specialized in tax law. Dinner table conversations were not about sports.

The Utilitarian Awakening

SBF — as the world would come to know him — attended MIT, where he studied physics and mathematics. He was sharp, restless, and socially awkward in the way that brilliant quantitative thinkers often are. But it wasn’t a physics lecture that changed his life. It was a conversation with Will MacAskill, a young Oxford philosopher and one of the founders of the effective altruism movement.

The pitch was elegant and intoxicating: if you really want to do the most good in the world, don’t go work at a nonprofit making $40,000 a year. Go make as much money as humanly possible, then give it all away. They called it “earning to give.” For a kid who was already good at math and itching to get rich, it was moral permission to pursue wealth with the intensity of a Wall Street shark while maintaining the self-image of a saint.

MacAskill would later tell interviewers that he saw extraordinary potential in the young SBF. Bankman-Fried himself would tell journalist Michael Lewis, as recounted in Going Infinite, that the encounter fundamentally reoriented his life. He wasn’t going to just make money. He was going to make all the money. For the greater good, of course.

Jane Street: Learning to Print Money

After graduating from MIT in 2014, SBF took a job at Jane Street Capital, one of the most elite quantitative trading firms on the planet. Jane Street is not the kind of place that hires people who are merely smart. It hires people who can look at a screen full of numbers and see patterns that the rest of humanity’s brains literally cannot process. And SBF belonged.

He traded international ETFs — exchange-traded funds — and by all accounts, he was very good at it. He learned how markets really worked: not through the tidy models from textbooks, but through the messy, fast, exploitable reality of global capital flows. He learned about arbitrage — buying something cheap in one market and selling it expensive in another, pocketing the difference. He learned about market microstructure, about liquidity, about the spaces between prices where real money lives.

He was reportedly earning well into the six figures. Most 23-year-olds would have been thrilled. SBF was bored. He didn’t want to be one more smart guy at a smart firm. He wanted to run the table.

And he’d spotted something that the buttoned-up world of traditional finance was still mostly ignoring: cryptocurrency markets were a mess. The same Bitcoin was trading at wildly different prices on different exchanges around the world. The arbitrage opportunities were enormous, and almost nobody sophisticated was exploiting them.

In 2017, Sam Bankman-Fried quit Jane Street. He was 25 years old, and he was about to build a machine that would make him one of the richest people on Earth — and then destroy him.

📈 Chapter 2: Alameda Research — The Money Machine (2017–2019)

In November 2017, SBF founded Alameda Research, a quantitative cryptocurrency trading firm. The name was deliberately boring — a misdirection. This wasn’t some basement crypto bro operation. This was a Jane Street–trained quant applying institutional-grade trading strategies to markets that were, at the time, dominated by amateurs.

The Kimchi Premium

The first big play was the “kimchi premium.” In late 2017 and early 2018, Bitcoin was trading at a significant premium on South Korean exchanges — sometimes 30% to 50% higher than on American exchanges. The reason was simple: massive retail demand in South Korea combined with capital controls that made it difficult for arbitrageurs to move money in and out of the country.

SBF figured out how to do it anyway. According to reporting by the Wall Street Journal and details in Michael Lewis’s Going Infinite, Alameda was reportedly moving tens of millions of dollars through a complex web of intermediaries to buy Bitcoin cheap in the US and sell it at inflated prices in South Korea. By some accounts, at its peak, the operation was generating roughly $25 million per day.

There’s a catch, and it’s an important one: the logistics were a nightmare. Moving fiat currency across borders, dealing with sketchy intermediaries, navigating regulatory gray zones. Several people who were involved in Alameda’s early operations would later describe the experience to journalists as chaotic, stressful, and at times terrifying. Money got stuck. Transfers failed. People had to physically carry cash. The whole thing was held together with duct tape and adrenaline.

But it worked. By early 2018, Alameda had reportedly generated over $100 million in revenue. SBF, still in his mid-twenties, was already very wealthy.

Internal Chaos

The money was flowing, but the operation was a disaster internally. According to multiple accounts, including testimony during SBF’s 2023 trial, Alameda’s early days were defined by poor record-keeping, almost no risk management, and a culture where questioning SBF’s decisions was essentially career suicide.

Several early employees and co-founders departed within the first year, some acrimoniously. They complained about SBF’s management style — or lack thereof. He made massive trading decisions unilaterally. He mixed personal and company funds. He kept the books in a state that one former employee would later describe to prosecutors as “a disaster.”

None of this mattered, because the money kept coming. And SBF had an even bigger idea.

🏗️ Chapter 3: FTX — Building the Exchange (2019–2021)

In May 2019, SBF launched FTX, a cryptocurrency exchange. The thesis was straightforward: existing crypto exchanges were clunky, unreliable, and built by engineers who didn’t understand what professional traders actually needed. SBF, having been a professional trader, would build the exchange that the market deserved.

And credit where it’s due: from a product standpoint, FTX was genuinely impressive. The platform was faster, more intuitive, and offered more sophisticated trading products than most competitors. It introduced innovations like tokenized stocks, prediction markets, and a liquidation engine that was meaningfully better than the industry standard. Serious traders loved it.

The Bahamas Move

In September 2021, SBF moved FTX’s headquarters from Hong Kong to the Bahamas. The stated reason was the regulatory environment — the Bahamas had created a framework for digital asset businesses that was more accommodating than most jurisdictions. The unstated reason, prosecutors would later allege, was that the Bahamas offered something even more valuable: distance from American regulators.

SBF installed himself and a small inner circle in a $30 million penthouse apartment in Albany, an ultra-luxury resort community in Nassau. According to prosecutors and trial testimony, FTX and Alameda insiders spent approximately $256 million on Bahamian real estate, often using company funds.

The Explosion of Growth

Between 2020 and early 2022, FTX’s growth was staggering. A $25 million Series A in 2019. A $900 million Series B in July 2021 at a valuation of $18 billion. Then, in January 2022, a $400 million Series C that valued FTX at $32 billion.

Read that again. $32 billion. For a crypto exchange that was barely three years old.

The investor list read like a who’s who of finance: Sequoia Capital, SoftBank, Tiger Global, the Ontario Teachers’ Pension Plan, Temasek, BlackRock. These weren’t crypto-native speculators. These were the most sophisticated institutional investors in the world. Sequoia famously published a glowing profile of SBF on their website — later deleted — that described a video call during which he appeared to be playing League of Legends. They found it charming. They invested anyway.

SBF was, according to Forbes, worth approximately $26 billion at his peak. He was the richest person under 30 in the world. He was on the cover of magazines. He testified before Congress, sitting next to traditional financial executives, and calmly argued for more crypto regulation. Senators were impressed. Reporters were charmed. The narrative was irresistible: the nerdy genius who was going to fix finance and give all the money to charity.

Meanwhile, according to federal prosecutors, the entire machine was running on stolen customer deposits.

🎭 Chapter 4: The Image — Effective Altruism and the World’s Most Expensive T-Shirt (2020–2022)

The SBF brand was, in our editorial view, one of the most sophisticated pieces of reputation engineering in modern business history. Every element was calibrated to project a single message: this person does not care about money for its own sake.

The messy hair. The cargo shorts. The beat-up sneakers. The Toyota Corolla — which he drove despite being worth billions. The beanbag he slept on at the office. The veganism. The public pledges to donate 99% of his wealth. He signed the Giving Pledge. He was featured in effective altruism conferences alongside moral philosophers. He told interviewers with apparent sincerity that he was “just trying to do the most good.”

“I wanted to have a positive impact on the world,” Bankman-Fried said in testimony during his trial in October 2023. The jury did not find this compelling.

Political Influence

SBF didn’t just talk about changing the world — he wrote checks. According to Federal Election Commission filings and reporting by The New York Times, Bankman-Fried donated approximately $40 million to political campaigns and PACs during the 2022 election cycle, making him one of the largest individual political donors in the United States. The donations went overwhelmingly to Democratic candidates, though Republican recipients existed as well. SBF would later tell journalist Tiffany Fong in an interview that some Republican donations were made through intermediaries to avoid public attention — a practice that, if true, would constitute illegal straw donations.

He cultivated relationships with members of Congress. He met with SEC officials. He hired an army of lobbyists. He wasn’t just building a business — he was building a regulatory moat, and he was using customer money to do it.

The Inner Circle

Behind the public persona was a small, tightly controlled group of insiders. Caroline Ellison, SBF’s on-again, off-again girlfriend, ran Alameda Research. Gary Wang, his MIT roommate, was FTX’s co-founder and CTO. Nishad Singh, another close associate, served as FTX’s Director of Engineering. These three would all eventually plead guilty to federal charges and testify against SBF at trial.

According to trial testimony from all three cooperating witnesses, the operation was essentially run as SBF’s personal fiefdom. He made the major decisions. He controlled the money. And critically, he was the one who allegedly directed that customer funds deposited into FTX be made available to Alameda Research through a secret backdoor in the exchange’s code — a backdoor that, according to Gary Wang’s testimony, exempted Alameda from the automated liquidation system that applied to every other user.

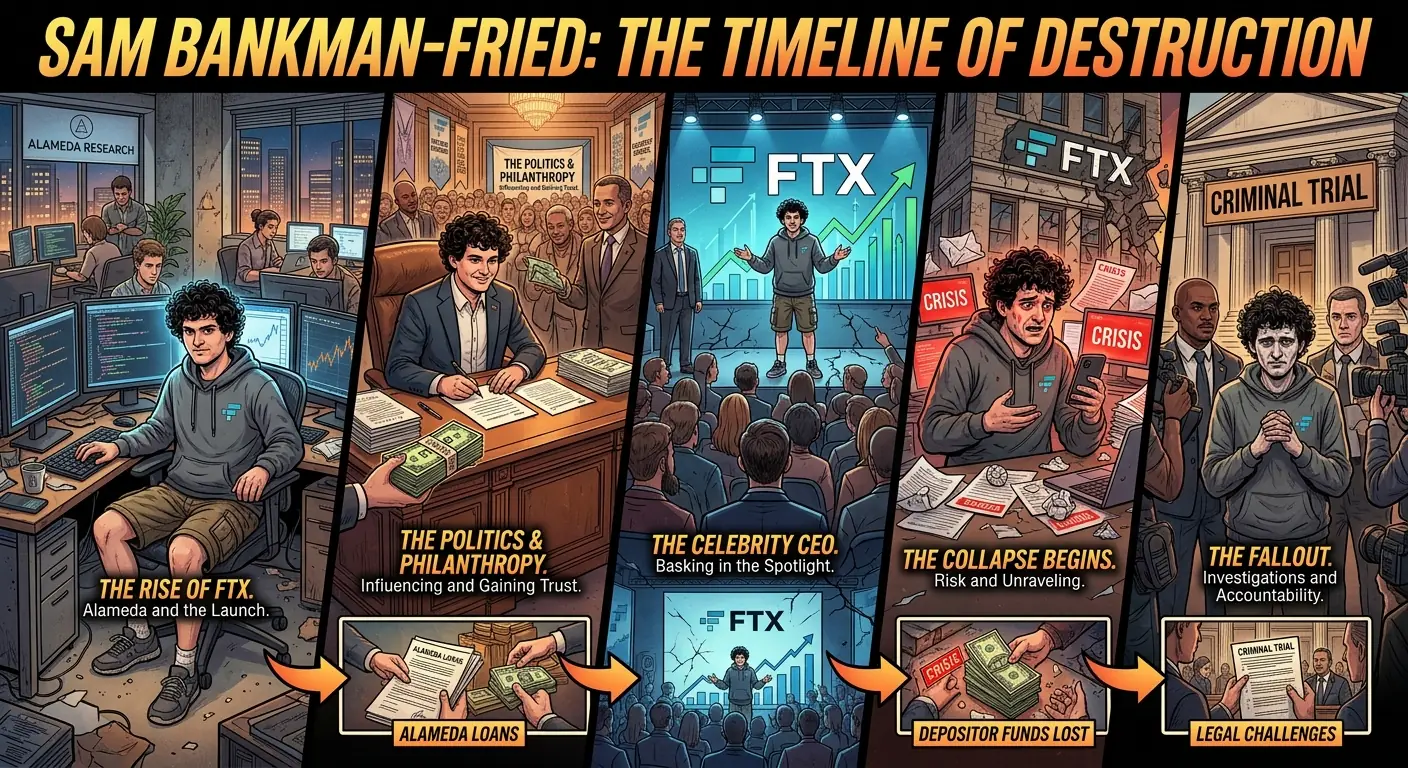

💣 Chapter 5: The CoinDesk Article — Six Days That Destroyed an Empire (November 2–8, 2022)

On November 2, 2022, a reporter at CoinDesk named Ian Allison published an article that would become one of the most consequential pieces of financial journalism in the 21st century.

The article was titled “Divisions in Sam Bankman-Fried’s Crypto Empire Blur on His Trading Titan Alameda’s Balance Sheet.” It was based on a leaked document — Alameda Research’s private balance sheet — and what it revealed was damning.

Alameda’s assets, according to the leaked document, were not primarily composed of independent, liquid assets like dollars or Bitcoin. Instead, a huge portion of Alameda’s $14.6 billion balance sheet was made up of FTT — the token that FTX itself had created. In other words, Alameda’s wealth was largely denominated in a token that its sister company had invented and whose value depended on the continued success of FTX. It was circular. It was self-referential. It was, in a word, fragile.

Changpeng Zhao Lights the Fuse

The CoinDesk article was bad. What happened next was catastrophic.

On November 6, 2022, Changpeng Zhao — known as CZ — the CEO of Binance, the world’s largest crypto exchange, tweeted: “As part of Binance’s exit from FTX equity last year, Binance received roughly $2.1 billion USD equivalent in cash (BUSD and FTT). Due to recent revelations that have come to light, we have decided to liquidate any remaining FTT on our books.”

That tweet was a kill shot. Binance was announcing that it would dump its massive FTT holdings on the open market. The implications were immediate: if FTT’s price collapsed, Alameda’s balance sheet would be destroyed. And if Alameda went down, would FTX go with it?

The answer came fast.

The Bank Run

Within hours of CZ’s tweet, FTX customers began withdrawing their funds. On November 6 alone, approximately $5 billion in withdrawal requests hit the exchange, according to SBF’s own later statements. This was the crypto equivalent of a bank run — and just like a bank run, it revealed a terrible truth: the money wasn’t there.

FTX could not honor the withdrawals because, prosecutors would later prove, the customer funds had been sent to Alameda Research to cover trading losses, make venture investments, purchase real estate, and fund political donations. The customer deposits were gone. They had been spent.

On November 8, in a stunning reversal, CZ announced that Binance had signed a non-binding letter of intent to acquire FTX. For a few hours, it seemed like a rescue might happen. SBF tweeted: “Things have come full circle, and FTX.com’s first, and last, parsee [sic] investor is the same: we have come to an agreement on a strategic transaction with Binance.”

Then, on November 9, Binance walked away. After looking at the books, Binance released a statement saying the issues were “beyond our control or ability to help.” Translation: the hole was too big.

FTX was dead. The six-day collapse — from the CoinDesk article on November 2 to the Binance withdrawal on November 9 — destroyed a $32 billion company and wiped out the savings of over one million customers worldwide.

⚖️ Chapter 6: The Arrest — From Penthouse to Prison (November 2022–March 2024)

On November 11, 2022, FTX filed for Chapter 11 bankruptcy. John J. Ray III — the same restructuring specialist who had unwound Enron — was appointed as CEO. His assessment of what he found was blistering. In a court filing, Ray stated: “Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here.”

That’s the Enron guy saying FTX was worse than Enron. Let that sink in.

According to Ray’s findings and subsequent court documents, FTX had no functioning accounting department. The company used QuickBooks — consumer-grade accounting software — to manage billions of dollars. Employee expenses were approved via emoji reactions on group chats. There was no board of directors providing meaningful oversight. Loans totaling over $3.3 billion had been made to insiders, including more than $1 billion to SBF personally.

The Bahamas Arrest

SBF didn’t run. Whether that was confidence, delusion, or simply a lack of better options remains debatable. He stayed in the Bahamas, gave a series of increasingly bizarre interviews — including one with The New York Times at the DealBook Summit via video link — in which he insisted he hadn’t committed fraud, said he was “deeply sorry,” and claimed he hadn’t knowingly commingled funds.

On December 12, 2022, Bahamian police arrested SBF at his Albany apartment at the request of the United States government. The Southern District of New York had unsealed an eight-count indictment charging him with wire fraud, conspiracy to commit money laundering, securities fraud, and campaign finance violations.

He was extradited to the United States on December 21. Initially released on a $250 million bond — one of the largest in U.S. history — he was confined to his parents’ home in Palo Alto, California, with an ankle monitor. Even this arrangement didn’t last. In August 2023, Judge Lewis Kaplan revoked SBF’s bail after prosecutors presented evidence that he had attempted to tamper with witnesses, including sharing Caroline Ellison’s private journal entries with The New York Times. He was remanded to the Metropolitan Detention Center in Brooklyn to await trial.

The Trial

The trial of United States v. Samuel Bankman-Fried began on October 3, 2023, in the Southern District of New York, before Judge Lewis Kaplan.

The prosecution’s case was devastating, built largely on the testimony of SBF’s former inner circle. Caroline Ellison, who had pleaded guilty and agreed to cooperate, testified that SBF had directed her to use FTX customer funds to cover Alameda’s losses. She described a culture of deception, testifying: “He directed me to commit these crimes.” Gary Wang testified that he had built the secret code — the backdoor — that allowed Alameda to borrow unlimited funds from FTX’s customer accounts, and that SBF had instructed him to do so. Nishad Singh broke down in tears on the stand while describing what he characterized as the scale of the fraud.

SBF took the stand in his own defense — a risky move. He was combative, evasive, and frequently said he “didn’t recall” specific events. His defense centered on the argument that he had made mistakes but had not intended to defraud anyone. The jury was not convinced.

On November 2, 2023 — exactly one year after the CoinDesk article that started the unraveling — the jury found Sam Bankman-Fried guilty on all seven counts he faced at trial.

The Sentence

On March 28, 2024, Judge Kaplan sentenced SBF to 25 years in federal prison. Prosecutors had requested 40 to 50 years. The defense had asked for five to six-and-a-half years.

Judge Kaplan, in delivering the sentence, stated that he believed SBF had committed perjury during his trial testimony. “He knew it was wrong. He knew it was criminal,” Kaplan said from the bench. “There is a risk that this man will be in a position to do something very bad in the future, and it’s not a trivial risk.”

The sentence was the harshest ever handed down for a financial crime in the cryptocurrency industry. SBF was ordered to forfeit over $11 billion.

💀 Chapter 7: The Wreckage — What Was Left Behind

The collapse of FTX sent shockwaves through the entire cryptocurrency industry and far beyond.

The Victims

Over one million customers had funds on FTX when it collapsed. The total customer shortfall was estimated at approximately $8.7 billion, according to bankruptcy court filings. These were not all wealthy speculators. Many were ordinary people in developing countries — Nigeria, Turkey, South Korea — who had trusted FTX with their savings.

The bankruptcy proceedings, led by John Ray III and the law firm Sullivan & Cromwell, ultimately recovered far more than initially expected. By 2024, the estate announced that 98% of creditors would receive at least 118% of their allowed claims in cash — a remarkable recovery driven largely by the appreciation of crypto assets after FTX’s collapse and the sale of FTX’s venture portfolio. But the recovery doesn’t erase the harm: customers spent months or years locked out of their funds, some facing genuine financial hardship, and the recovery was in dollar terms based on November 2022 prices, meaning those who had held Bitcoin or other assets missed the subsequent market rally.

The Industry Fallout

FTX’s collapse triggered a cascading series of failures across crypto. BlockFi, which had significant exposure to FTX and Alameda, filed for bankruptcy. Genesis, a major crypto lender, followed. The contagion spread. Regulatory crackdowns accelerated worldwide. The SEC filed lawsuits against multiple crypto exchanges and projects. Congressional hearings multiplied. The era of crypto companies operating in regulatory gray zones was effectively over.

The Cooperators

Caroline Ellison was sentenced to two years in prison in September 2024. Gary Wang received no prison time — a reflection of his extensive cooperation. Nishad Singh also avoided incarceration. Ryan Salame, FTX’s co-CEO, was sentenced to seven and a half years after pleading guilty to campaign finance violations and operating an unlicensed money transmission business.

The Effective Altruism Reckoning

The EA movement, which had embraced SBF as its most prominent success story and received tens of millions in his donations, faced an existential crisis. The FTX Future Fund, which SBF had established to distribute hundreds of millions to EA causes, collapsed overnight. Grants were clawed back. Organizations that had planned around FTX money found themselves suddenly defunded. The philosophical question that haunted the movement was uncomfortable: had “earning to give” provided moral cover for exactly the kind of reckless, ends-justify-the-means behavior that led to the fraud?

🔑 Chapter 8: The Autopsy — How It Actually Worked

The mechanics of the fraud, as established at trial, were simpler than the crypto jargon suggested.

FTX customers deposited money — dollars, Bitcoin, other cryptocurrencies — into the exchange to trade. That money was supposed to stay in FTX accounts, available for withdrawal at any time. Instead, according to prosecutors and cooperating witness testimony, customer deposits were funneled to Alameda Research through a series of mechanisms.

The primary channel was a secret exemption in FTX’s code. While every other trading firm on FTX was subject to automatic liquidation if their accounts went negative — meaning the system would force-sell their positions to prevent losses from exceeding their deposits — Alameda had a special privilege that allowed it to maintain a negative balance of virtually unlimited size. This meant Alameda could borrow from FTX’s pool of customer funds without limit and without triggering any alarms.

According to trial testimony, by mid-2022, Alameda owed FTX approximately $8 billion — money that belonged to FTX customers. Alameda used these funds for everything from covering trading losses to making venture capital investments to purchasing Bahamian real estate to making political donations.

When customers tried to withdraw their money, the system worked — until it didn’t. As long as total withdrawals on any given day were smaller than the remaining pool of customer funds, nobody noticed. It was, in essence, a digital version of the oldest financial crime in existence: taking money from Peter to pay Paul, and hoping you can stay ahead of the math.

The CoinDesk article and CZ’s tweet created a withdrawal surge that exceeded the remaining pool. The scheme collapsed not because it was discovered internally, but because external events triggered a run that the depleted reserves could not sustain.

📉 The Timeline of Destruction

For clarity, here’s how fast a $32 billion empire disintegrated:

- November 2, 2022 — CoinDesk publishes Alameda’s balance sheet. FTT’s circular dependency is exposed.

- November 6 — Changpeng Zhao tweets that Binance will sell its FTT holdings. $5 billion in withdrawal requests hit FTX in 24 hours.

- November 7 — FTT price crashes over 30%. FTX halts withdrawals intermittently.

- November 8 — Binance announces intent to acquire FTX. Brief relief.

- November 9 — Binance walks away after due diligence. FTX halts all withdrawals.

- November 10 — SBF’s net worth drops from $16 billion to effectively zero in a single day, per Bloomberg Billionaires Index.

- November 11 — FTX files for bankruptcy. SBF resigns. John Ray III takes over.

- December 12 — SBF arrested in the Bahamas.

- October 3–November 2, 2023 — Trial in SDNY.

- November 2, 2023 — Guilty on all counts.

- March 28, 2024 — Sentenced to 25 years.

From the CoinDesk article to bankruptcy: six days. From the wealthiest under-30 on Earth to federal inmate: sixteen months.

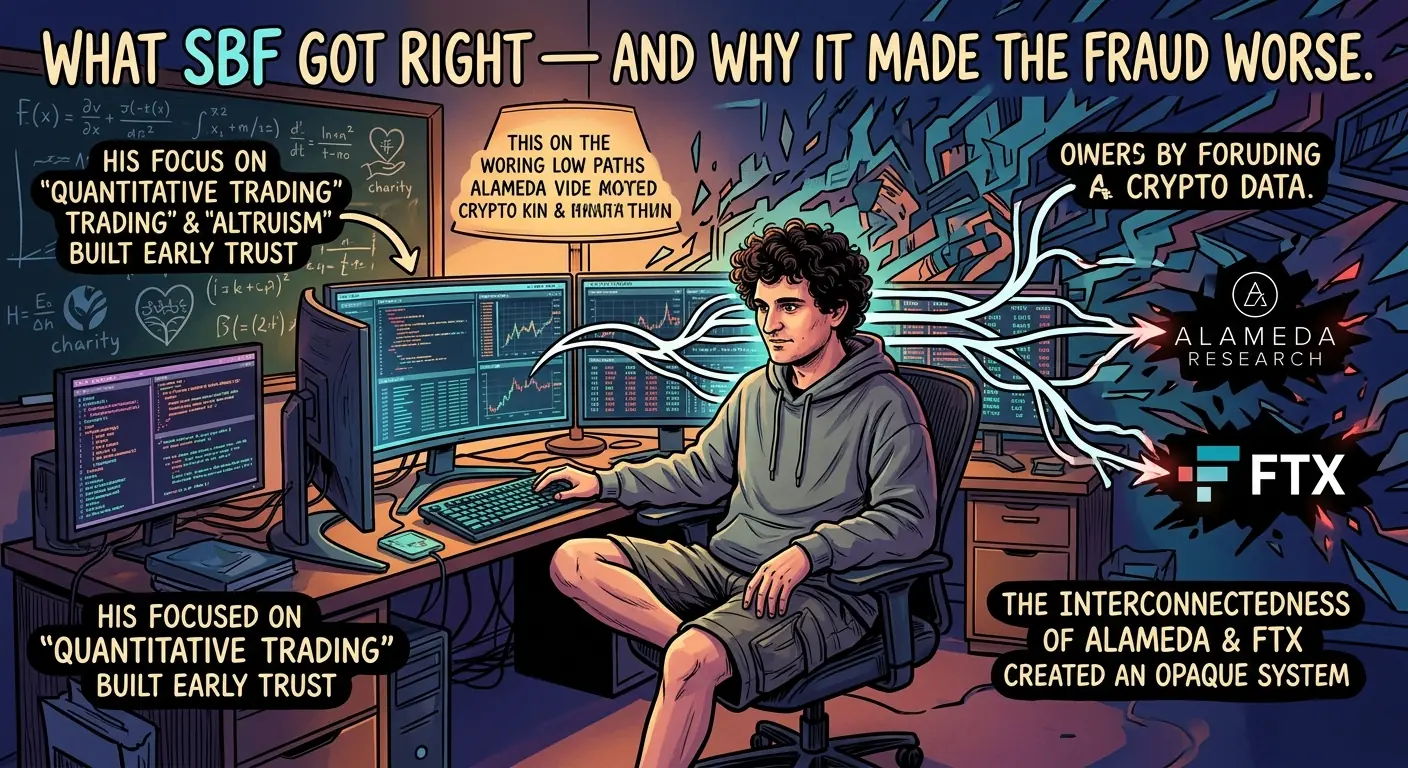

🧠 What SBF Got Right — And Why It Made the Fraud Worse

This is the part that makes the story genuinely tragic rather than merely criminal.

SBF was right about several things. Cryptocurrency exchanges were poorly built. There was a massive opportunity in bringing institutional-grade infrastructure to crypto markets. FTX’s product was better than its competitors. The arbitrage opportunities in early crypto were enormous.

He had real talent, real intelligence, and real vision. He wasn’t a pure con artist selling nothing — he was building something genuine and then destroying it by stealing from the people who trusted him. That’s worse, in a way. A pure scam is easier to spot. A brilliant product built on stolen money is the kind of trap that catches sophisticated investors, journalists, and regulators alike.

Tom Brady endorsed FTX. Steph Curry endorsed FTX. The Miami Heat played in the FTX Arena. Sequoia Capital — Sequoia! — invested $214 million. The Ontario Teachers’ Pension Plan put in $95 million of Canadian teachers’ retirement savings. These weren’t rubes. They were the smart money. And they all got fooled because the product was real, the growth was real, and the guy running it was telling everyone he wanted to give all the money to charity.

“I think the thing that I’m most sorry about is that — I screwed up,” Bankman-Fried said during his sentencing hearing in March 2024. Judge Kaplan was unmoved.

The lesson of Sam Bankman-Fried isn’t that crypto is a scam. It’s that the same human failures — greed, self-deception, the willingness to cut corners when you believe the ends justify the means — will find their way into any system, new or old, regulated or not, that involves large amounts of other people’s money. The technology changes. The fraud doesn’t.

SBF is currently serving his 25-year sentence at a federal prison. He will be eligible for release in approximately 2044. He will be 52 years old.

His customers got their dollars back, eventually. What they lost — the trust, the time, the faith that the system was what it claimed to be — doesn’t fit on a balance sheet.

🫂 Chapter 9: The Inner Circle — A Polycule of Power (2018–2022)

So, you’ve got Sam Bankman-Fried, the brilliant, socially awkward wunderkind who’s convinced he’s going to save the world by making billions. What kind of people do you think he surrounds himself with? Not your typical Wall Street types, that’s for sure. SBF cultivated an inner circle that was less a corporate executive team and more a tight-knit, insular commune of effective altruists, many of whom were also engaged in polyamorous relationships. If you thought the “sleep on a beanbag” thing was quirky, just wait.

The Stanford-Berkeley Nexus: A Family Affair (of sorts)

The core team at Alameda Research and later FTX wasn’t just a collection of random hires. It was a carefully curated group, heavily skewed towards young, bright graduates from elite universities (Stanford, MIT, Berkeley, Carnegie Mellon), many of whom were deeply steeped in the effective altruism philosophy. Caroline Ellison, the eventual CEO of Alameda, was a Stanford math graduate who had worked at Jane Street with SBF. Nishad Singh, FTX’s Director of Engineering, was an MIT classmate and lifelong friend. Gary Wang, FTX’s CTO, was another MIT alum and former Google software engineer. These weren’t just employees; they were ideological fellow travelers, bound by shared beliefs and, in several cases, romantic entanglements.

This created an echo chamber, a “friendship group that also happened to be running a multi-billion-dollar crypto empire,” as one former employee put it. It meant that critical checks and balances, the kind of boring corporate governance that prevents financial meltdown, were often ignored or deemed unnecessary. Who needs a robust compliance department when everyone trusts each other implicitly? (Spoiler: everyone.) SBF himself reportedly spent little time in meetings, often playing video games while others handled the day-to-day. The irony of building a multi-billion dollar empire with the management style of a dorm room Dungeons & Dragons session is truly something.

The Bahamas Penthouse: Where Work Met… Everything Else

When FTX moved its headquarters to the Bahamas in late 2021, the inner circle followed, settling into a luxurious, sprawling penthouse in the Albany Resort. This wasn’t just an office; it was a living experiment. SBF, Ellison, Singh, Wang, and about eight other key figures lived together, sharing bedrooms, meals, and, yes, romantic relationships. This setup, often described as a “polycule,” further blurred the lines between personal and professional.

As detailed in Michael Lewis’s Going Infinite, and later confirmed by witnesses during SBF’s trial, the atmosphere was chaotic, intense, and fueled by a relentless drive to work. There were allegations of drug use, specifically Adderall, to maintain the grueling pace. This wasn’t just a bunch of kids coding in a garage; this was a multi-billion-dollar operation being run out of a shared living space with virtually no oversight. Imagine running a Fortune 500 company where the CEO is dating the CFO, the head of engineering, and possibly half the board, and everyone lives in the same house. The potential for conflicts of interest, emotional baggage, and sheer corporate lunacy was off the charts. It fostered an environment where secrecy thrived and dissent was likely stifled, if not outright impossible. When your entire executive team shares a toothbrush, asking tough questions about a missing $8 billion might feel a little awkward.

“The whole thing was set up to be a completely self-contained world,” one former employee recounted, highlighting the insular nature of the operation. “If you weren’t in the penthouse, you weren’t really in the loop.”

The “Effective Altruism” of the Heart

The deep personal connections, combined with the effective altruism ideology, created a potent cocktail. They believed they were doing good, even when they were (allegedly) doing very bad things. The constant refrain was “earning to give,” but it seems the “earning” part became an end in itself, and the “giving” was more of a future promise that justified any present action. The shared living, the shared ideology, the shared relationships – it all contributed to a collective delusion where ethical boundaries became increasingly blurry. It wasn’t just about money; it was about a shared identity, a shared purpose, and ultimately, a shared downfall. The irony being, of course, that a group so dedicated to “doing good” managed to cause so much harm, arguably because they were too close to see the forest for the polycule.

🥊 Chapter 10: The Crypto Wars — SBF vs. CZ and the Battle for Dominance (2021–2022)

The crypto world is a wild west, but even in a land of outlaws, there are kings. For a long time, Changpeng “CZ” Zhao, the founder of Binance, was the undisputed monarch. Then Sam Bankman-Fried arrived, fresh off his Alameda success, with a new exchange, FTX, and an ambition that knew no bounds. What began as a strategic partnership quickly devolved into one of the most significant rivalries in crypto history, a clash of titans that ultimately played a starring role in FTX’s spectacular collapse. It was less a gentle competition and more a digital street brawl, with billions on the line.

Binance’s Early Investment: A Reluctant Embrace

In a move that would later prove to be a massive headache for both parties, Binance was an early investor in FTX. In December 2019, Binance invested an undisclosed sum, reportedly around $100 million, in FTX and took a stake in the FTT token, FTX’s native exchange token. This was a common strategy for larger exchanges to hedge bets and support promising newcomers. However, by July 2021, the relationship had soured. FTX was growing at an alarming rate, threatening Binance’s dominance. SBF bought out Binance’s stake in FTX for a reported $2 billion, paid partly in FTT tokens and partly in Binance USD (BUSD).

This transaction was a turning point. It marked FTX’s declaration of independence and its clear intent to challenge Binance for the top spot. CZ later stated that the decision to divest was mutual, but the underlying tension was palpable. SBF, known for his relentless ambition, wasn’t content to be number two. He wanted the crown, and he wasn’t shy about it. The crypto world watched as the two exchanges, led by their charismatic (and very different) founders, began to circle each other, each vying for market share, regulatory favor, and industry influence. It was like watching two Godzilla-sized tech bros duke it out, only with fewer skyscrapers and more tweets.

The FTT vs. BNB Showdown: A Proxy War

The rivalry wasn’t just about trading volumes; it was a proxy war waged through their native tokens. Binance Coin (BNB) was the lifeblood of the Binance ecosystem, offering trading fee discounts and access to exclusive sales. FTT was FTX’s equivalent, promising similar perks. As FTX grew, the value of FTT became a critical metric of its success and stability.

The conflict reached its boiling point in early November 2022. A CoinDesk article (which we covered in Chapter 5) revealed that Alameda Research’s balance sheet was heavily reliant on FTT tokens, a token issued by its sister company, FTX. This was a massive red flag, implying that Alameda’s assets were essentially backed by FTX’s own printed money. CZ, ever the shrewd operator, saw his opening. On November 6, 2022, he tweeted:

“As part of Binance’s exit from FTX equity last year, Binance received roughly $2.1 billion USD equivalent in cash… and FTT. We have decided to liquidate any remaining FTT on our books.”

This single tweet, from the CEO of the world’s largest crypto exchange, sparked a bank run. It was a calculated move, effectively signaling a lack of confidence in FTX and Alameda. While CZ later claimed it was merely risk management, the timing and public nature of the announcement were widely seen as a strategic strike against a formidable rival. The FTT token, already under scrutiny, plummeted, taking Alameda’s balance sheet with it and triggering the cascade that would bring down FTX. It was a masterclass in competitive destruction, executed with the cold precision of a chess grandmaster. Or perhaps, a well-timed punch in a crypto cage match.

Regulatory Ambitions: SBF’s Pivot to D.C.

Beyond the token wars, SBF also sought to gain an edge through regulation. While Binance often operated in a more decentralized, global, and sometimes legally ambiguous manner, SBF made a highly publicized pivot to Washington D.C. in 2022. He became a vocal advocate for crypto regulation, testifying before Congress and making massive political donations (as discussed in Chapter 4). His aim was to shape the regulatory landscape in FTX’s favor, potentially creating barriers for competitors like Binance, who faced their own ongoing regulatory challenges in various jurisdictions.

This aggressive lobbying, however, ultimately backfired. While SBF positioned himself as the “responsible adult” of crypto, his efforts were seen by many in the industry, including CZ, as an attempt to centralize power and stifle innovation, often at the expense of smaller players. The very regulatory framework he sought to influence would eventually be the one that brought him down, highlighting the profound irony of his “effective altruism” applied to lobbying. In the end, the crypto war wasn’t won by better regulation or superior tech; it was won by the company whose balance sheet wasn’t built on a house of cards.

🧊 Chapter 11: The Trial and the Fallouts — Justice (or Lack Thereof) and the Industry’s Reckoning (2023–Present)

After the whirlwind of his arrest, extradition, and an initial period of house arrest at his parents’ Palo Alto home (the ultimate “time out” for a grown-up billionaire), Sam Bankman-Fried’s fate would be decided in a New York courtroom. The trial, spanning just over a month in the fall of 2023, captivated the financial world, offering a rare, unvarnished look into the inner workings of a multi-billion-dollar fraud. It was less a legal proceeding and more a meticulously crafted exposé of hubris, deception, and the chilling consequences of unchecked power.

The Star Witnesses: Former Friends Turn State’s Evidence

The prosecution’s case was built not just on documents and financial records, but on the damning testimony of SBF’s closest confidantes – the very people who lived and worked with him in that Bahamian penthouse. Caroline Ellison, Alameda’s CEO and SBF’s on-again, off-again romantic partner, took the stand and delivered devastating testimony. She admitted to conspiring with SBF to misappropriate FTX customer funds, manipulate the price of FTT, and falsify Alameda’s balance sheets. She described SBF as directing her to use FTX customer money to repay Alameda’s loans, knowing it was wrong.

Equally crucial were the testimonies of Gary Wang, FTX’s CTO, and Nishad Singh, FTX’s Director of Engineering. Wang testified that SBF instructed him to implement code that allowed Alameda to withdraw virtually unlimited funds from FTX, even when it didn’t have the assets to back it up. Singh corroborated this, explaining how he wrote code to conceal Alameda’s massive debt. These were not external enemies, but members of SBF’s self-proclaimed “inner circle,” each facing their own legal battles, but all agreeing on one thing: Sam Bankman-Fried was at the center of the fraud. Their collective testimony painted a picture of SBF as the orchestrator, not an unwitting participant. It was a brutal betrayal, but one necessitated by self-preservation.

“He was the one who set up the system that allowed Alameda to take money from FTX customers,” Caroline Ellison stated matter-of-factly during her testimony, sealing SBF’s fate with chilling clarity.

The Defense Strategy: “I Didn’t Know” vs. “I Was Just Doing My Job”

SBF’s defense was, to put it mildly, a tough sell. His lawyers attempted to paint him as a well-intentioned but overwhelmed CEO who made mistakes, but never intended to defraud anyone. SBF himself took the stand, a risky move for any defendant, and spent days trying to distance himself from the day-to-day operations of Alameda, claiming he was unaware of the extent of its liabilities or the illicit use of customer funds. He argued that he was primarily focused on “risk management” and that others were responsible for the accounting errors.

However, his testimony was often evasive, contradictory, and failed to account for the detailed, corroborating evidence provided by his former colleagues and the prosecution’s financial experts. The prosecution skillfully dismantled his claims, showing how deeply involved he was in critical decisions and how the system was designed to benefit Alameda at FTX customers’ expense. The jury wasn’t buying the “I’m just a messy math genius who accidentally misplaced $8 billion” routine. On November 2, 2023, after just a few hours of deliberation, a jury found Sam Bankman-Fried guilty on all seven counts of fraud, conspiracy, and money laundering. It was a swift, decisive verdict that left little room for doubt.

The Ripple Effect: Who Else Paid the Price, and the Industry’s Reckoning

SBF’s conviction was a landmark moment, but the fallout extended far beyond his prison sentence. Many other key figures from FTX and Alameda, including Ellison, Wang, and Singh, pleaded guilty and cooperated with prosecutors, hoping for leniency. The saga sent shockwaves through the crypto industry, triggering a deeper regulatory scrutiny that continues to reshape the landscape. It exposed the perils of opaque financial structures, the dangers of centralized power in a supposedly decentralized world, and the seductive allure of “move fast and break things” when those “things” are other people’s life savings.

While SBF is now behind bars, the victims of FTX’s collapse, from individual retail investors to institutional players, are still grappling with the losses. The recovery process, led by FTX’s new CEO, John Ray III (who famously oversaw the Enron bankruptcy), is painstakingly slow, with many unlikely to recoup their full investments. The lessons are stark: trust, but verify; regulation, however imperfect, serves a purpose; and even the most brilliant minds, fueled by the loftiest ideals, can fall prey to the oldest temptations of greed and deceit. The crypto world learned a hard lesson, etched in the billions lost and the reputation of a former prodigy, now inmate.

💡 Key Insights

- ▸ FTX proved that in unregulated markets, the appearance of legitimacy is more dangerous than obvious fraud. Bankman-Fried didn't look like a con artist — he looked like a genius philanthropist, which is exactly why billions flowed in unchecked. The most effective deception wears the costume of virtue.

- ▸ Customer funds are not your venture capital. The moment FTX began funneling depositor money to Alameda Research, it crossed from aggressive business into theft. No amount of genius trading or market-making justifies using other people's money without their knowledge or consent.

- ▸ The 'effective altruism' brand gave Bankman-Fried a moral shield that delayed scrutiny by years. When a billionaire says they're making money to give it all away, regulators, reporters, and investors relax. The lesson: judge institutions by their controls, not their founder's stated philosophy.

- ▸ Concentrated, interconnected entities without independent oversight are financial time bombs. FTX and Alameda shared staff, funds, and systems with no meaningful separation. This isn't innovation — it's the exact structural failure that traditional financial regulation was designed to prevent.

- ▸ The crypto industry's collapse wasn't caused by blockchain technology failing — it was caused by humans doing the same things humans have always done when given access to other people's money with no one watching. The technology was new; the fraud was ancient.

Sources

- Michael Lewis — Going Infinite: The Rise and Fall of a New Tycoon ↗

- CoinDesk — Divisions in Sam Bankman-Fried's Crypto Empire Blur on His Trading Titan Alameda's Balance Sheet ↗

- U.S. Department of Justice — United States v. Samuel Bankman-Fried ↗

- The Wall Street Journal — FTX Collapse Coverage ↗

- SEC Complaint Against Samuel Bankman-Fried ↗

- Reuters — FTX Trial and Sentencing Coverage ↗

- New York Times — FTX's Collapse and the Fallout ↗